Advance tax means income tax should be paid in advance instead of lump sum payment at year end. It is also known as pay as you earn tax. These payments have to be made in instalments as per due dates provided by the income tax department.

Total estimation is used for the calculation of advance tax.

WHO SHOULD PAY ADVANCE TAX?

If the total tax liability exceeds Rs 10,000 in a financial year in case of salaried, freelancers and businesses, then advance tax shall be payable.

Senior citizens whose income does not come out of any business or profession, are exempt from paying advance tax.

In case of Presumptive income under Section 44AD for Businesses & for Professionals, the taxpayers have to pay the whole amount of their advance tax in one instalment on or before 15th March of any financial year. Although, they can pay all of their tax dues till 31st March.

ADVANCE TAX DUE DATES

Advance Tax has to be paid in different installments. The due dates for payment of advance tax are as follows:

STATUS

By 15th June

By 15th September

By 15th December

By 15th March

All assessee (other than eligible assessee as referred to in section 44AD/44ADA)

Minimum 15% of Advance Tax

Minimum 45% of Advance Tax

Minimum 75% of Advance Tax

100% of Advance Tax

Taxpayers who opted for presumptive taxation scheme of section 44AD/44ADA

Nil

Nil

Nil

100 % of Advance Tax

INTEREST UNDER SECTION 234B

Interest under section 234B is applicable in two of the following cases:

When the tax liability after reducing TDS for the financial year is more than Rs.10,000 and advance tax hasn’t been paid, or

The advance tax is paid, but the amount paid is less than 90% of the ‘assessed tax’.

Interest is calculated @ 1% on (Assessed Tax less Advance Tax).

Part of a month is rounded off to a full month.

The amount on which interest is calculated is also rounded off in such a way that any fraction of a hundred is ignored.

Example

Assume that Saurabh needs to pay a total tax of Rs.1,00,000. And, TDS of Rs 85,650 has already been deducted from his income. Saurabh paid Rs.5,000 on 25th March and he paid the balance amount at the time of filing his return on 17th July. Let’s check whether Saurabh needs to pay interest under section 234B.

Interest will be calculated as : Rs 9350 x 1% x 4 months (April, May, June, July) = Rs 374

Rs 374 is the interest payable under section 234B by Saurabh.

INTEREST UNDER SECTION 234C

Income Tax Department strives to make it as easy and convenient for citizens to comply with advance tax payments. So, one has the option of paying it in 4 instalments quarter-wise over the financial year.

However, if there is still any default, there are consequences in the form of interest penalty. Section 234C deals with the interest to be levied on the defaulters of payment of Advance Tax installment.

The interest for late payment is set at 1% on the amount of tax due. It is calculated from the individual cut-off dates shown above, till the date of actual payment of outstanding taxes.

The interest under this section is charged according to the scheduled installments. The taxpayer has to pay interest if he/she has paid the advance tax

Less than 12% of assessed tax before 15th June

Less than 36% of assessed tax before 15th September

Less than 75% of assessed tax before 15th December

Less than 100% of assessed tax before 15th March/31st March

Example

Mr. X has the total tax liability of Rs.1,00,000. This tax is to be paid in 4 installments. The calculation of interest to be charged for delay will be calculated as follows:

Due Dates

Advance Tax to be paid

Advance Tax actually paid

Shortfall

Months for which interest is charged

Penal Interest

15th June

15,000 (15%)

5,000

10,000

3

10000*1%*3= 300

15th Sept

45,000 (45%)

25,000

20,000

3

20,000*1%*3 = 600

15th Dec

75,000 (75%)

35,000

40,000

3

40,000*1%*3 = 1200

15th March

1,00,000 (100%)

50,000

50,000

1

50,000*1%*1= 5000

CRITERIA UNDER WHICH ADVANCE TAX INTEREST IS NOT PAYABLE

In case, there is any shortfall in the payment of advance tax due if it is on account of underestimation or failure to estimate the amount of capital gains or speculative income (lottery income, gambling income, etc), then the interest would not be payable.

Also, interest would not be payable if the taxpayers pay his dues before the end of the financial year.

FAQs

Q1. Does an NRI have to pay advance tax?

An NRI, who has an income accruing in India and the tax liability is in excess of Rs 10,000, is liable for payment of advance tax.

Q2. A senior citizen only has interest and pension income. Should he/she pay advance tax?

