Gold is one of the most preferred investment options in India, available in multiple forms such as physical gold, Gold ETFs, Sovereign Gold Bonds (SGBs), digital gold, and gold mutual funds. Each form has a different tax treatment under the Income-tax Act. This article explains the taxation on sale of gold in a simple and professional manner.

1. Physical Gold (Jewellery, Coins & Bars)

Physical gold includes jewellery, coins, and bars. Tax is applicable at the time of sale based on the holding period.

• Short-Term Capital Gain (STCG): If sold within 24 months, gains are taxed as per the individual’s income tax slab. • Long-Term Capital Gain (LTCG): If held for more than 24 months, gains are taxed at 12.5% without indexation. • GST paid at the time of purchase is not refundable and forms part of the cost.

2. Gold Exchange Traded Funds (ETFs)

Gold ETFs are paper gold investments traded on stock exchanges and backed by physical gold.

• STCG: Units sold within 12 months are taxed as per income tax slab rates. • LTCG: Units sold after 12 months are taxed at 12.5% without indexation.

3. Sovereign Gold Bonds (SGBs)

Sovereign Gold Bonds are issued by the RBI on behalf of the Government of India and are considered the most tax-efficient form of gold investment.

• If held till maturity (8 years): Capital gains are completely tax-free. • If sold on stock exchange: – Within 12 months: Taxed at slab rates. – After 12 months: Taxed at 12.5% without indexation. • Interest earned (around 2.5% annually) is taxable as per slab rates.

Amendment in Finance Bill, 2026 “exemption will be applicable only to those Sovereign Gold Bonds issued by the Reserve Bank of India that are subscribed to by an individual at the time of original issue and are held continuously by such individual until redemption upon maturity” it means Capital gains exemption does not apply if bought from secondary market.

4. Digital Gold & Gold Mutual Funds

Digital gold and gold mutual funds offer convenience and flexibility but follow similar tax rules.

• STCG: If sold within 24 months, gains are taxed as per income tax slab. • LTCG: If sold after 24 months, gains are taxed at 12.5% without indexation.

Conclusion:

From a tax perspective, Sovereign Gold Bonds are the most efficient option for long-term investors, while Gold ETFs and mutual funds provide liquidity with moderate taxation. Physical gold, though culturally significant, is the least tax-efficient due to GST and higher holding period requirements.

In Tabular Format

Investment type

Short-term capital gains (STCG)

Long-term capital gains (LTCG)

Notes

Sovereign Gold Bonds (SGBs)

If sold within 12 months: taxed at slab rate

If held beyond 12 months and sold before maturity: 12.5% without indexation; Nil if held till 8-year maturity

Capital gains exemption does not apply if bought from secondary market

Gold ETFs

Up to 12 months: taxed at slab rate

Beyond 12 months: 12.5% without indexation

Treated as listed securities

Gold mutual funds

Up to 24 months: taxed at slab rate

Beyond 24 months: 12.5%

Usually invest in gold ETFs

Physical gold

Up to 24 months: taxed at slab rate

Beyond 24 months: 12.5%

GST paid cannot be set off against capital gains tax

Gifted gold

Taxable only if gift from non-relatives exceeds ₹50,000

Taxable in the recipient’s hands

Gifts from specified relatives are tax-free

Inherited gold

Capital gains apply on sale

Capital gains apply on sale

Original owner’s cost and holding period are considered

India’s labour law landscape has undergone its most profound transformation in decades with the implementation of the four new Labour Codes, effective from 21 November 2025. This historic move rationalizes 29 existing labour statutes into a streamlined and modern framework. The aim is to simplify and streamline regulations, enhance workers’ welfare, align the labour ecosystem with global standards, and lay the foundation for a future-ready workforce, boosting employment and driving reforms for Aatmanirbhar Bharat.

The key provisions include universal minimum wages, standardized working conditions, broadened social security coverage, and simplified industrial dispute procedures.

The Four Pillars of Reform

The government has brought into force the key provisions of four consolidated codes:

1. Code on Wages, 2019: Focuses on wages, bonus, and equal remuneration.

2. Industrial Relations Code, 2020: Deals with trade unions, standing orders, and dispute resolution.

3. Code on Social Security, 2020: Expands coverage for benefits like PF, ESI, Gratuity, and includes gig workers.

4. Occupational Safety, Health & Working Conditions (OSHWC) Code, 2020: Covers safety, health, and welfare, including rules for working hours and women’s employment.

The new framework introduces several themes designed to unify compliance across all establishments:

Theme

Summary of Change

Unified Definition of “Wages”

Wages comprise basic pay, dearness allowance, and retaining allowance minus specified exclusions. Exclusions are capped, meaning at least 50% of the employee’s Cost-to-Company (CTC) must be counted as wages for calculating benefits like PF, gratuity, and overtime.

Single Registration & Return

Establishments register once on the Shram Suvidha portal and file a consolidated return instead of multiple returns under different laws.

Inspector-cum-Facilitator

Traditional inspectors are re-designated as “facilitators” who advise employers on compliance. They conduct risk-based digital inspections and still hold powers to issue notices and inspect records.

Decriminalisation & Compounding

Many procedural offences have been decriminalized. First-time minor procedural offences can often be compounded by paying 50% of the maximum fine, promoting compliance over punitive action.

Digital Compliance

Employers are permitted to maintain registers and submit forms electronically, primarily through the Shram Suvidha portal.

