Gold is one of the most preferred investment options in India, available in multiple forms such as physical gold, Gold ETFs, Sovereign Gold Bonds (SGBs), digital gold, and gold mutual funds. Each form has a different tax treatment under the Income-tax Act. This article explains the taxation on sale of gold in a simple and professional manner.

1. Physical Gold (Jewellery, Coins & Bars)

Physical gold includes jewellery, coins, and bars. Tax is applicable at the time of sale based on the holding period.

• Short-Term Capital Gain (STCG): If sold within 24 months, gains are taxed as per the individual’s income tax slab. • Long-Term Capital Gain (LTCG): If held for more than 24 months, gains are taxed at 12.5% without indexation. • GST paid at the time of purchase is not refundable and forms part of the cost.

2. Gold Exchange Traded Funds (ETFs)

Gold ETFs are paper gold investments traded on stock exchanges and backed by physical gold.

• STCG: Units sold within 12 months are taxed as per income tax slab rates. • LTCG: Units sold after 12 months are taxed at 12.5% without indexation.

3. Sovereign Gold Bonds (SGBs)

Sovereign Gold Bonds are issued by the RBI on behalf of the Government of India and are considered the most tax-efficient form of gold investment.

• If held till maturity (8 years): Capital gains are completely tax-free. • If sold on stock exchange: – Within 12 months: Taxed at slab rates. – After 12 months: Taxed at 12.5% without indexation. • Interest earned (around 2.5% annually) is taxable as per slab rates.

Amendment in Finance Bill, 2026 “exemption will be applicable only to those Sovereign Gold Bonds issued by the Reserve Bank of India that are subscribed to by an individual at the time of original issue and are held continuously by such individual until redemption upon maturity” it means Capital gains exemption does not apply if bought from secondary market.

4. Digital Gold & Gold Mutual Funds

Digital gold and gold mutual funds offer convenience and flexibility but follow similar tax rules.

• STCG: If sold within 24 months, gains are taxed as per income tax slab. • LTCG: If sold after 24 months, gains are taxed at 12.5% without indexation.

Conclusion:

From a tax perspective, Sovereign Gold Bonds are the most efficient option for long-term investors, while Gold ETFs and mutual funds provide liquidity with moderate taxation. Physical gold, though culturally significant, is the least tax-efficient due to GST and higher holding period requirements.

In Tabular Format

Investment type

Short-term capital gains (STCG)

Long-term capital gains (LTCG)

Notes

Sovereign Gold Bonds (SGBs)

If sold within 12 months: taxed at slab rate

If held beyond 12 months and sold before maturity: 12.5% without indexation; Nil if held till 8-year maturity

Capital gains exemption does not apply if bought from secondary market

Gold ETFs

Up to 12 months: taxed at slab rate

Beyond 12 months: 12.5% without indexation

Treated as listed securities

Gold mutual funds

Up to 24 months: taxed at slab rate

Beyond 24 months: 12.5%

Usually invest in gold ETFs

Physical gold

Up to 24 months: taxed at slab rate

Beyond 24 months: 12.5%

GST paid cannot be set off against capital gains tax

Gifted gold

Taxable only if gift from non-relatives exceeds ₹50,000

Taxable in the recipient’s hands

Gifts from specified relatives are tax-free

Inherited gold

Capital gains apply on sale

Capital gains apply on sale

Original owner’s cost and holding period are considered

Salaried individuals who engage in stock trading or Futures & Options (F&O) transactions often have queries about income tax return filing, applicability for maintaining Books of Accounts and the applicability of tax audit on F&O transactions. This guide provides an in-depth analysis based on the latest provisions under the Income Tax Act, 1961.

Understanding Trading Transactions for Taxation

Trading in stocks or F&O can be broadly classified into two categories:

Speculative Business Transactions

Non-Speculative Transactions (F&O Trading)

1. Speculative Transactions:

As per Section 43(5) of the Income Tax Act, a speculative transaction is one where the purchase and sale of stocks or commodities are settled without actual delivery. Intraday trading in equities falls under this category.

2. Non-Speculative Transactions (F&O Trading):

F&O trading, including commodity derivatives on recognized stock exchanges, is treated as non-speculative business income even though no physical delivery takes place.

Applicability of Tax Audit for F&O Trading

Since F&O trading is considered business income, tax audit provisions under Section 44AB apply similarly to any other business income. Understanding the turnover limits and profit declaration rules is crucial for compliance.

When is Tax Audit Mandatory?

Tax audit under Section 44AB is applicable in the following cases:

Turnover up to Rs. 1 crore:

Tax audit is not required, regardless of profit or loss, provided Section 44AD(4) does not apply.

Turnover exceeding Rs. 1 crore but up to Rs. 10 crore:

Tax audit is not required if at least 95% of transactions are digital.

Tax audit is mandatory if cash transactions exceed 5% of total receipts or 5% of total payments.

Please Note Receipts and payments are calculated separately, not cumulatively.

Turnover above Rs. 10 crore:

Tax audit is mandatory, irrespective of profit or loss.

Presumptive Taxation (Section 44AD) and Tax Audit:

If a taxpayer opts for Section 44AD, no tax audit is required for turnover up to Rs. 3 crore from Financial Year 2023-24 (Assessment Year 2024-25).

However, if Section 44AD(4) applies, tax audit is required if the declared profit is less than 6% (digital) or 8% (cash) of turnover, and total income exceeds the basic exemption limit.

Tax Audit for Professionals Under Section 44ADA and F&O Traders

If a taxpayer is carrying on a profession eligible for presumptive taxation under Section 44ADA and simultaneously engaged in F&O trading, the tax audit requirement is determined separately for each activity:

For F&O trading, tax audit is applicable as per Section 44AB turnover limits discussed above.

For professionals under Section 44ADA, tax audit is applicable if gross receipts exceed Rs. 75 lakh from Financial Year 2023-24 (Assessment Year 2024-25).

If both activities are carried out simultaneously, each must be evaluated independently for tax audit applicability.

How to Calculate Turnover for F&O Trading?

Determining turnover for tax audit purposes is essential for accurate reporting. The method of turnover calculation varies based on the type of transaction:

Futures and Options (F&O) Trading: Turnover is calculated as the sum of absolute values of profits and losses from each squared-off trade during the financial year.

Options Trading: If an options contract is physically settled, the premium received on the sale is included in turnover computation.

Turnover Calculation as per ICAI Guidance Note: The calculation of turnover for tax audit purposes is guided by ICAI’s Guidance Note on Tax Audit. This method ensures uniformity in turnover computation and compliance with audit requirements.

Understanding the 5% Cash Transaction Clause Under Section 44AB

For businesses with turnover between Rs. 1 crore and Rs. 10 crore, tax audit is not required if cash receipts and cash payments do not exceed 5% of total transactions. This is computed separately as follows:

Aggregate of all cash receipts, including sales, should not exceed 5% of total receipts.

Aggregate of all cash payments, including expenses, should not exceed 5% of total payments.

If either of these conditions is violated, tax audit becomes mandatory.

Since turnover is below Rs. 1 crore, no tax audit is required unless Section 44AD(4) applies.

When is Books of Accounts Mandatory to maintain?

The Income Tax Act has specified the books of accounts that are required to be maintained for the purpose of Income Tax. These have been prescribed under section 44AA and Rule 6F.

In case business/profession is being carried out by the individual or HUF the limits are increased as under:

a. For Income – Limit is Rs. 2,50,000

b. For Turnover/Gross Receipt – Limit is Rs. 25,00,000

Tax Benefits on Losses in F&O Transactions

Losses incurred in Futures & Options (F&O) transactions can be set off against rental or interest income. Any unadjusted losses can be carried forward for up to eight years and offset against future business profits, including profits from F&O transactions.

Is Declaring F&O Loss in the Income Tax Return is Mandatory

Many taxpayers, particularly salaried individuals engaged in F&O trading, often fail to report these transactions in their income tax returns. This omission may occur due to ignorance, but it is crucial to note that reporting all sources of income is a legal requirement.