Resident senior citizens who do not have income arising out of business or profession, are not liable for advance tax.

Q3. Can an assessee claim deduction under 80C while estimating income for determining my advance tax?

Yes. An assessee can consider all the deductions under 80C (whichever applicable within the limit) while estimating the income for the financial year for computing your advance tax liability.

Q4. How can we make payment for advance tax?

Advance tax payment can be made using Challan 280 just like any other regular tax payment.

Q5. What happens if an assessee misses the deadline for payment of the last installment of advance tax, i.e., on 15th March?

Payment of advance tax can be made on or before 31st March of the year. Such payment will still be treated as advance tax only.

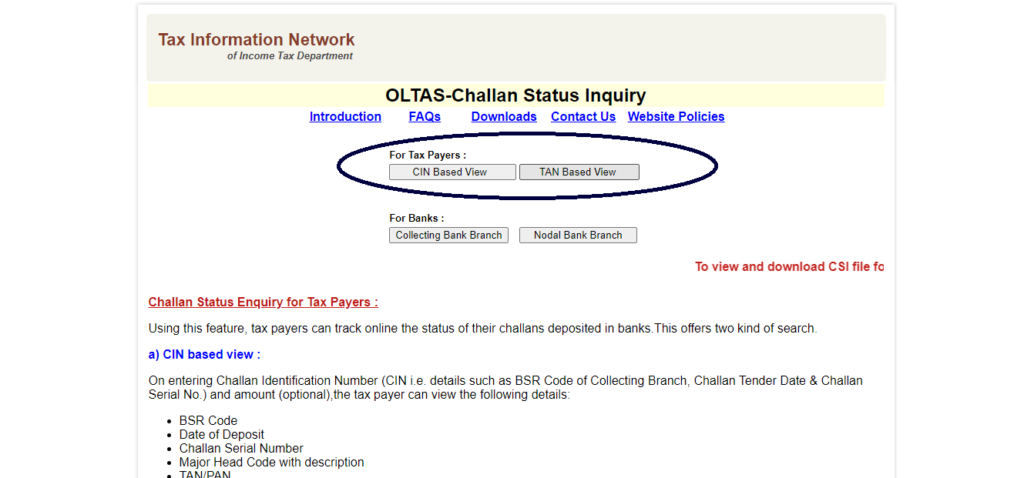

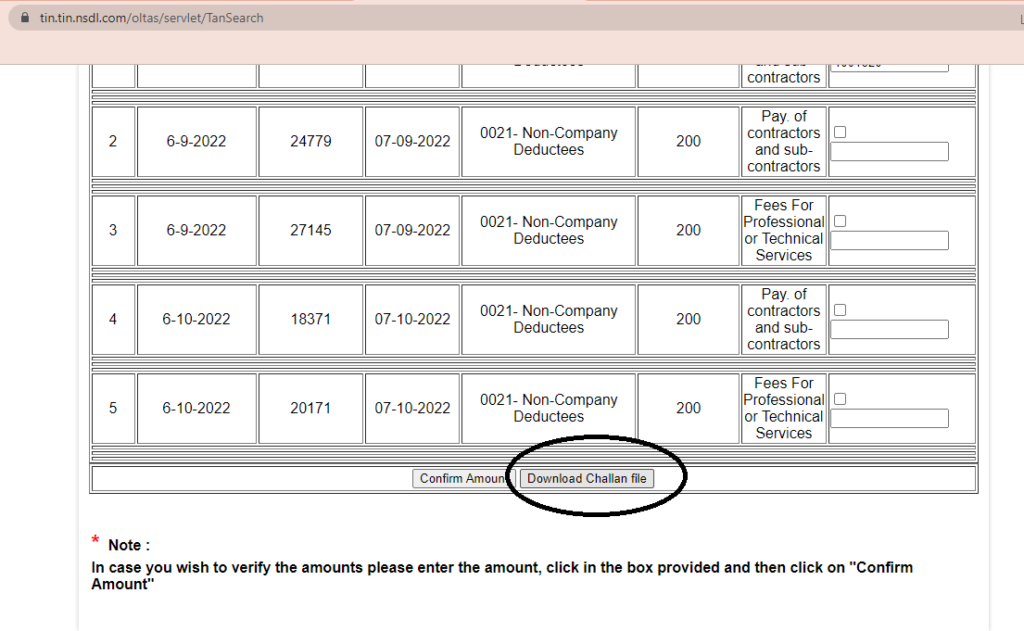

Step 2: Click on “Challan Status Inquiry” under the ‘Services‘ tab.