Key Features of the Four Labour Codes:

The following table summarizes the core mandates and applicability thresholds for the four codes:

Code

Core Provisions and Features

Applicability Highlights

Code on Wages, 2019

National Floor Wage: Central government notifies a floor wage that states cannot set minimum wages below. Wages must be reviewed at least every five years. Equal Remuneration: Enforces equal pay for equal work irrespective of gender or transgender status. Overtime: Must be paid at double the ordinary wage for work beyond 8 hours/day or 48 hours/week. Final Settlement (FnF): Requires settlement of all wages and dues (including salary and leave encashment) within two working days of dismissal, retrenchment, removal, or voluntary resignation.

Applies to all employees in organized and unorganized sectors, covering factories, shops, IT/ITES, and gig workers.

Industrial Relations Code, 2020

Standing Orders: Mandatory for employers with 300 or more workers (covering service rules like classification, hours, and misconduct). Lay-off/Closure: Establishments with 300+ workers require prior government permission for lay-off (15 days notice), retrenchment (60 days notice), or closure (90 days notice). Grievance Redressal Committee (GRC): Mandatory for establishments with 20+ workers, requiring equal worker and management representation, including at least one woman representative. Dispute Resolution: Accelerated process through two-member tribunals; parties can approach directly if conciliation fails within 90 days.

Applicability threshold for certain provisions (like standing orders) is 300 workers. Extends the definition of “worker” to include sales promotion staff and supervisory employees earning up to about ₹18,000/month.

Code on Social Security, 2020

Gig & Platform Workers: Recognizes these workers; aggregators must contribute 1–2% of annual turnover (capped at 5% of payments to workers) to a social security fund. Gratuity: Fixed-term employees become eligible for gratuity after one year of service. Maternity Benefit: Retains 26-week paid leave and mandates crèche facilities for establishments with 50 or more employees. EPF & ESIC: Coverage is extended Pan-India and made voluntary for establishments with fewer than 10 employees, but mandatory for hazardous industries regardless of size.

Applies to all establishments, employees, and workers, including unorganised, gig, and platform workers.

OSHWC Code, 2020

Working Hours: Normal working day limited to eight hours. Employment of Women: Removes blanket prohibitions; women may work night shifts and in all types of establishments, including mines, with their consent and subject to safety conditions like safe transport and security. Health & Welfare: Mandatory annual health check-ups for workers aged over 40. Safety Committees: Mandatory in establishments employing 500 or more workers.

Covers factories (with revised thresholds: 20 workers w/ power or 40 w/o power), mines, plantations, contract labour, and migrant workers.

The reforms are designed to extend protections to vulnerable and non-traditional employment sectors:

Worker Category

New Benefit/Protection under the Codes

All Workers

Mandatory appointment letters to ensure transparency, job security, and formal employment. Statutory right to minimum wage and timely payment.

Gig & Platform Workers

Mandatory social security coverage and defined contribution model from aggregators. Aadhaar-linked Universal Account Number (UAN) for portable benefits.

Fixed-Term Employees (FTE)

Eligible for all benefits (leave, medical, social security) equal to permanent workers. Gratuity eligibility after only one year of continuous service.

Women Workers

Permitted to work night shifts and in all types of work (including underground mining) subject to consent and safety measures. Explicit prohibition of gender discrimination and guarantee of equal pay for equal work.

Inter-State Migrant Workers

Defined to cover self-migrated workers; receive annual travel allowance, portability of ration and social security benefits, and access to a toll-free helpline.

Practical Obligations for Employers:

The implementation of the Codes places greater responsibilities on employers, particularly concerning payroll and HR procedures. Employers must revise their operations to ensure compliance:

• Review Wage Structure: Salary components must be reworked to ensure that at least 50% of CTC is classified as “wages” to avoid penalties related to PF/bonus liability misclassification.

• Establish FnF Workflow: Companies should adopt a strict T+2 working day internal standard for full-and-final settlement upon an employee’s exit (resignation, termination, etc.).

• Update Registration: Register on the Shram Suvidha portal (Form II) to obtain a single Labour Identification Number (LIN).

• Maintain Records: Issue wage slips (Form V) and maintain statutory registers electronically, including those for fines (Form I), deductions (Form IV), employee details (Form VI), and attendance/wages/overtime (Form VII).

• Safety Compliance: Conduct periodic safety audits, provide free annual medical check-ups for workers over 40, and supply Personal Protective Equipment (PPE) and training.

Failure to Comply: particularly regarding non-payment of minimum wages or delayed remittance of contributions (PF/ESI), can lead to serious penalties, including fines up to ₹50,000 for first offences or imprisonment for repeat violations or serious negligence causing death.

The four labour codes represent a paradigm shift aimed at fostering a fair, safe, and productive work environment by simplifying the fragmented laws and expanding the social safety net.

Q&A: New Labour Codes

1. What are the New Labour Codes?

The Government of India has consolidated 29 existing labour laws into four major Labour Codes:

Code on Wages, 2019

Industrial Relations Code, 2020

Occupational Safety, Health and Working Conditions (OSH) Code, 2020

Social Security Code, 2020

2. When will the new labour codes come into effect?

The codes are scheduled to be implemented from 21 November 2025 across India.

3. Why were labour laws consolidated?

To:

Simplify compliance

Improve ease of doing business

Provide uniform definitions

Protect workers with updated standards

Enable digital and transparent systems

4. Who will be covered under the new labour codes?

The Codes apply to:

All establishments

All employees (skilled, unskilled, managerial, operational)

Contract labour

Gig and platform workers (under Social Security Code)

Inter-state migrant workers

5. What is the biggest reform introduced under the Code on Wages?

A universal definition of wages that applies across all labour laws—affecting PF, gratuity, leave encashment, and salary structuring.

6. What is the new definition of “Wages”?

“Wages” include basic pay + DA + retaining allowance, capped at a minimum of 50% of total CTC. Allowances cannot exceed 50%. If allowances exceed 50%, the excess will be added back into “wages”.