Brokers are mandated to report all security transaction details to the Income Tax Department by filing a Statement of Financial Transactions (SFT) annually. Non-disclosure of F&O transactions can attract scrutiny from the department, resulting in notices for non-compliance and potential penalties for failure to maintain books of accounts and non-filing of the required tax audit report along with the income tax return.

Notice Under Section 139(9) of the Income Tax Act (Defective Return)

Failure to furnish a Balance Sheet and Profit & Loss Account when required can lead to receiving a notice under Section 139(9) from the Centralized Processing Centre (CPC) of the Income Tax Department. The notice typically states:

“The assessee has claimed loss under the head ‘Profits and Gains of Business or Profession’; however, a Balance Sheet and Profit & Loss Account must be provided. If the assessee falls under Section 44AD/44AE/44ADA, the books of account must be audited if the income offered is below the prescribed limits as per the provisions of the Income Tax Act.”

While an audit is not mandatory if the turnover is below INR 1 crore, the income tax return must be duly filed with a complete Balance Sheet and Profit & Loss Account under Section 139 of the Income Tax Act.

Table in Glance:

Scenarios

Opted for 44AD

Declaring Profit

Remarks

1

Yes (Turnover is less than Rs. 2Cr.)

According to 44AD

Neither require to maintain books of accounts nor audit.

2

Yes (Turnover is less than Rs. 2Cr.)

Less than 8% or 6% as the case may be or declaring loss.

Require to maintain books of accounts and audit.

3

No (Turnover is less than limit given u/s 44AB)

Profit or loss whatever is the case.

No audit, maintain books of accounts if limit of 44AA is crossed.

4

No (Turnover is more than limit given u/s 44AB)

Profit or loss whatever is the case.

Audit and maintaining books of accounts is mandatory.

Note: In all the cases of loss audit is not mandatory. It depends case to case. But in general practice and to deal with future litigation this practice followed.

Disclaimer: This article is solely for educational purpose and cannot be construed as legal and professional opinion. It is based on the interpretation of the author and are not binding on any tax authority. Author is not responsible for any loss occurred to any person acting or refraining from acting as a result of any material in this article.

Form 10-IEA is required to fill by individuals or HUFs those want to continue with the old tax regime in the present financial year ie FY 2023-24. The Budget 2023 proposes that from FY 2023-24, the new tax regime will be considered the default tax regime. By filling Form 10-IEA, taxpayers can choose the old tax regime. They must file the form on or before the due date prescribed for filing an income tax return. Let’s start with the detailed analysis of Form 10-IEA and go through its important aspects.

What is Form 10-IEA

In FY 2022-23 the old tax regime was announced as the default tax regime. Those taxpayers willing to choose the New tax regime must have to file Form 10-IE electronically. But in FY 2023-24 the new tax regime was announced as the default tax regime. And now those taxpayers willing to choose the New tax regime must have to file Form 10-IEA electronically and this action make Form 10-IE which was earlier employed to opt for the new tax regime has now been discontinued

Purpose of Filing Form 10-IEA

let’s understand the purpose of Form 10IEA.

Individuals and HUF’s having income from profession/business must file Form 10-IEA by adhering to the prescribed deadline under Section 139(1). Please note this revised procedure streamlines the process, enabling individuals without business or professional income to directly specify their preference while filing a tax return by selecting the preferred option.

The corresponding choice determines the rules and regulations that would be applicable to the assessee.

Filling Form 10-IEA requires individuals to provide all the necessary information like PAN number, assessment year, name, and current status. These details can be used to accurately categorise and identify taxpayer information.

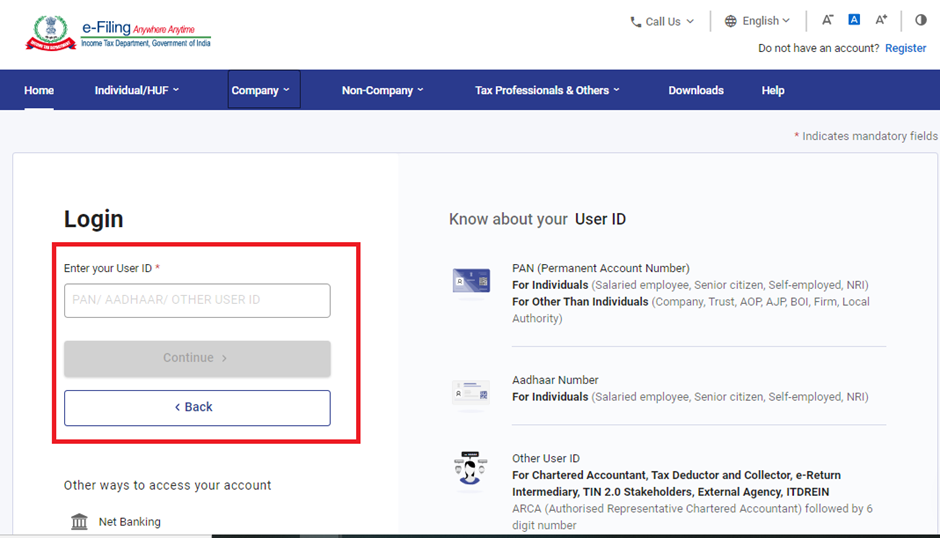

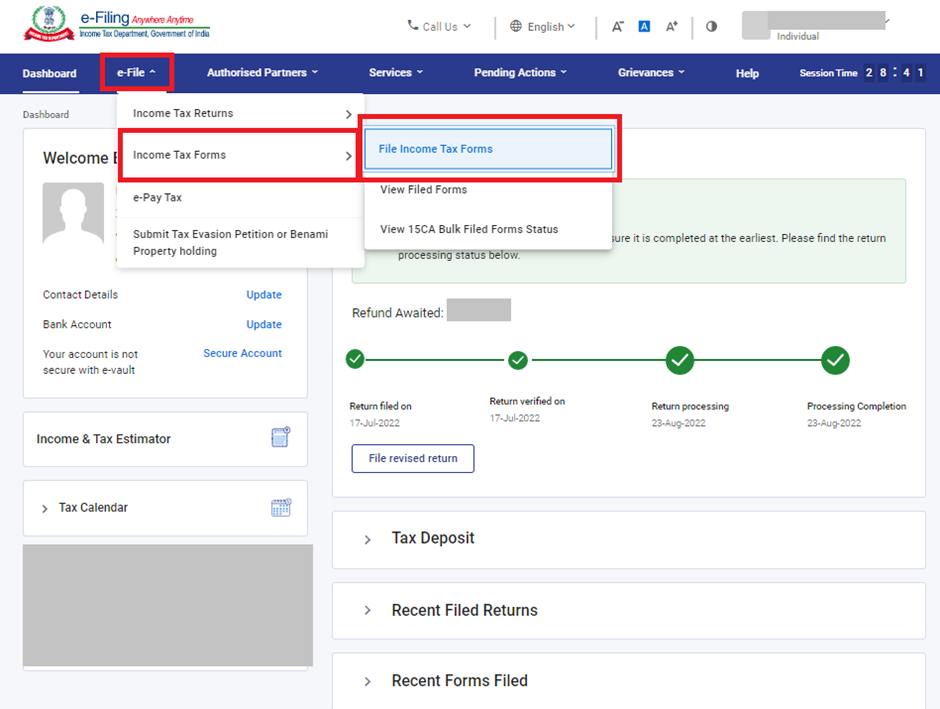

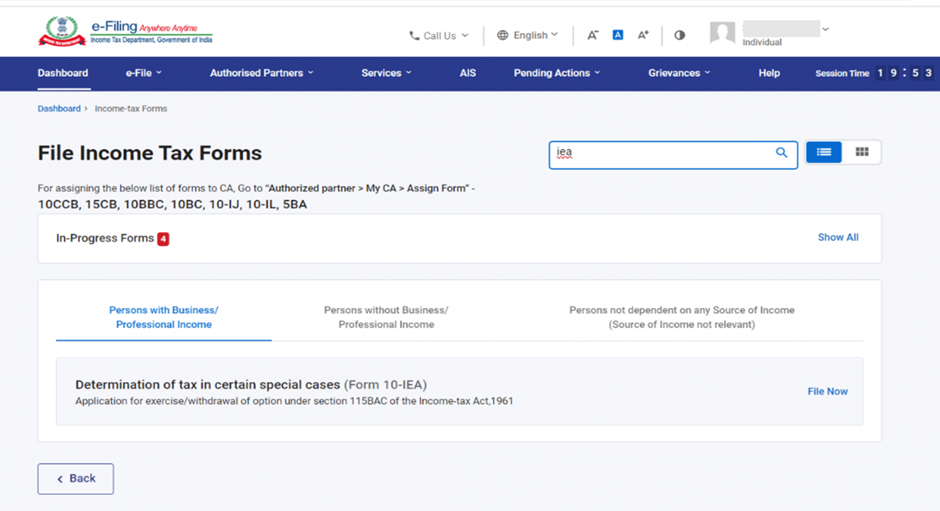

How to File Form 10-IEA

Follow these steps for filing Form 10-IEA online:

Step 1: Login on the e-filing portal

Step 2: On the dashboard, click ‘e-File’ > ‘Income tax forms’ > ‘File Income Tax Forms’

Step 3: Scroll down to select Form 10-IEA. Alternatively, enter Form 10-IEA in the search box. Click on ‘File now’ button to proceed.

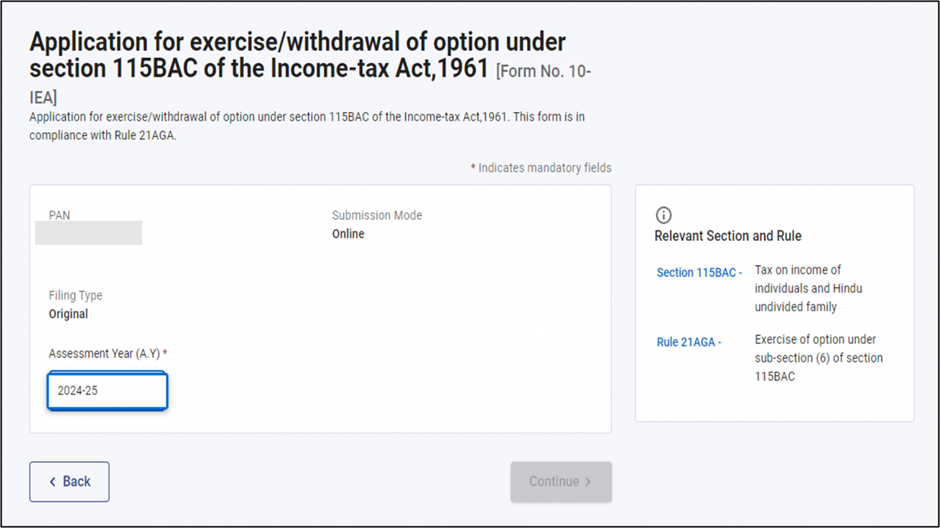

Step 4: Select the Assessment Year for which you are filing the return. For eg: If you are filing taxes for the income earned in FY 2023-24, then select AY 2024-25.

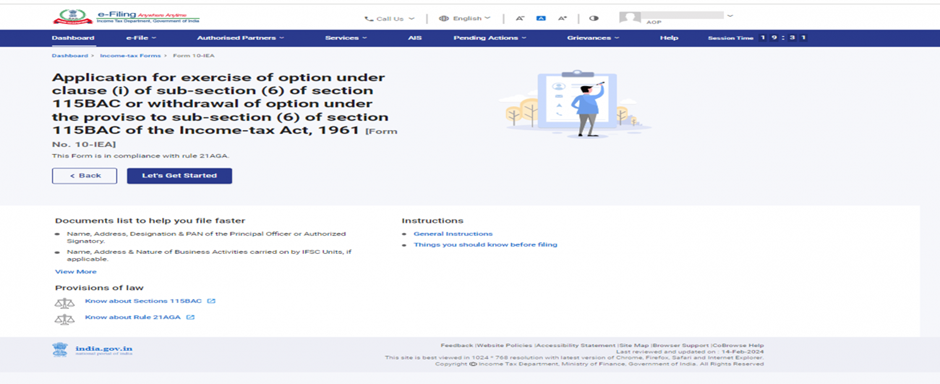

Step 5: After checking the documents required for filing the form click on ‘Let’s Get Started’.

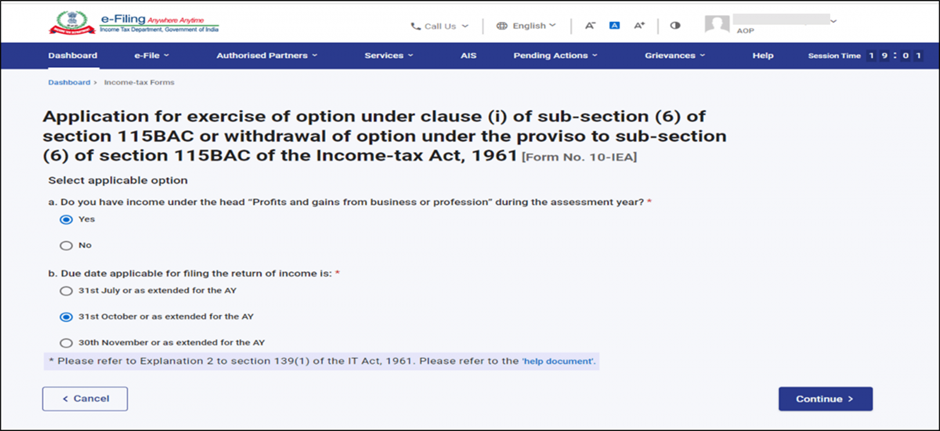

Step 6: Select “Yes” if you have Income under the head “Profits and gains from business or profession” during the assessment year. Select the due date applicable for filing of return of income and click on continue.

Note: Use “help document” by clicking on help document hyperlink for the help for selecting the applicable due date.

Step 7: Click ‘Yes’ to confirm the selection of the regime.

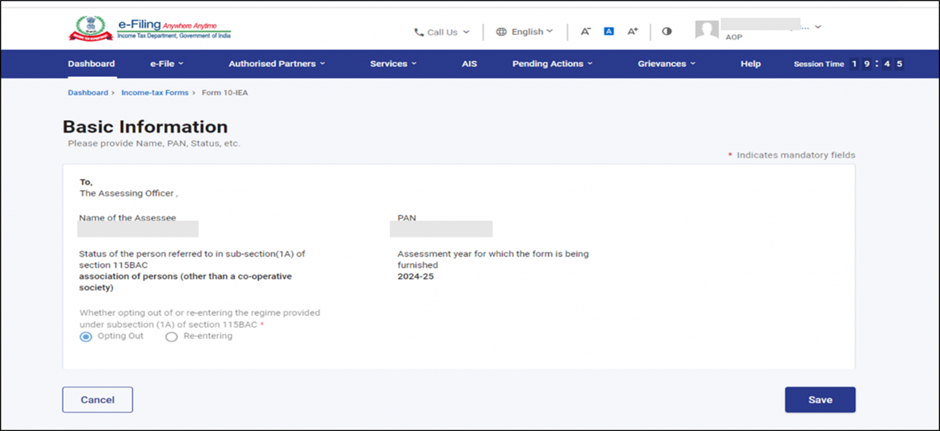

Step 8: Form 10-IEA has 3 sections. Verify and Confirm each section. They are as follows:

i. Basic Information: In Basic Informationsection, your basic information will be pre-filled. If you are filing form for the first time then opting out option will be auto-selected and if system has valid form with opting out option, then re-entering option will be auto-selected. Click on ‘Save’ button.