Step 3: We can view the challans either by providing the CIN number or the TAN number.

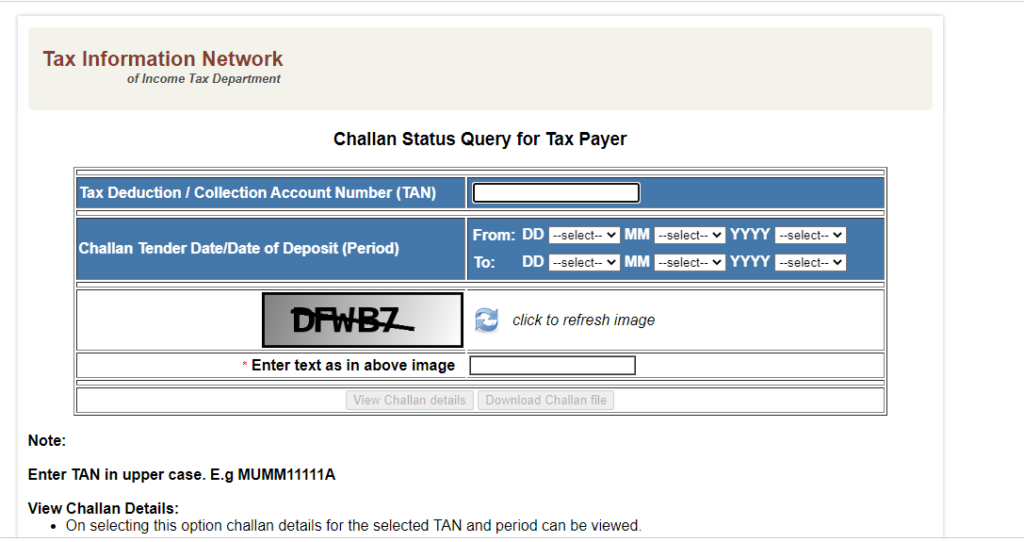

Step 4: In case of Tan Based View, fill in the details by entering the TAN number of the assessee and select the period for which you want to view the challans. Period selected should be within 24 months.

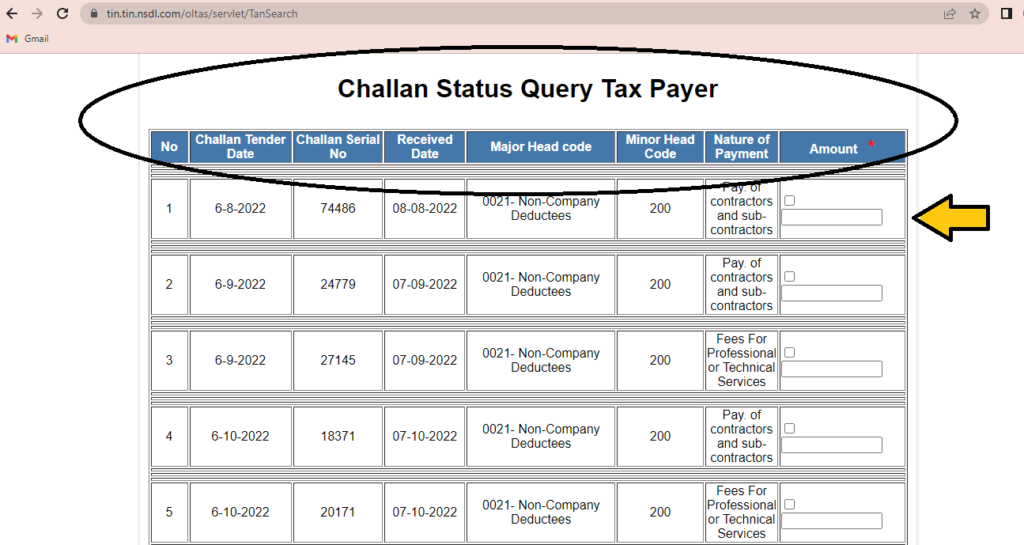

Step 5: We can view the challan details for the mentioned period as below.