Salaried individuals who engage in stock trading or Futures & Options (F&O) transactions often have queries about income tax return filing, applicability for maintaining Books of Accounts and the applicability of tax audit on F&O transactions. This guide provides an in-depth analysis based on the latest provisions under the Income Tax Act, 1961.

Understanding Trading Transactions for Taxation

Trading in stocks or F&O can be broadly classified into two categories:

Speculative Business Transactions

Non-Speculative Transactions (F&O Trading)

1. Speculative Transactions:

As per Section 43(5) of the Income Tax Act, a speculative transaction is one where the purchase and sale of stocks or commodities are settled without actual delivery. Intraday trading in equities falls under this category.

2. Non-Speculative Transactions (F&O Trading):

F&O trading, including commodity derivatives on recognized stock exchanges, is treated as non-speculative business income even though no physical delivery takes place.

Applicability of Tax Audit for F&O Trading

Since F&O trading is considered business income, tax audit provisions under Section 44AB apply similarly to any other business income. Understanding the turnover limits and profit declaration rules is crucial for compliance.

When is Tax Audit Mandatory?

Tax audit under Section 44AB is applicable in the following cases:

Turnover up to Rs. 1 crore:

Tax audit is not required, regardless of profit or loss, provided Section 44AD(4) does not apply.

Turnover exceeding Rs. 1 crore but up to Rs. 10 crore:

Tax audit is not required if at least 95% of transactions are digital.

Tax audit is mandatory if cash transactions exceed 5% of total receipts or 5% of total payments.

Please Note Receipts and payments are calculated separately, not cumulatively.

Turnover above Rs. 10 crore:

Tax audit is mandatory, irrespective of profit or loss.

Presumptive Taxation (Section 44AD) and Tax Audit:

If a taxpayer opts for Section 44AD, no tax audit is required for turnover up to Rs. 3 crore from Financial Year 2023-24 (Assessment Year 2024-25).

However, if Section 44AD(4) applies, tax audit is required if the declared profit is less than 6% (digital) or 8% (cash) of turnover, and total income exceeds the basic exemption limit.

Tax Audit for Professionals Under Section 44ADA and F&O Traders

If a taxpayer is carrying on a profession eligible for presumptive taxation under Section 44ADA and simultaneously engaged in F&O trading, the tax audit requirement is determined separately for each activity:

For F&O trading, tax audit is applicable as per Section 44AB turnover limits discussed above.

For professionals under Section 44ADA, tax audit is applicable if gross receipts exceed Rs. 75 lakh from Financial Year 2023-24 (Assessment Year 2024-25).

If both activities are carried out simultaneously, each must be evaluated independently for tax audit applicability.

How to Calculate Turnover for F&O Trading?

Determining turnover for tax audit purposes is essential for accurate reporting. The method of turnover calculation varies based on the type of transaction:

Futures and Options (F&O) Trading: Turnover is calculated as the sum of absolute values of profits and losses from each squared-off trade during the financial year.

Options Trading: If an options contract is physically settled, the premium received on the sale is included in turnover computation.

Turnover Calculation as per ICAI Guidance Note: The calculation of turnover for tax audit purposes is guided by ICAI’s Guidance Note on Tax Audit. This method ensures uniformity in turnover computation and compliance with audit requirements.

Understanding the 5% Cash Transaction Clause Under Section 44AB

For businesses with turnover between Rs. 1 crore and Rs. 10 crore, tax audit is not required if cash receipts and cash payments do not exceed 5% of total transactions. This is computed separately as follows:

Aggregate of all cash receipts, including sales, should not exceed 5% of total receipts.

Aggregate of all cash payments, including expenses, should not exceed 5% of total payments.

If either of these conditions is violated, tax audit becomes mandatory.

Since turnover is below Rs. 1 crore, no tax audit is required unless Section 44AD(4) applies.

When is Books of Accounts Mandatory to maintain?

The Income Tax Act has specified the books of accounts that are required to be maintained for the purpose of Income Tax. These have been prescribed under section 44AA and Rule 6F.

In case business/profession is being carried out by the individual or HUF the limits are increased as under:

a. For Income – Limit is Rs. 2,50,000

b. For Turnover/Gross Receipt – Limit is Rs. 25,00,000

Tax Benefits on Losses in F&O Transactions

Losses incurred in Futures & Options (F&O) transactions can be set off against rental or interest income. Any unadjusted losses can be carried forward for up to eight years and offset against future business profits, including profits from F&O transactions.

Is Declaring F&O Loss in the Income Tax Return is Mandatory

Many taxpayers, particularly salaried individuals engaged in F&O trading, often fail to report these transactions in their income tax returns. This omission may occur due to ignorance, but it is crucial to note that reporting all sources of income is a legal requirement.

Brokers are mandated to report all security transaction details to the Income Tax Department by filing a Statement of Financial Transactions (SFT) annually. Non-disclosure of F&O transactions can attract scrutiny from the department, resulting in notices for non-compliance and potential penalties for failure to maintain books of accounts and non-filing of the required tax audit report along with the income tax return.

Notice Under Section 139(9) of the Income Tax Act (Defective Return)

Failure to furnish a Balance Sheet and Profit & Loss Account when required can lead to receiving a notice under Section 139(9) from the Centralized Processing Centre (CPC) of the Income Tax Department. The notice typically states:

“The assessee has claimed loss under the head ‘Profits and Gains of Business or Profession’; however, a Balance Sheet and Profit & Loss Account must be provided. If the assessee falls under Section 44AD/44AE/44ADA, the books of account must be audited if the income offered is below the prescribed limits as per the provisions of the Income Tax Act.”