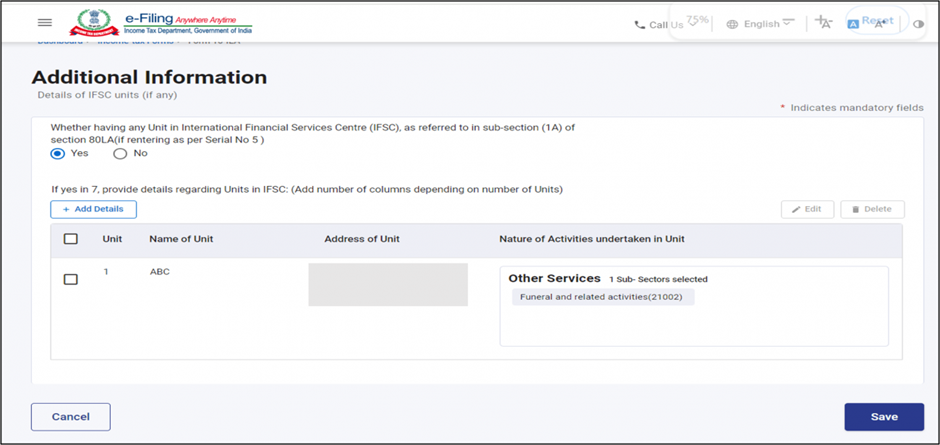

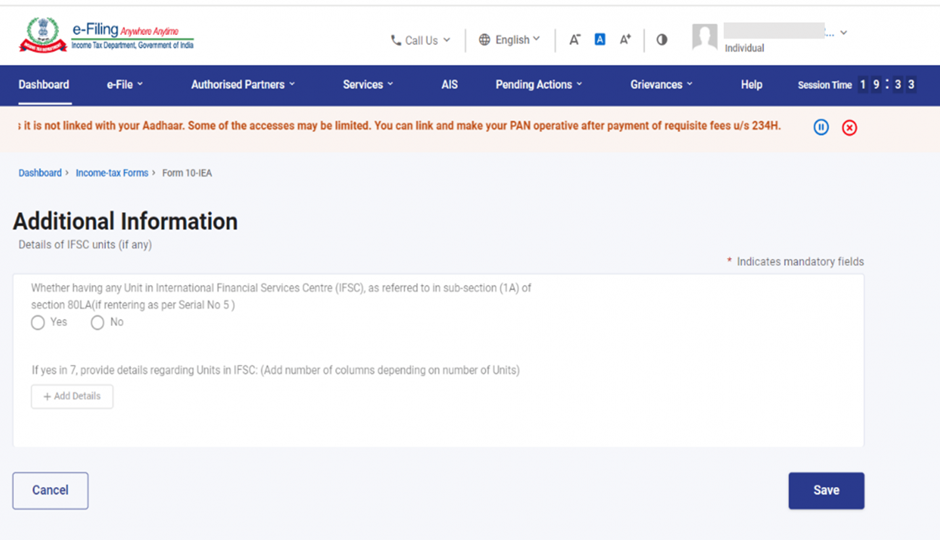

ii. Additional Information: Fill the necessary details in Additional information section related to IFSC unit (if any) and click on ‘Save’.

If you are opting out of new Tax regime this Additional Information panel will be greyed off

iii. Declaration and Verification: Verification section contains self-declaration where you will be required to check the boxes and agree to the terms and conditions. Verify whether all the details are correct and save the information. Once done, click on ‘Preview’ to review Form 10-IEA.

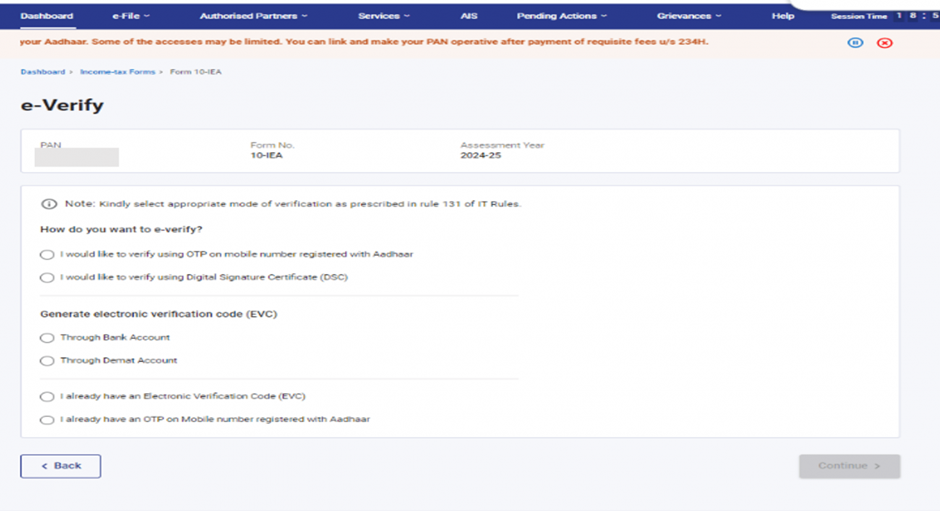

Step 9: After reviewing all the information, ‘Proceed’ to e-verify’. You can e-verify either through:

Aadhaar OTP

Digital Signature Certificate (DSC)

Electronic Verification Code (EVC)

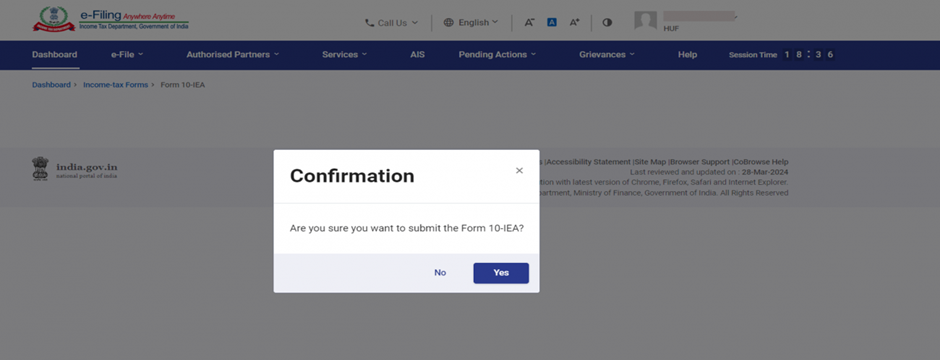

Step 10: After verification Click on ‘Yes’ to submit the Form.

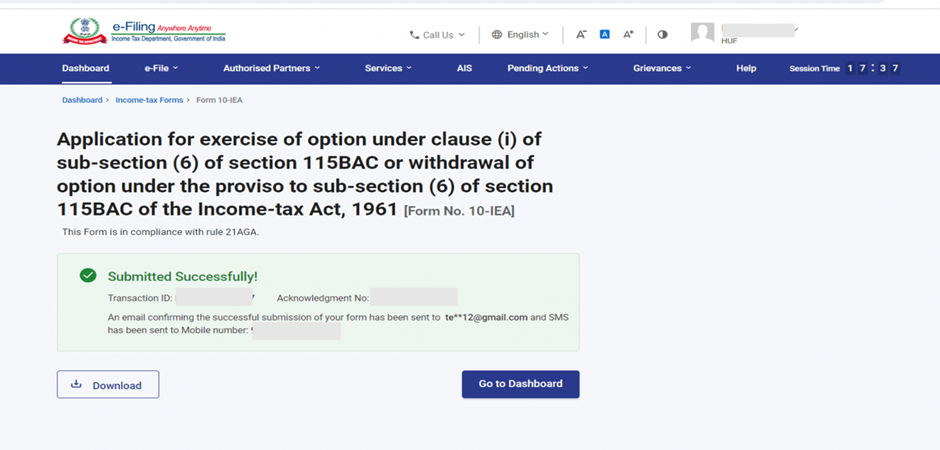

Step 11: After successful e-Verification, a success message is displayed along with a Transaction ID and an Acknowledgement Receipt Number. Please keep a note of the Transaction ID and Acknowledgement number for future reference. You can also download the form and locate the acknowledgment number. To download the filed form, go to ‘e-File’ → ‘Income Tax Forms’ → ‘View Filed Forms’.