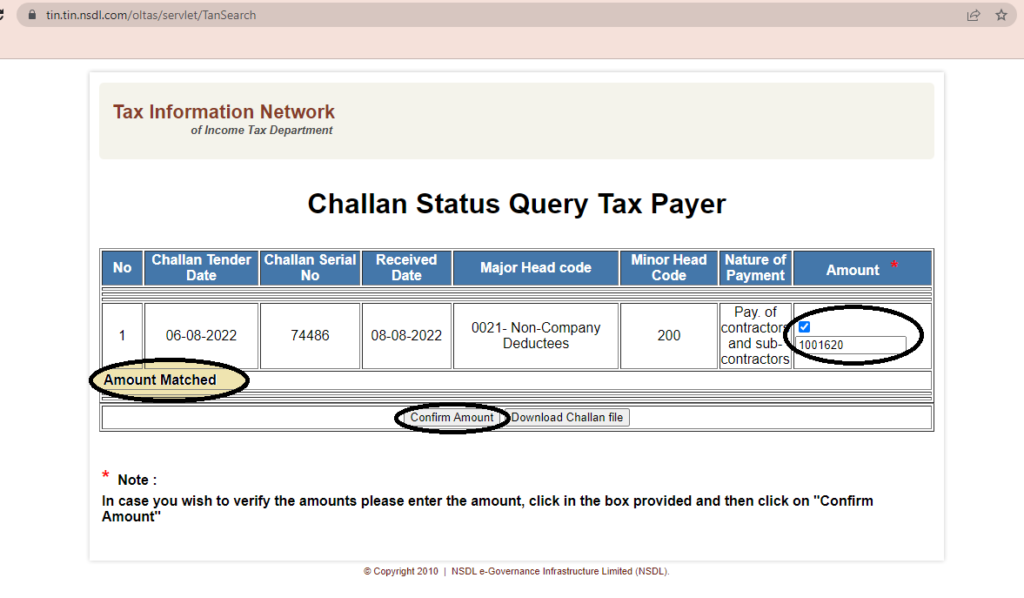

Under the given picture, the column for “Amount” has been given blank. we can enter the amount and ‘Confirm the Amount’. If the amount you have entered is correct, a text in bold would display as “Amount Matched” and vice versa.

In case you want download the challan file, click on “Download Challan File“.

A ‘csi’ file would be created, you can use that csi file for verifying the challan details while filing TDS returns.

According to section 2(13) of the Income Tax Act, the term “business” is defined as any trade, commerce, or manufacture or any adventure or concern in the nature of trade, commerce or manufacture.”

The term `Business’ means an activity being carried on continuously and systematically by a person with the application of his labor or skill with a view to earn income. The expression “business” does not necessarily mean trade or manufacture only, it has a much wider meaning. Business simply means any economic activity being carried on for earning profits. In any business, repetition of transactions or continuity of similar transactions is not a necessary element. Transactions may not be regular in nature.

The following activities have been considered as ‘Business’:

Advertising agent

Clearing, forwarding and shipping agents

Couriers

Insurance agent

Nursing home

Stock and share broking and dealing in shares and securities

Travel agent

DEFINITION OF PROFESSION

The term ‘Profession’ is defined under Section 2(36) of the Act Profession also includes vocation which is only a way of living. “Profession” involves the idea of an occupation requiring purely intellectual skill or manual skill controlled by the skill of the operator, as distinguished from an operation which is substantially the production or sale or arrangement for the production or sale of commodities.

Classification of any activity as ‘business’ or ‘profession’ will depend on the facts and circumstances of each case.

As per Section 44AA of the IT Act, the following have been considered as ‘Profession‘:

legal,

medical,

engineering,

architectural profession,

the profession of accountancy,

technical consultancy or

interior decoration.

Further under Rule 6F and other professions notified thereunder, the following activities can also be considered as a ‘Profession‘:

(i) Authorized Representative,

(ii) Company Secretary,

(iii) Film Artists/Actors, Cameraman, Director including an assistant director; a music director, including an assistant music director, an art director, including an assistant art director; a dance director, including an assistant dance director; Singer, Story-writer, a screen-play writer, a dialogue writer; editor, lyricist and dress designer,

(iv) Information Technology.

DIFFERENCE BETWEEN BUSINESS AND PROFESSION

PARTICULARS

BUSINESS

PROFESSION

MEANING

An economic activity where people sell goods or services.

An economic activity where people work with their knowledge and skills.

QUALIFICATION

No minimum qualification is required.