While an audit is not mandatory if the turnover is below INR 1 crore, the income tax return must be duly filed with a complete Balance Sheet and Profit & Loss Account under Section 139 of the Income Tax Act.

Table in Glance:

Scenarios

Opted for 44AD

Declaring Profit

Remarks

1

Yes (Turnover is less than Rs. 2Cr.)

According to 44AD

Neither require to maintain books of accounts nor audit.

2

Yes (Turnover is less than Rs. 2Cr.)

Less than 8% or 6% as the case may be or declaring loss.

Require to maintain books of accounts and audit.

3

No (Turnover is less than limit given u/s 44AB)

Profit or loss whatever is the case.

No audit, maintain books of accounts if limit of 44AA is crossed.

4

No (Turnover is more than limit given u/s 44AB)

Profit or loss whatever is the case.

Audit and maintaining books of accounts is mandatory.

Note: In all the cases of loss audit is not mandatory. It depends case to case. But in general practice and to deal with future litigation this practice followed.

Disclaimer: This article is solely for educational purpose and cannot be construed as legal and professional opinion. It is based on the interpretation of the author and are not binding on any tax authority. Author is not responsible for any loss occurred to any person acting or refraining from acting as a result of any material in this article.

The Professional Tax Registration Certificate (PTRC) is a statutory requirement for employers in Maharashtra under the Maharashtra State Tax on Professions, Trades, Callings and Employments Act, 1975. PTRC pertains to the professional tax that an employer deducts from the salaries of employees and remits it to the Maharashtra Government.

Applicability

Every employer who has even one employee drawing a salary exceeding ₹7,500 per month (₹10,000 for women employees) is required to register under PTRC and deduct professional tax from employee salaries. The employer must deposit this tax with the Maharashtra State Government. Separate PTRC registrations are required for each branch office if located in different jurisdictions.

PTRC Slab Rates (FY 2024-25)

The slab rates for PTRC deduction in Maharashtra are as follows: – Salary up to ₹7,500 per month (₹10,000 for women): Nil – Salary between ₹7,501 and ₹10,000: ₹175 per month – Salary above ₹10,000: ₹200 per month (except ₹300 in February) The total annual liability per employee cannot exceed ₹2,500.

Registration Process

Employers must register online through the Maharashtra Goods and Services Tax (MGST) portal at https://mahagst.gov.in. Under the e-Services section, they should choose ‘New Registration’ and select ‘PTRC’. Form I must be filled out with employer and employee details. Required documents typically include PAN, Aadhaar, address proof, and salary structure. Upon submission, the PTRC number is usually issued within 1 working day.

Payment and Return Filing

Employers must file returns and make payments on the MGST portal. The return Form IIIB is auto-generated upon payment. Filing frequency depends on the tax liability in the previous financial year: – Monthly: If liability > ₹1,00,000 – Quarterly: If liability ≤ ₹1,00,000 – Annual: For employers registered after 31 March 2020 with monthly tax liability of ₹2,500 Due dates are the 30th of the following month for monthly/quarterly returns and 31st March for annual returns.

Penalties and Interest for Non-Compliance

Failure to register, deduct, or pay PTRC can result in interest and penalties. Interest is charged at 1.25% per month for delays. Late filing of returns attracts a penalty of ₹1,000 per return. Non-registration or non-payment can lead to penalties up to the amount of tax due, along with possible prosecution.

Difference Between PTRC and PTEC

PTRC is related to the tax deducted by an employer from employees, whereas PTEC (Professional Tax Enrollment Certificate) is applicable to individual professionals, proprietors, and business owners, who must pay professional tax on their own behalf. Many businesses require both PTRC and PTEC registrations.

PTRC compliance is crucial for all employers in Maharashtra to ensure legal compliance and avoid penalties. Timely registration, accurate deduction, and proper return filing are essential. Employers are encouraged to integrate professional tax compliance into their payroll processes or seek assistance from professionals for smooth operations.

Disclaimer: This article is solely for educational purpose and cannot be construed as legal and professional opinion. It is based on the interpretation of the author and are not binding on any tax authority. Author is not responsible for any loss occurred to any person acting or refraining from acting as a result of any material in this article.

The new section 43B(h) will be applicable from April 1, 2024 (AY 2024-25), Section 43B(h) of the Income Tax Act introduces significant changes concerning expenses related to purchases or services from Micro and Small Enterprises. Please note this section is not applicable on Medium Enterprises.

43B(h) has been inserted as a Socio-Economic Welfare Measure to ensure timely payments to micro and small enterprises.

We all know that section Section 43B of the Act provides for certain deductions to be allowed only on Actual Payment basis.

Finance Bill 2023 has newly inserted a clause to this section which is as under:

Section 43B (h) of Income Tax Act says:

“any sum payable by the assessee to a MICRO or SMALL enterprise beyond the time limit specified in 15 of the Micro, Small and Medium Enterprises Development Act, 2006,”

The above clause indicated that, in order to be eligible to claim deduction of the sum payable to micro and small enterprises, the payment shall be actually made within the time limit specified in 15 of the MSME Act, 2006.

Section 15 of MSME Development Act, 2006 says:

“Where any supplier supplies any goods or renders any services to any buyer, the buyer shall make payment therefor on or before the date agreed upon between him and the supplier in writing or, where there is no agreement in this behalf, before the appointed day*:

Provided that in no case the period agreed upon between the supplier and the buyer in writing shall not exceed forty-five days from the day of acceptance or the day of deemed acceptance”

It is very clear that, the buyer shall make the payment to the supplier as agreed between them, however the same cannot exceed beyond 45 days from date of acceptance or the day of deemed acceptance i.e., from the day of acceptance of the goods/service.