The new section 43B(h) will be applicable from April 1, 2024 (AY 2024-25), Section 43B(h) of the Income Tax Act introduces significant changes concerning expenses related to purchases or services from Micro and Small Enterprises. Please note this section is not applicable on Medium Enterprises.

43B(h) has been inserted as a Socio-Economic Welfare Measure to ensure timely payments to micro and small enterprises.

We all know that section Section 43B of the Act provides for certain deductions to be allowed only on Actual Payment basis.

Finance Bill 2023 has newly inserted a clause to this section which is as under:

Section 43B (h) of Income Tax Act says:

“any sum payable by the assessee to a MICRO or SMALL enterprise beyond the time limit specified in 15 of the Micro, Small and Medium Enterprises Development Act, 2006,”

The above clause indicated that, in order to be eligible to claim deduction of the sum payable to micro and small enterprises, the payment shall be actually made within the time limit specified in 15 of the MSME Act, 2006.

Section 15 of MSME Development Act, 2006 says:

“Where any supplier supplies any goods or renders any services to any buyer, the buyer shall make payment therefor on or before the date agreed upon between him and the supplier in writing or, where there is no agreement in this behalf, before the appointed day*:

Provided that in no case the period agreed upon between the supplier and the buyer in writing shall not exceed forty-five days from the day of acceptance or the day of deemed acceptance”

It is very clear that, the buyer shall make the payment to the supplier as agreed between them, however the same cannot exceed beyond 45 days from date of acceptance or the day of deemed acceptance i.e., from the day of acceptance of the goods/service.

Section 2(b) of the MSME Development Act, 2006 says:

“Appointed Day” means the day following immediately after the expiry of the period of fifteen (15) days from the day of acceptance or the day of deemed acceptance of any goods or any services by a buyer from a supplier.

Explanation—For the purposes of this clause-

(i) “the day of acceptance” means-

(a) the day of the actual delivery of goods or the rendering of services; or

(b) where any objection is made in writing by the buyer regarding acceptance of goods or services within fifteen days from the day of the delivery of goods or the rendering of services, the day on which such objection is removed by the supplier;

(ii) “the day of deemed acceptance” means, where no objection is made in writing by the buyer regarding acceptance of goods or services within fifteen days from the day of the delivery of goods or the rendering of services, the day of the actual delivery of goods or the rendering of services;

Section 16 of MSME Development Act, 2006 says:

“Where any buyer fails to make payment of the amount to the supplier, as required under section 15, the buyer shall, notwithstanding anything contained in any agreement between the buyer and the supplier or in any law for the time being in force, be liable to pay compound interest with monthly rests to the supplier on that amount from the appointed day or, as the case may be, from the date immediately following the date agreed upon, at three times of the bank rate notified by the Reserve Bank”

Consequences upon Failure to make payment to Micro and Small Enterprises under Section 43B(h)

If the payment is made after 45 days or 15 days as specified – then expenses disallowed in the year and deduction will be available in the year in which the payment is made.

If the payment is due for more than 45 days or 15 days as specified but the payment is made before the end of the Financial Year – then in such case, the deduction of the expense will be available in the same year itself.

The classification of the enterprise as Micro, Small & Medium as defined in Micro, Small and Medium Enterprises Development Act, 2006 is hereby produced for your reference:

Section 92 of the Income Tax Act, 1961, deals with regulations of transfer pricing in India. It is a practice of determining the price of the transactions between associate enterprises and computation of Income from International transaction at Arm’s Length Price. This section has significant implications for Multi National Enterprises (MNE) operating in India and also on Specified Domestic Transaction (SDT).

Section 92E (Audit under Transfer Pricing):

Every person who has entered into an international transaction (IT) or specified domestic transaction (SDT) during a previous year shall obtain a report from an accountant (Chartered Accountant) and furnish such report on or before the “specified date” in the prescribed form (3CBE) duly signed and verified in the prescribed manner by such accountant and setting forth such particulars as may be prescribed.

Prescribed form for report from accountant is Form No. 3CEB. Under proviso to rule 12(2) audit report shall be furnished electronically.

“Specified date” means the date one month prior to the due date for furnishing the return of income under sub-section (1) of section 139 for the relevant assessment year.[Section 92F(iv)] As due date for ITR in transfer pricing cases is 30th November of the relevant assessment year, specified date is 31St October. Report from accountant (CA) will have to be furnished on or before 31st October of relevant assessment year in Form 3CEB.

PENALTY ON ASSESSEE FOR FAILURE TO FURNISH REPORT UNDER SECTION 192E [SECTION 271BA]

If any person fails to furnish a report from an accountant as required by section 92E, the Assessing Officer may direct that such person shall pay, by way of penalty, a sum of one hundred thousand rupees ie.Rs.1,00,000.

PENALTY ON AUDITOR FOR FURNISHING INCORRECT INFORMATION IN REPORTS OR CERTIFICATES

Section 271J of the Act provides for Penalty for furnishing incorrect information in reports or certificates. Section 271J provides that where the Assessing Officer or the Commissioner (Appeals), in the course of any proceedings under the Income Tax Act, 1961, finds that an accountant has furnished incorrect information in any report or certificate furnished under any provision of Income Tax Act or the rules made thereunder, the Assessing Officer or the Commissioner (Appeals) [or Joint Commissioner (Appeals) may direct that such accountant (CA), shall pay, by way of penalty, a sum of Rs. 10,000 for each such report or certificate.

HOW TO FILE FORM 3CEB:

Form 3CEB can be filed online by following these easy steps

Step 1: You need to avail the services of a Chartered Accountant (CA) who will audit the business transactions. For this log in to your e-Filling portal account, navigate to the ‘My Chartered Accountants’ page and add a CA authorised by you.

Step 2: Once you select a CA from the list, you must assign Form 3CEB to him/her. You can assign the form by selecting the CA’s name, selecting the filing type and entering the assessment year.

Step 3: Once the form has been successfully assigned, the CA can find it in his/her work list in the ‘For Your Action’ section. He/she can either accept or reject the assignment. If the assigned CA rejects it, you must reassign the form.

Step 4: If the CA accepts the task, he will fill in all the necessary details in the form after proper assessment and auditing.

Step 5: Once done, you can find the form uploaded by the CA in the Taxpayer’s work list. You can click the ‘For Your Action’ button and find the form marked ‘Pending for Acceptance’. You can either accept or reject it after reviewing the form. Once you approve it, Form 3CEB will be filed.

Form 3CEB comprises three parts – Part A, Part B and Part C.

Part A contains basic details that need to be filled up.

Part B have a lot of information related to international transactions must be provided. It includes information about associate enterprises, nature and particulars of transactions.

Part C of the form is solely dedicated to specified domestic transactions. While Part B focuses on international transactions, Part C is on engagements with domestic enterprises.

Conclusion:

As per Section 92E of the Income Tax Act, which relates to international transactions and specified domestic transactions, filing Form 3CEB is mandatory for companies who are engaged in foreign or domestic business with associated enterprises. Taxpayers must strictly follow the requirements listed in Form 3CEB; otherwise, there are penalty rules which might be enforced.

Clause 44 It was added w.e.f 20th August 2018 but Reporting under this clause was deferred till 31st March 2019 vide Circular No. 6/2018 dated 17th August 2018, So reporting in clause 44 is started from AY 2019-20.

TheObjective for insertion of this Clause 44:

The main objective is to co-relate GST Data with Income Tax Data.

FAQ’s on CLAUSE 44

Q.1. Is reporting in this clause applicable only for Assessee who are GST registered?

Ans: No, Reporting is to be made by all assesses who are registered under GST or not.

Q.2. Interpretation of wordings “Breakup of total expenditure”? What expenditures are not Included?

Ans: Interpretation should be “broader” with reference to Capital Expenditure as well as Revenue Expenditure including Purchases.

But activities or transactions which those neither as a supply of goods nor a supply of services and thus expenditure incurred in respect of such activities need not be reported under this clause.

1. Salary not Included

2. Depreciation under section 32, deduction for bad debts u/s 36(1)(vii) etc. which are not expenses should not be reported under this clause.