Educational or professional degree or specified knowledge is required.

TRANSFER OF INTEREST

Transfer of interest is possible.

Generally, transfer of interest is not possible.

ACCOUNTING TYPE

Generally, Manufacturing / Trading / Profit & Loss a/c is maintained.

Generally, Income & Expenditure a/c is maintained.

REWARD

Reward for business is known as ‘profit’.

Reward for profession is known as ‘professional fee’.

TAX AUDIT U/S 44AB

Applicable if annual turnover or gross receipt exceeds Rs. 1crore (Rs.2 crore for presumptive income scheme u/s 44AD).

Applicable if gross receipt exceeds Rs. 50 lakhs.

FAQs

1. Are Nursing Homes and Hospitals a Business or a Profession?

If Nursing Home or Hospital is owned by an Individual then it will be treated as ‘Profession’. But if it is owned by a Company or a firm then it will be treated as ‘Business’ because an artificial body like a company or a firm cannot possess any personal skills required to practice in a profession.

2. Teaching institutes are Business or Profession?

Same logic will be applicable in case of teaching institutes. Teaching is a profession as specified skills are required to teach any student/class. But in case of a teaching institution, it is an artificial body, and hence, it will be considered as a business. But a teaching institution can be considered as a Profession if it is owned by an individual.

SECTION 115BBH – TAX ON INCOME FROM VIRTUAL DIGITAL ASSETS

As per Section 115BBH, virtual digital assets (cryptocurrencies and non-fungible tokens) would be taxed at a flat rate of 30% on profits. This section will be effective from 1st April, 2023 and will accordingly apply in relation to the assessment year 2023-24 (Financial Year 2022-23) and subsequent assessment years.

Tax shall be levied in the same manner as winnings from horse races or other speculative transactions are treated.

No deduction will be allowed in respect of such income from virtual digital assets except for the deduction as “Cost of Acquisition”.

Cost of Acquisition does not include infrastructure cost which might be incurred on mining crypto assets.

Losses incurred from one virtual digital currency cannot be set-off against any income, not even from the income from another digital currency. However, Rebate under section 87A is available.

If any person receives Digital Currency as a gift, it would be taxable in the hands of recipient.

SECTION 194S – TDS ON VIRTUAL DIGITAL ASSETS

The Finance Bill, 2022 has inserted a new section 194S which requires to deduct tax at source (TDS) @ 1% on the purchase consideration on transfer on virtual digital asset to any resident. Section 194S is effective from 1st July, 2022.

TDS @ 1% shall be paid irrespective of profit or loss on Virtual Digital Asset (mainly cryptocurrencies). Virtual Digital Asset is defined under Section 2(47A). In case of transfer of virtual digital assets, tax shall be deducted from the gross amount of consideration paid to the resident person.

However, in some cases, before releasing the consideration, the person responsible for the transfer of virtual digital asset shall ensure that tax has been paid in respect of such consideration:

Where consideration is wholly in kind;

Where a transaction is in exchange for another virtual digital asset, and there is no part in cash; or

Where consideration is partly in cash and partly in kind, but the part in cash is not sufficient to meet the liability of deduction of tax in respect of whole of such transfer.

According to Section 194S of the Income tax Act, Specified Person is defined as:

a person being an individual or Hindu Undivided Family (HUF) whose total sales, gross receipts or turnover in case of business does not exceed Rs 1 crore and in case of profession does not exceed Rs 50 lakh during the financial year immediately preceding the financial year, or

a person being an individual or Hindu Undivided Family (HUF) not having any income under the head “Profits and gains of business and profession”.

In case of Specified Person, the provisions of section 203A (Requirement to obtain Tax deduction and Collection Account Number) and 206AB (Special provision for deduction of TDS for Non-Filers of Income Tax Returns) will not be applicable.

Further, in case the payer is a Specified Person and the aggregate value of such consideration to a resident is less than Rs.50,000 during the financial year, no tax shall be deducted. However, in any other case, the threshold limit is proposed to be Rs.10,000 during the financial year.

TDS collected under Section 194S shall be deposited within 30 days from the end of the month in which the deduction has been made. Deposit of tax so deducted shall be made in the challan-cum-statement Form 26QE.