Section 2(b) of the MSME Development Act, 2006 says:

“Appointed Day” means the day following immediately after the expiry of the period of fifteen (15) days from the day of acceptance or the day of deemed acceptance of any goods or any services by a buyer from a supplier.

Explanation—For the purposes of this clause-

(i) “the day of acceptance” means-

(a) the day of the actual delivery of goods or the rendering of services; or

(b) where any objection is made in writing by the buyer regarding acceptance of goods or services within fifteen days from the day of the delivery of goods or the rendering of services, the day on which such objection is removed by the supplier;

(ii) “the day of deemed acceptance” means, where no objection is made in writing by the buyer regarding acceptance of goods or services within fifteen days from the day of the delivery of goods or the rendering of services, the day of the actual delivery of goods or the rendering of services;

Section 16 of MSME Development Act, 2006 says:

“Where any buyer fails to make payment of the amount to the supplier, as required under section 15, the buyer shall, notwithstanding anything contained in any agreement between the buyer and the supplier or in any law for the time being in force, be liable to pay compound interest with monthly rests to the supplier on that amount from the appointed day or, as the case may be, from the date immediately following the date agreed upon, at three times of the bank rate notified by the Reserve Bank”

Consequences upon Failure to make payment to Micro and Small Enterprises under Section 43B(h)

If the payment is made after 45 days or 15 days as specified – then expenses disallowed in the year and deduction will be available in the year in which the payment is made.

If the payment is due for more than 45 days or 15 days as specified but the payment is made before the end of the Financial Year – then in such case, the deduction of the expense will be available in the same year itself.

The classification of the enterprise as Micro, Small & Medium as defined in Micro, Small and Medium Enterprises Development Act, 2006 is hereby produced for your reference:

Clause 44 It was added w.e.f 20th August 2018 but Reporting under this clause was deferred till 31st March 2019 vide Circular No. 6/2018 dated 17th August 2018, So reporting in clause 44 is started from AY 2019-20.

TheObjective for insertion of this Clause 44:

The main objective is to co-relate GST Data with Income Tax Data.

FAQ’s on CLAUSE 44

Q.1. Is reporting in this clause applicable only for Assessee who are GST registered?

Ans: No, Reporting is to be made by all assesses who are registered under GST or not.

Q.2. Interpretation of wordings “Breakup of total expenditure”? What expenditures are not Included?

Ans: Interpretation should be “broader” with reference to Capital Expenditure as well as Revenue Expenditure including Purchases.

But activities or transactions which those neither as a supply of goods nor a supply of services and thus expenditure incurred in respect of such activities need not be reported under this clause.

1. Salary not Included

2. Depreciation under section 32, deduction for bad debts u/s 36(1)(vii) etc. which are not expenses should not be reported under this clause.

3. Bad Debts written off etc.,

So we can say any expenditure that is incurred, wholly and exclusively for the business or profession of the assessee qualifies for the deduction under the Act.

Q.3. Tabular format for disclosure:

Sl. No.

Total amount of Expenditure incurred during the year

Relating to Goods or services Exempt from GST

Relating to entities Falling under Composition Scheme

Relating to Other Registered Entities

Total Payment to Registered Entities

Expenditure relating to entities not registered under GST

(1)

(2)

(3)

(4)

(5)

(6)

(7)

The format as per clause 44 of form 3CD requires that the information is to be given as per the following details:

A. Total amount of expenditure incurred during the year

B. Expenditure in respect of entities registered under GST

C. Expenditure related to entities not registered under GST

the expenditure in respect of entities registered under GST is further sub-classified into four categories as follows:

a) Expenditure relating to goods or services exempt from GST

b) Expenditure relating to entities falling under the composition scheme

c) Expenditure relating to other registered entities

d) Total payment to registered entities

Q.4. Colum 2 says “Total amount of Expenditure incurred during the year” so shall we report head-wise / nature wise expenditure?

Ans: The heading of the table which starts with the words “Breakup of total expenditure” and hence the total expenditure including purchases as per the above format may be given. It appears that head-wise / nature wise expenditure details are not envisaged in this clause.

However, it is recommended to take head wise/nature wise expenditure details as a part of working paper of the Audit.

Q.5. What are the Expenditure relating to other registered entities (column 5)?

Ans: The value of all inward supplies from registered dealers, other than supplies from composition dealers and exempt supply from registered dealers, are to be mentioned in this column.

Q.6. What is the meaning of “Total payment to registered entities (column 6)”?

Ans: The language used in sub-heading of column 6 is total’ payment’ to registered entities. The word ‘payment’ should harmoniously be interpreted as ‘expenditure’ as the combined heading of columns (3), (4), (5) is ‘Expenditure in respect of entities registered under GST’. Hence, the total expenditure in respect of registered entities i.e., sum total of values reported in columns (3), (4) and (5) should be reported in Column 6.

Q.7. Checks and Control while reporting?

Ans: There are some checks and control so auditor make sure on correctness on reporting.

Amount of Serial number 2 is equal to amount of serial number 6 PLUS Serial number 7.

Amount of Serial number 6 is equal to amount of serial number 3 PLUS Serial number 4 PLUS Serial number 5.

Total Value of Expenditure in P & L for the year

XXX

Add: Total Value Capital Expenditure Not Included in P & L

XXX

Less: Total Value Of non-cash Charges considered as expenditure

XXX

Less: Total Value of Expenditure Excluded For being Transactions in securities and Transactions In money

XXX

Less: Total value Of Expenditure Excluded by virtue of Schedule III to the CGST Act,2017

The Foreign Currency Exposure is a risk associated with the businesses and investors engaged in the activities (trade and investments) of dealing in foreign currency transactions. The entities involved in the activities of transactions in different foreign currency denominations and does not take steps to protect themselves from currency fluctuations.