3. Bad Debts written off etc.,

So we can say any expenditure that is incurred, wholly and exclusively for the business or profession of the assessee qualifies for the deduction under the Act.

Q.3. Tabular format for disclosure:

Sl. No.

Total amount of Expenditure incurred during the year

Relating to Goods or services Exempt from GST

Relating to entities Falling under Composition Scheme

Relating to Other Registered Entities

Total Payment to Registered Entities

Expenditure relating to entities not registered under GST

(1)

(2)

(3)

(4)

(5)

(6)

(7)

The format as per clause 44 of form 3CD requires that the information is to be given as per the following details:

A. Total amount of expenditure incurred during the year

B. Expenditure in respect of entities registered under GST

C. Expenditure related to entities not registered under GST

the expenditure in respect of entities registered under GST is further sub-classified into four categories as follows:

a) Expenditure relating to goods or services exempt from GST

b) Expenditure relating to entities falling under the composition scheme

c) Expenditure relating to other registered entities

d) Total payment to registered entities

Q.4. Colum 2 says “Total amount of Expenditure incurred during the year” so shall we report head-wise / nature wise expenditure?

Ans: The heading of the table which starts with the words “Breakup of total expenditure” and hence the total expenditure including purchases as per the above format may be given. It appears that head-wise / nature wise expenditure details are not envisaged in this clause.

However, it is recommended to take head wise/nature wise expenditure details as a part of working paper of the Audit.

Q.5. What are the Expenditure relating to other registered entities (column 5)?

Ans: The value of all inward supplies from registered dealers, other than supplies from composition dealers and exempt supply from registered dealers, are to be mentioned in this column.

Q.6. What is the meaning of “Total payment to registered entities (column 6)”?

Ans: The language used in sub-heading of column 6 is total’ payment’ to registered entities. The word ‘payment’ should harmoniously be interpreted as ‘expenditure’ as the combined heading of columns (3), (4), (5) is ‘Expenditure in respect of entities registered under GST’. Hence, the total expenditure in respect of registered entities i.e., sum total of values reported in columns (3), (4) and (5) should be reported in Column 6.

Q.7. Checks and Control while reporting?

Ans: There are some checks and control so auditor make sure on correctness on reporting.

Amount of Serial number 2 is equal to amount of serial number 6 PLUS Serial number 7.

Amount of Serial number 6 is equal to amount of serial number 3 PLUS Serial number 4 PLUS Serial number 5.

Total Value of Expenditure in P & L for the year

XXX

Add: Total Value Capital Expenditure Not Included in P & L

XXX

Less: Total Value Of non-cash Charges considered as expenditure

XXX

Less: Total Value of Expenditure Excluded For being Transactions in securities and Transactions In money

XXX

Less: Total value Of Expenditure Excluded by virtue of Schedule III to the CGST Act,2017

SEBI has been notified as the regulator of gold exchanges in the country. SEBI has come up with the ‘Framework for operationalizing the Gold Exchange in India’ vide Circular dated January 10, 2022 and has also declared the instrument for trading in Gold Exchange ,i.e., EGRs as ‘securities’ under Section 2(h)(iia) of the Securities Contracts (Regulation) Act 1956 dated December 24, 2021 vide Gazette notification. The SEBI Regulations, 2021’ provides that any person willing to carry on the business of providing vaulting services in relation to gold, i.e., storage and safekeeping of physical gold deposited by the depositor for the purpose of trading in EGRs may apply to SEBI and obtain registration to act as a Vault Manager. The Framework provides that stock exchanges willing to trade in EGRs may apply to SEBI and begin trading in EGRs in new segment. A structure of the transactions in respect of creation, trading and conversion of EGR into Physical Gold has also been defined.

PROPOSED AMENDMENTS

In line with these new developments, it is proposed to bring following amendments in the ITA to make the conversion of physical gold into EGR and vice versa tax neutral:

New provision, S. 47(viid), is proposed where under the conversion of physical gold (held as capital asset) into EGRs issued by a Vault Manager and vice versa, shall not be considered as ‘transfer’ within the meaning of S. 47 of the ITA. Hence, there would be no capital gain arising at the time of mere conversion.

Further, S. 2(42A) is proposed to be amended to include the period of holding of the converting asset in the period of holding of the converted asset. In other words, the period of holding of EGRs would include even the period for which the physical gold was held by the assessee prior to conversion into EGRs and vice versa. (Clause (hi) to Explanation 1 of S. 2(42A)).

Lastly, it is proposed that the Cost of Acquisition of EGRs shall be deemed to be the cost of gold in the hands of the person in whose name EGRs is issued. Similarly, where gold is released against an EGRs, the COA of the gold shall be deemed to be the cost of the EGRs in the hands of such person. (S. 49(10)).

These amendments will become effective from April 1, 2024 and shall accordingly, apply in relation to the AY 2024-25 and subsequent AYs.

CLARIFICATION REQUIRED

There is an ambiguity in relation to the indexation benefit. A clarification is also needed with regard to the classification of Electronic Gold Receipts (ECRs) as Short term or Long term, whether EGRs must be considered as a Capital Asset (36months/ 3 years) or as a Security (12 months/1 year).

Section 2(13A) of Income Tax Act defines Business Trust as below: “Business trust” means a trust registered as, —

(i) an Infrastructure Investment Trust under the Securities and Exchange Board of India (Infrastructure Investment Trusts) Regulations, 2014 made under the Securities and Exchange Board of India Act, 1992 (15 of 1992); or

(ii) a Real Estate Investment Trust under the Securities and Exchange Board of India (Real Estate Investment Trusts) Regulations, 2014 made under the Securities and Exchange Board of India Act, 1992 (15 of 1992)

Business Trust act like a mutual fund that invest into real estate projects or infrastructure projects by raising resources from different investors. These trusts can raise capital by way of issue of units which are listed on a recognized stock exchange. Business trusts can also raise debt from people – both residents and non-residents. It is not necessary that the business trust must be listed, however it is mandatory for it to be registered with SEBI with effect from 1st April, 2020.

REAL ESTATE INVESTMENT TRUST (REITs)

REITs are companies which owns, manages and finance few income-generating real estate and offers its units to public investors. REITs own many types of commercial real estate, ranging from office and apartment buildings to warehouses, hospitals, shopping centers, hotels and even timberlands.

Globally, REITs invest primarily in completed, revenue generating real estate assets and distribute major part of the earning among their investors. Typically, most of such investments are in completed properties which provide regular income to the investors from the rentals received from such properties.

REITs are principally expected to invest in completed assets. Income would consist of rental income, interest income or capital gains arising from sale of real assets / shares of SPV. They are managed by professional managers which usually have diverse skill bases in property development, redevelopment, acquisitions, leasing and management etc. Listed REITs provide liquidity and therefore provide easy exit to the investors.

INFRASTRUCTURE INVESTMENT TRUSTS (InvITs)

Infrastructure Investment Trusts make direct investment in infrastructure facilities which are yielding income e.g., Toll Road, Railways, Inland waterways, Airport, Urban public transport. InvITs will allow infrastructure developers to monetize specific assets, helping them use proceeds for completing projects of theirs stalled for want of funds.

Structure of InvITs is quite similar to REITs. The main difference is InvITs make investment into infrastructure facilities whereas REITs make investment in commercial real estate properties.

TAXABILITY UNDER SECTION 115 UA:

IN THE HANDS OF THE UNIT HOLDERS:

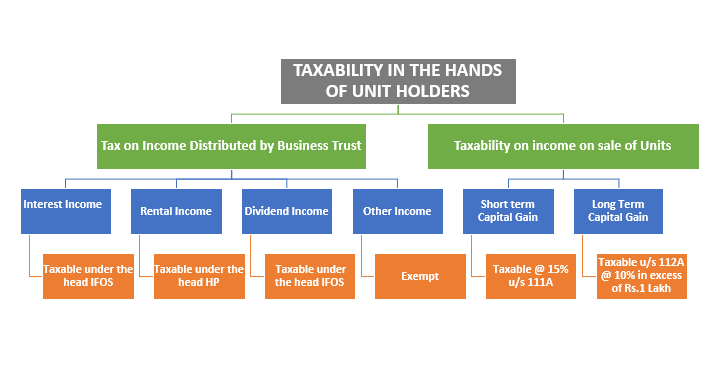

The income of unit holders of Business Trust can be categorized into two parts.

Tax on Income Distributed by Business Trust:

There is a special taxation regime for taxability of income distributed by such business trusts in the hands of the unit holders. The income distributed by a business trust to its unit holders shall be deemed to be of the same nature and in the same proportion in the hands of the unit holders, as it had been received by, or accrued to the business trust. The person distributing the income on behalf of the business trust is required to furnish the statement of income distributed to the unitholder in Form No. 64B by the 30th June. Example Mr. Saurabh, a resident individual, has received the following ‘Form 64B – Statement of income distributed by a business trust to the unit holders’ for the Financial Year 2017-18.

S. No.

Amount Distributed

Date of Distribution

Amount of income in the nature of interest referred to in Section 10 (23FC)

Amount of Income in the nature of renting or leasing referred to in Section 10(23FCA)

Amount of Income in the nature of Dividend

Amount of Other Income

1

50,000

25/10/2020

30,000

20,000

2

75,000

16/11/2020

25,000

27,000

23,000

Let’s see how taxability of each of such income will be determined in the hands of Mr. Saurabh

Income in the nature of Interest: The income in the nature of interest referred to in sub clause (a) of Section 10(23FC) is chargeable to tax in the hands of the unit holders. If the unit holder is non-resident the rate of tax on such income is 5% and for resident unit holders, it is chargeable to tax at slab rates. This income is exempt in the hands of the business trust. This interest received or receivable from a special purpose vehicle by the business trust is accorded a pass-through treatment and is taxable directly in the hands of the unit holders. The business trust is liable to deduct TDS on this interest income at the rate of 10% in the case of a resident unit holder and 5% in the case of Non-resident unit holders. Example Mr. Saurabh has to include the income of Rs.30,000 distributed by the business trust on 25/10/2017 as an interest income in his Income Tax Return.

Rental Income: The rental income referred to in Section 10(23FCA) is taxable income in the hands of the unit holders. Any income of a business trust, being a real estate investment trust, by way of renting or leasing or letting out any real estate asset owned directly by such business trust is exempt in the hands of the business trust. This income is chargeable to tax in the hands of the unit holders as rental income. The REIT is liable to deduct TDS on such distributed income at the rate of 10% for resident unit holders and at the rates in force for non-resident unit holders. Example Mr. Saurabh has to show the income of Rs.25,000 distributed on 16/11/2017 by the business trust as rental income in his Income Tax Return.

Dividend Income: Earlier, the dividend component of the income distributed by the business trust is exempt in the hands of the unit holder. The business trust was also provided an exemption in respect of such income. However, with effect from April 1, 2020, there has been an overhaul of India’s dividend tax regime. Until now Indian companies were required to pay DDT and shareholders (except non-corporate residents) were exempt. Going forward, the tax incidence will shift from the company to the shareholders.

Any Other Income: Any distributed income, referred to in section 115UA, received by a unit holder from the business trust is exempt in the hands of the unit holder as per Section 10(23FD). Example The income of Rs.20,000 received on 25/10/2017 and Rs.23,000 received on 16/11/2017 is exempt in the hands of Mr. Saurabh.

Tax on Income on Sale of Units

The profit from the sale of the units of the business trust is chargeable to tax under the head capital gains. The tax treatment will differ for the Short-term capital gains and long-term Capital gains. The period of holding of units of the business trust to qualify as a long-term capital asset is more than 36 months.

Short-Term Capital Gain: The short-term capital gains on which STT is paid is chargeable to tax at the rate of 15% as per section 111A. The deductions under Chapter VI-A are not allowed from such capital gains.

Long-Term Capital Gain: The long-term capital gains on which STT is paid were exempt in the hands of the Unit holders under Section 10(38) till the A.Y 2018-19. Exemption for long-term capital gains arising from the transfer of units of business trust has been withdrawn by the Finance Act, 2018 with effect from Assessment Year 2019-20 and a new section 112A is introduced in the Income-tax Act. As per Section 112A, long-term capital gains arising from the transfer of a unit of a business trust shall be taxed at 10% (without giving the benefit of indexation). The tax on capital gains shall be levied in excess of Rs.1 lakh. The deductions under Chapter VI-A are not allowed from such capital gains.

2. IN THE HANDS OF THE BUSINESS TRUST:

REITs have been conferred as hybrid pass-through status for income tax purposes, meaning that the onward distribution of income by a REIT to its unit holders retains the same character as the underlying income stream received by the REIT. Interest income and rental income from property held directly by the trust, is not taxable in the hands of the REIT. However, any capital gains on the sale of assets/ shares of an SPV are taxable in the hands of the trust, depending on the period of holding whereas dividend income is not liable to tax. Further, any other income earned by a REIT shall be subject to tax at the maximum marginal rate. Business trust is compulsorily required to file return as per section 139(4E)

STATEMENT UNDER SUB-SECTION (4) OF SECTION 115UA:

(1) The statement of income distributed by a business trust to its unit holder shall be furnished to the Principal Commissioner or the Commissioner of Income-tax within whose jurisdiction the principal office of the business trust is situated, by the 30th November of the financial year following the previous year during which such income is distributed;

Provided that the statement of income distributed shall also be furnished to the unit holder by the 30th June of the financial year following the previous year during which the income is distributed.

(2) The statement of income distributed shall be furnished under sub-section (4) of section 115UA by the business trust to –

the Principal Commissioner or the Commissioner of Income tax referred to in sub-rule (1), in Form No. 64A, duly verified by an accountant in the manner indicated therein and shall be furnished electronically under digital signature;

the unit holder in Form No. 64B, duly verified by the person distributing the income on behalf of the business trust in the manner indicated therein.

FORM 64A

This form will comprise of the statement of income paid or credited by a venture capital company under section 115U of the Income Tax Act 1961. Any individual who is responsible of making payment of the income distributed on behalf of a business trust to a unit holder is required to furnish a statement to the authority within the prescribed time. This form can be submitted at the post offices and banks designated for this purpose. Form 64A can be found online on the official Income Tax filing website and can be downloaded from Forms download section or Directly download Form 64A. The form contains several details which need to be filled out before submission. It is important to fill out the correct details before submitting the form. Copy of certificate of registration under SEBI, copy of trust deed registered under the provisions of the registration act, 1908, Audited accounts including balance sheet, annual report and certifies copies of income shall be enclosed with the form 64A at the time of submission.

FORM 64B

The person distributing the income on behalf of the business trust is required to furnish the statement of income distributed to the unitholder in Form No. 64B by the 30th June.