This exposure arises when a company or individual holds assets, liabilities, or cash flows in a foreign currency without implementing any hedging mechanisms to mitigate potential adverse currency fluctuation.

Entities needs to hedge ourselves from foreign currency exposure in the market to avoid any risk of volatility in the exchange rates and Derivative hedging is the one of the best ways to hedge.

Unhedged foreign currency exposure (UFCE):

The RBI issues guidelines for banks to manage their foreign currency exposure either fund base or non-fund base, in an attempt to reduce the risk of unhedged exposure on the banking system during extreme volatility in forex markets.

Banks would be required to assess the unhedged foreign currency exposures of all entities to whom they have an exposure in any currency.

Accordingly, the banks were given advisory through the issuance of various directions, guidelines and circulars to develop a framework for regular monitoring of entities that do not have a hedge. Henceforth, the present directions dated 11th October 2022

Applicability of the Directions:

The provision pertaining to the current directions shall apply to all commercial Banks excluding Payments Bank and Regional Rural Banks along with the Overseas Branches and Subsidiaries of Banks incorporated in India.

These Directions shall come into effect from January 1, 2023.

Computation of UFCE:

Banks shall ascertain the Foreign Currency Exposure (FCE) of all entities at least on an annual basis. Banks shall compute the FCE following the relevant accounting standard applicable for the entity. For ascertaining the Foreign Currency Exposer, the banks shall also include all the sources of an entity’s exposure, including Foreign Currency Borrowings & External Commercial Borrowings.

UFCE shall be obtained from entities on a quarterly basis based on statutory audit, internal audit or self-declaration by the concerned entity. Moreover UFCE information shall be audited and certified by the statutory auditors of the entity, at least on an annual basis.

Provisioning and Capital Requirements:

The bank is required to calculate the total potential loss to the entity from Unhedged Foreign Currency Exposure. It shall be determined by using the data published by FEDAI on the annual volatility rate in the USD-INR exchange rate for the last 10 years and multiplying it with the UFCE of an entity.

The bank is required to ascertain the susceptibility of an entity towards adverse exchange rate movements. It shall be determined by computing the ratio of potential loss to the entity from UFCE and the entity EBID (Earnings before interest and depreciation).

In case if the bank is unable to gather information on UFCE and EBID of an entity due to restrictions on disclosure of information, then, in that case, the bank can compute the susceptibility ratio by using data that is immediately preceding the last four quarters.

In case of Unlisted Company if the information on EBID and UFCE is not available due to the non-availability of the last audited results of the last quarter, then, in that case, the bank shall undertake the latest quarterly and annual result. However, the EBID figure shall be for the last financial year.

The direction has determined the figure for computing the incremental provisioning and capital requirements which are as follows:

Potential Loss or EBID ( in Percentage)

Incremental provisioning Requirements

Incremental Capital Requirements

Up to 15 %

0

0

15% to 30%

20 BPS

0

30% to 50%

40 BPS

0

50% to 75%

60 BPS

0

More than 75%

80 BPS

Risk weight + 25%

Further, the bank is required to calculate the incremental requirements on quarterly basis.

For projects under implementation and the new entities, banks shall calculate the incremental provisioning and capital requirements based on projected average annual EBID for the three years from the date of commencement of commercial operations.

In the case of consortium arrangements, the consortium leader / bank having the largest exposure shall have the lead role in monitoring the unhedged foreign exchange exposure of entities.

Exemption / Relaxation (a) Banks shall have the option to exclude the following exposures from the calculation of UFCE:

(i) Exposures to entities classified as sovereign, banks and individuals.

(ii) Exposures classified as Non-Performing Assets.

(iii) Intra-group foreign currency exposures of Multinational Corporations (MNCs) incorporated outside India.

Provided that the bank is satisfied that such foreign currency exposures are appropriately hedged or managed robustly by the parent. (iv) Exposures arising from derivative transactions and / or factoring transactions with entities, provided such entities have no other exposures to banks in India.

Assessment of Unhedged Foreign Currency Exposure (UFCE):

The banks are further required to ascertain the UFCE by obtaining such information from the concerned entity on quarterly basis. Further, the information on UFCE supplied to the bank must be audited and certified by a statutory auditor of the entity.

The Securities and Exchange Board of India (SEBI) on Tuesday, 20th December,2022 amended the buyback rules to gradually phase out the Open Market Route in favor of the Tender Route. SEBI has improvised the present share buyback norms for listed companies and has tightened the disclosure rules to increase the transparency and credibility of the market.

Over a period, buyback regulations have also evolved with the growth and complexity of the market. Initially, buyback was allowed only from the open market through stock exchanges. Subsequently, the tender method for buyback was also introduced. It was felt that the stock exchange route is less efficient as it may be difficult to buyback through this route the full quantity without affecting the share price. Also, it may take a long time to complete it. Further, there is a possibility of one shareholder’s entire trade getting matched with the purchase order placed by the company, thus depriving other shareholders to avail the benefit of the buyback. Therefore, a time-bound program under the tender route was considered a superior method.

Few of the major changes made by SEBI are:

Increase in the limit of utilization of proceeds:

The regulator has amended the rules on the way of using of the funds which are kept for buyback. The buyback norms at present require companies to utilize at least 50 per cent of the amount earmarked for this purpose. On Tuesday, SEBI has raised the minimum threshold of 50 per cent to 75 per cent for the purpose of utilization. In case of failure to use the minimum proceeds by the company, SEBI can direct the merchant banker to forfeit the amount deposited in an Escrow account.

Reduction in time for the process of buyback:

In buyback under the Tender route, SEBI has reduced the timeline for completion by 18 days. It has dropped the requirement to file the draft letter of offer.

Advertisement for buyback to increase awareness/knowledge:

SEBI has made it mandatory to place the relevant advertisements/ documents with respect to buyback, such as, copy of the public announcement, letter of offer etc. on the respective website of the stock exchange(s), merchant banker and the company for better dissemination of information to shareholders.

Revision of price for Buyback:

SEBI has permitted the upward revision of the buyback price until one working day prior to the record date.

Additional Points:

SEBI has also decided to create a separate window on stock exchanges for undertaking buyback till the time tender offers are fully in effect.

SEBI has proposed to reduce the timeline for completion of process of buyback to 66 days with effect from 1st April, 2023 and to 22 working days from 1st April, 2024.

It has also been proposed that Open Market Route will be completely closed by 1st April, 2025.

These amendments aim to streamline the process of buyback, create a level-playing field for investors and promote the ease of doing business. We hope that the new regime to choose tender route for buyback with a shorter timeline and ability to revise the price upwards until the late stage will make the buy-back scheme much more robust, market friendly as well as investor friendly.

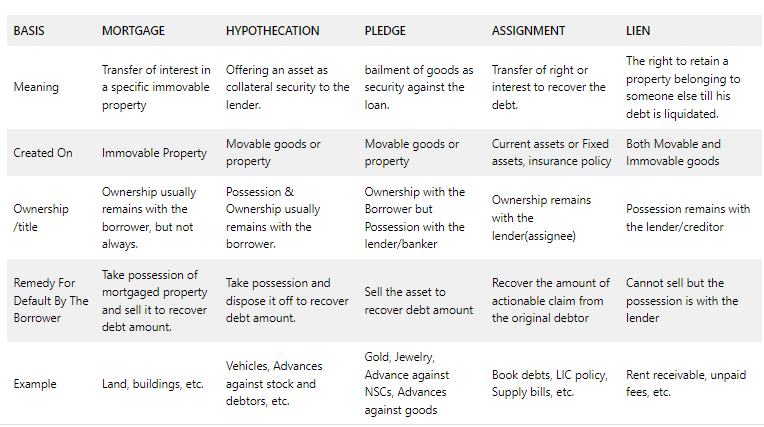

Companies Act, 2013 defines “charge” as an interest or lien created on the property or assets of a company or any of its undertakings or both as security and includes a mortgage. There are various forms of creation of charge. Some of the terms used of creation of charge are: Mortgage, Hypothecation, Pledge, etc. Although these terms are used interchangeably many times, there is different meaning attached to these words. So in this article, you will be able to understand each of the terms separately which are used in the contracts.

MORTGAGE:

A mortgage is one of the ways to create charge against immovable property where the amounts involved are generally very high, and the transfer of title is often passed. Mortgage is the transfer of interest in a specific immovable property in order to secure an existing or future debt.

The legal ownership of the asset can be transferred to the lender under mortgage if the borrower defaults on the repayment of the loan amount. However, the borrower continues to remain in possession of the property.

A mortgage is usually used for immovable assets which are permanently fixed to the earth or attached to the land like house, land, building, or any property, etc. Home loans are classified as mortgages.

The person creating the mortgage is called as Mortgagor while the person in whose favor mortgage is created (usually Banks) is called as Mortgagee.

PLEDGE:

Pledge is the bailment of goods as a security for payment of debt or performance of a promise. Bailment means delivery of goods with some purpose and with the condition that when the purpose is accomplished, the goods will be delivered back to the Bailor. Pledge is a contract between the lender and borrower, where the borrower pledges an asset as a security to the lender. Under Pledge, the ownership of the asset remains with the borrower, however, the possession of the asset is transferred to the Banker/Pledgee.

Pledge can be charged only on movable goods like stocks. The bank shall take care of the possession in good faith and as the same as its own goods.

In case of default by the borrower, the bank has a right to sell the goods in his possession with any intervention of the court and recover the amount due.

If there is any surplus while selling the asset, the amount is returned back to the pledger (borrower).

The asset can only be sold by the pledgee after giving reasonable reminder and notice to the pledgor(borrower).

In case of pledge, risk of lending comparatively reduces because possession of assets is with the lender.

Some examples of pledge are gold /jewelry loans, advance against goods or stock, advances against National Saving Certificates etc.

HYPOTHECATION:

Hypothecation is another way of creating a charge but against movable assets. Hypothecation means offering an asset as collateral security to the lender. The borrower enjoys both the ownership as well as the possession.

In the case of any default by the borrower, the lender can take the possession of the security and exercise his right to seize the asset and sell the asset to recover the dues.

The charge created under hypothecation is Equitable Charge (where there is no variation).

But in case of hypothecation of stocks to the bank, the charge which is created is called floating charge.

The common example for hypothecation is car loans. In car or vehicle loans, it remains with the borrower but the same is hypothecated to the bank or financer. If the borrower defaults, the bank then takes the possession of the car after providing sufficient notice to recover the money.

Sometimes when a bank or financial institution puts the already pledged asset as collateral for borrowing from another bank, it is called re-hypothecation.

ASSIGNMENT:

An assignment is another type of charge on current assets or fixed assets. Under assignment, the charge is created on the assets held in the books. Assignment refers to the transfer of right or interest to recover the debt.

The transferor of the claim is called as the Assignor (Borrower) and the transferee is called the Assignee (Bank).

Assignor cannot give better title to the assignee than what assignor has.

In case of default, the assignee, i.e., the bank can recover the amount of actionable claim from the original debtor without reference to the Assignor.

Assignment is possible through writing only.