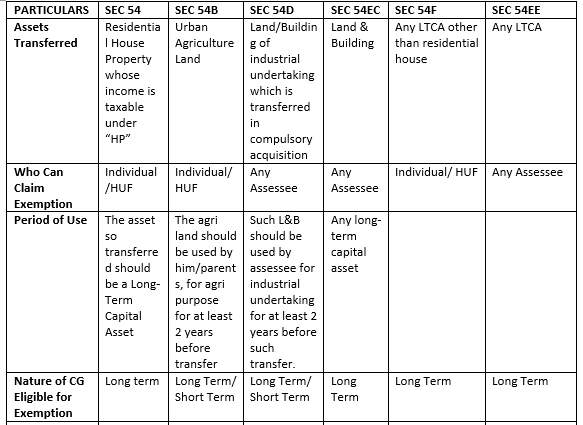

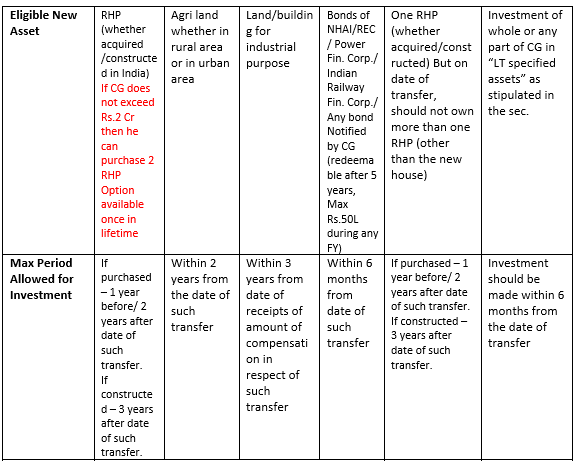

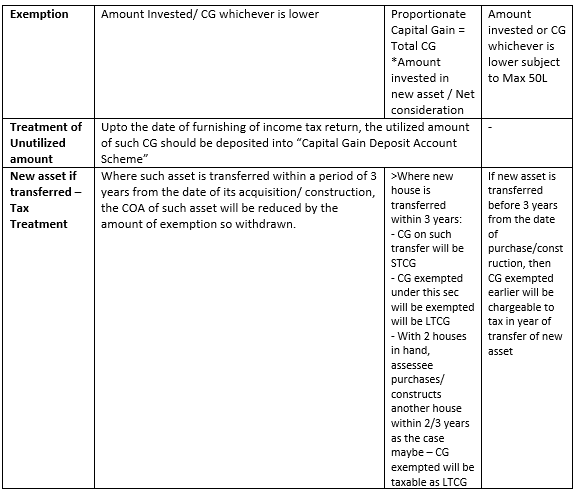

Section 54 gives exemption to a taxpayer who sells his residential house and acquires another residential house property from the sale proceeds. Only an Individual/HUF can avail this benefit under this section.

Section 54 provides the exemption which will be the lower of the following:

Amount of capital gains arising on transfer of residential house;

Amount invested in purchase/construction of new residential house property including the amount deposited under Capital Gains Deposit Account Scheme.

Exemption is available in respect of only one residential house property purchased/constructed in India. If more than one house is purchased or constructed, then exemption can only be claimed for one house property under this section. No exemption is available in respect of house purchased outside India.

In order to control any misutilization of the exemption claimed under section 54, this section restricts the taxpayer to sell the new house property till 3 years. If the taxpayer sells the new house before 3 years the benefit received under this section will be withdrawn and the amount of capital gain which was earlier claimed as exempt, will be deducted from the cost of acquisition of the new house at the time of computation.

SECTION 54EC OF INCOME TAX ACT, 1961

Section 54EC provides exemption to any assessee for the capital gain arising on sale of land or building, if when the amount received on sale is invested in Specified Bonds. Specified Bonds refer to those bonds issued by the Rural Electrification Corporation, National Highway Authority of India, Power Finance Corporation Limited, Indian Railway Finance Corporation or bonds issued by the Central Government if specified, which are redeemable after 5 years and are issued on or after 01.04.2018.

The Capital gain arising should be invested in a long term specified Asset within 6 months from the date of transfer.

The exemption shall be the lower of:

Actual Capital Gain; or

Amount invested in Specified Bonds (less than Rs.50 Lakhs)

However, the maximum investment that can be made under this section is Rs.50 Lakhs In case bonds are transferred or converted or availed loan or advance against these bonds before the expiry of 5 years, the Capital Gain exempted earlier shall be taxed as LTCG in the year of violation of the condition.

SECTION 54B OF INCOME TAX ACT, 1961

Section 54B provides the benefit of exemption to those Individuals/HUFs who wishes to sell their agricultural land and acquire another agricultural land from the sale proceeds. The old agricultural land acquired shall be used by him or his parents for at least 2 years before the transfer and the maximum period for the new investment to be made in agricultural land is 2 years from the date of such transfer.

Exemption under section 54B shall be lower of:

Amount of capital gain arising on transfer of agricultural land; or

Investment in new agricultural land including the amount deposited under Capital Gain Account Scheme.

The exemption shall be withdrawn if the new agricultural land is sold before the period of 3 years from the date of acquisition, and therefore the amount, earlier exempt, will be reduced from the cost of acquisition of agricultural land.

SECTION 54D OF INCOME TAX ACT, 1961

Section 54D gives the benefit to claim exemption to any assessee where capital gain arises on compulsory acquisition of land or building forming a part of industrial undertaking and reinvesting the amount for acquiring new land or building for the purpose of shifting or re-establishing the industrial undertaking.

Exemption under this section is available for both short term and long-term capital gain.

It is mandatory that the transferred asset should have been used for the industrial purpose for a period of at least two years before the date of acquisition. The transferor is required to invest the amount in purchasing any other land or building for the purpose of shifting or re-establishing the industrial units. The said amount needs to be invested within a period of three years from the date of receipt of the compensation

The exemption under section 54D would be lower of:

Capital Gain on compulsory acquisition of land or building; or

Amount of investment for acquisition of new land or building

The exemption would be retracted if the new land or building acquired is transferred before 3 years from the date of acquisition and hence, capital gain exempted under this section would be reduced from the cost of acquisition at the time of computation of capital gain.

SECTION 54F OF INCOME TAX ACT, 1961

Section 54F provides the exemption to an Individual/HUF on sale of any long-term capital asset (other than residential house property) and the proceeds shall be reinvested for purchasing or constructing a residential house property. Maximum period for investing in new residential property by purchase is one year before or two years after the date of transfer and by construction is 3 years from the date of transfer.

Exemption under this section shall be available as:

Full amount of capital gain is exempt in case full consideration is invested.

Although in case proportionate consideration is invested, exemption will be as

Exemption = Long term capital gain * Amount re-invested / Net consideration

Here, Net consideration refers to the value of consideration excluding any expenditure incurred exclusively for the purpose of transfer.

Exemption would be withdrawn if the taxpayer sells the residential property, whether purchased or constructed, before 3 years from the date of transfer. Exemption under Section 54F will not be available in certain cases:

If the taxpayer already owns more than one residential house property at the date of transfer of the asset

If the taxpayer purchases additional residential house (other than the new house purchased/constructed for exemption under Section 54F) within a time frame of one year from the date of transfer.

If the taxpayer constructs additional residential house (other than the new house constructed/purchased for exemption under Section 54F) within a time frame of three years from the date of such transfer.

SECTION 54EE OF INCOME TAX ACT, 1961

Exemption under section 54EE is available only when the assessee has earned capital gain on the sale of long-term capital gain and reinvested the sale proceeds either partly or in whole in “long term specified assets”. Long Term Specified Assets refers to the unit of funds issued on or after 1st April, 2019 as notified by the Government.

The investment must be made withing 6 months from the date of transfer of such specified asset. And, the total investment in such assets cannot exceed the limit of Rs.50 lakhs during the financial year and even in the subsequent financial year.

Exemption under section 54EE shall be lower of:

Amount of capital gain arising on the transfer; or

Rs.50 lakhs.

The amount so invested in the new specified asset cannot be transferred or converted within a period of 3 years. However, if the taxpayer transfer or converts the asset before the lock in period of 3 years, the exemption would be withdrawn and he/she would have to pay long-term capital gain on such transfer.

CAPITAL GAIN DEPOSIT ACCOUNT SCHEME:

To claim exemption under section 54 or under any other subsections as mentioned above, the taxpayer shall accept the conditions according to each section. If the capital gain arising on transfer of the asset is not utilized till the date of filing the return of income, then the benefit of exemption can be availed by depositing the unutilized amount in Capital Gains Deposit Account Scheme in any branch of public sector bank, in accordance with Capital Gains Deposit Accounts Scheme, 1988 (hereafter referred as Capital Gains Account Scheme). The new asset can be acquired by withdrawing the amount from the said account within the specified time-limit as the case may be.

NON UTILIZATION OF AMOUNT DEPOSITED IN CAPITAL GAIN DEPOSIT ACCOUNT SCHEME:

In case the amount deposited under the Capital Gains Account Scheme is not utilized within the specified period for acquisition of the asset, then the unutilized amount (for which exemption is claimed) will be taxed as long- term capital gain of the year in which the specified period gets over.