Assignment can be of two types: Legal and Equitable Assignment. Legal Assignment is the agreement where all the legal formalities are done on stamp paper while in case of equitable assignment, all the formalities are written on the paper but the legal element is missing from this.

Examples of assignments include life insurance policies, books of debts, receivables, etc., which the bank can finance. For example – A bank can finance against the book debts. The borrower assigns the book debts to the bank in such a case.

LIEN:

The right to retain a property belonging to someone else till his debt is liquidated is called as Lien. Under a lien, the lender gets the right to hold up the asset used as collateral against the funds borrowed. However, unless the contract states otherwise, if the borrower defaults on the loan, the lender doesn’t have the right to sell the property.

Example: A piece of cloth is given to a tailor to stitch a suit. After the suit is made, the tailor has the right to retain it as security with him till he is paid the stitching charge by the person who placed the order for the suit. Once the payment is received, the tailor is bound to give the suit to the person concerned.

It is a right given to the creditor to retain/possess the security until the loan amount is paid. It is the strongest form of security since possession of the security is with the creditor.

Lien can be on both movable and immovable property.

But generally, lending companies choose to have mortgages on immovable property and lien on movable security like shares, gold, deposits, etc.

Examples of lien include rent receivable, unpaid fees, etc.

SET-OFF

A settlement of mutual debt between a creditor and a debtor through offsetting transaction claims is also known as setoff. In order to cover a loan in default, a bank has a legal right to seize funds of a guarantor or the debtor. The right of set-off enables the bank to combine two accounts (a loan account and a deposit account) of the same person. Through this settlement, a creditor can collect a greater amount than they usually could under bankruptcy proceedings. When a setoff clause is entered into, the bank can seize the customer’s current deposit. For purposes of set-off, all bank branches are treated as one single entity. A bank exercising a right of setoff must fulfill the following conditions:

the account from which the firm transfers funds must be held by the customer owing the firm money;

the account from which the firm transfers the money and the account from which the money would otherwise have come, must be held with the same firm;

both the accounts must be held in the same capacity by the customer;

COMPANIES (INCORPORATION) THIRD AMENDMENT RULES, 2022

Companies (Incorporation) Third Amendment Rules, 2022 has been notified on 18th August 2022 by Ministry of Corporate Affairs (MCA) to further amend the Companies (Incorporation) Rules, 2014. In this amendment, MCA has introduced a new Rule 25B, which is about Physical verification of the registered Office of the Company. However, this new Rule will come into effect once notified in the Official Gazette.

OVERVIEW OF RULE 25B

Earlier, as per Section 12 of the Companies Act 2013, physical verification of the company’s registered office was required only when ROC have reasonable grounds to believe that the company concerned is not carrying on a business. However, after the amendment in the Companies (Incorporation) Third Amendment Rules, 2022, physical verification has been implemented as per Rule 25B.

After Rule 25A (Active Company Tagging Identities and Verification), MCA has inserted new Rule 25B (Physical verification of the Registered Office of the company).

Companies (Incorporation) Third Amendment Rules, 2022 has been introduced by the government to ensure a more transparent process for the physical verification of companies’ registered addresses. According to the new Rule 25B, the Registrar of Companies (ROC), based upon the information made available on MCA 21 portal, shall visit the Address of the Registered Office of the company and do the physical verification of the Registered Office of the company.

As per the new rule 25B, ROC will carry out a physical verification of the location of the Registered Office of the company in the presence of two independent witnesses.

The Registrar shall carry the documents filed on the MCA 21 portal in support of the Address of the company’s registered office for physical verification.

To check the authenticity and validity of the documents as well as the office, the same shall be cross-verified with the copies of supporting documents of such Address collected during the physical check, duly authenticated from the occupant of the property where the Registered Office is situated.

The Registrar will also need to have a photograph of the company’s registered Office for proof during the physical verification.

If required, RoC will also seek assistance from the local police.

After conducting the verification process, a detailed report shall be prepared including all the information such as location details and photographs.

REGISTERED OFFICE OF A COMPANY

The company’s Registered Office is the main Office of the Company at which all the communication relating to the company are sent by the governmental departments. Company’s Registered Office shall be declared during company incorporation/LLP incorporation by the Directors of the company/LLP and they shall maintain all the required documents at the registered Office.

Registrar of Company (ROC) will be determined by the state or location where the Registered Office of the Company is situated.

Any change in the Company’s address/location of the Registered Office must notify the Registrar of Company (ROC) within a specified period of time.

REPORT ON PHYSICAL VERIFICATION OF COMPANIES REGISTERED OFFICE

Verification Report of the Registered Office of the company will be prepared by RoC in the given format.

Name and Company Identification Number (CIN) of the company

Latest Address of the company as per the MCA 21 records

Date of authorization letter issued by the Registrar of Companies

Name of Registrar of Companies

Date and Time of Physical verification

Location Details of Company along with the landmark

Details of person available at the time of Physical verification

Along with these details, ROC will also have to attach the following documents with the report:

Copy of agreement/ownership /rent agreement/No objection certificate (NOC) of the registered Office of the company from owner/tenant/lessor

Photograph of the Registered Office

Self-Attested ID card of the person available

NOTICE TO COMPANY AND DIRECTORS

Suppose the Registered Office is unable to receive and acknowledge all notices due to its location or any other issue. In that case, the ROC will notify the Company and all Directors of the intention to remove the company’s name from the official Register of Companies (ROC) by the way of show-cause notice and request them to send their reply along with the required documents.

The Director of the company needs to send their reply against the show-cause notice along with the necessary documents within 30 days from the date of the notice by the MCA; otherwise, ROC will have to take further action under section 248 of the Companies Act.