If the PAN of the deductee (buyer) is not available, then the tax at the time of transfer of VDA will be deducted at the rate of 20%. Further, if an individual has not filed his/her income tax return, then TDS will be deducted at a higher rate of 5% (as against normal rate of 1%), if the payer is not a specified person.

CIRCULAR NO. 13 of 2022 – Guidelines for removal of difficulties under sub-section (6) of section 194S of the Income-tax Act, 1961 issued by CBDT on 22nd June, 2022

Question 1. Who is required to deduct tax when the transfer of VDA is taking place on or through an Exchange and payment is made by the purchaser to the Exchange (directly or through broker) and then from the Exchange it goes to seller directly or through the broker? Answer: According to section 194S of the Act, any person who is responsible for paying to any resident any sum by way of consideration for transfer of VDA is required to deduct tax. Thus, in a peer to peer (i.e. direct buyer to seller) transaction, the buyer (i.e. person paying the consideration) is required to deduct tax under section 194S of the Act. However, if the transaction is taking place on or through an Exchange there is a possibility of tax deduction requirement under section 194S of the Act at multiple stages. Hence, in order to remove difficulties for transactions taking place on or through an Exchange, the following clarifications are issued:- (i) In a case where the transfer of VDA takes place on or through an Exchange and the VDA being transferred is owned by a person other than the Exchange: In this case buyer would be crediting or making payment to the Exchange (directly or through a broker). The Exchange then would be required to credit or make payment to the owner of VDA being transferred, either directly or through a broker. Since there are multiple players, to remove difficulty it is clarified that:

Tax may be deducted under section 194S of the Act only by the Exchange which is crediting or making payment to the seller (owner of the VDA being transferred). In a case where broker owns the VDA, it is the broker who is the seller. Hence, the amount of consideration being credited or paid to the broker by the Exchange is also subject to tax deduction under section 194S of the Act.

In a case where the credit/payment between Exchange and the seller is through a broker (and the broker is not seller), the responsibility to deduct tax under section 194S of the Act shall be on both the Exchange and the broker. However, if there is a written agreement between the Exchange and the broker that broker shall be deducting tax on such credit/payment, then broker alone may deduct the tax under section 194S of the Act. The Exchange would be required to furnish a quarterly statement (in Form no 26QF) for all such transactions of the quarter on or before the due date prescribed in the Income-tax Rules, 1962.

(ii) In a case where the transfer of VDA takes place on or through an Exchange and the VDA being transferred is owned by such Exchange: In this case there are no multiple players. The buyer is required to deduct tax under section 194S of the Act. However, there may be a practical issue as the buyer may not know whether the VDA being transferred is owned by the Exchange or not. Hence, there may be genuine doubt in the mind of buyer with regard to its responsibility to deduct tax under section 194S of the Act. This difficulty would also be there if the buyer is buying VDA from an Exchange through a broker. To remove this difficulty, it is clarified that while the primary responsibility to deduct tax under section 194S of the Act, in this case, remains with the buyer or his broker, as an alternative the Exchange may enter into a written agreement with the buyer or his broker that in regard to all such transactions the Exchange would be paying the tax on or before the due date for that quarter. The Exchange would be required to furnish a quarterly statement (in Form No. 26QF) for all such transactions of the quarter on or before the due date prescribed in the Income-tax Rules, 1962. The Exchange would also be required to furnish its income tax return and all these transactions must be included in such return. If these conditions are complied with, the buyer or his broker would not be held as assessee in default under section 201 of the Act for these transactions. For the purpose of this circular,- (i) The term “Exchange” means any person that operates an application or platform for transferring of VDAs, which matches buy and sell trades and executes the same on its application or platform. (ii) The term “Broker” means any person that operates an application or platform for transferring of VDAs and holds brokerage account/accounts with an Exchange for execution of such trades.

Question 2: Question no 1 was with respect to transactions where the consideration for transfer of VDA is not in kind. How will this operate in a situation where it is in kind or in exchange of another VDA?

Answer: According to proviso to sub-section (1) of section 194S of the Act, there could be situations where the consideration is in kind or in exchange of another VDA or partly in kind and cash is not sufficient to meet the TDS liability. In these situations, the person responsible for paying such consideration is required to ensure that tax required to be deducted has been paid in respect of such consideration, before releasing the consideration.

In the above situation, the buyer will release the consideration in kind after seller provides proof of payment of such tax (e.g. Challan details etc.). In a situation where VDA “A” is being exchanged with another VDA “B”, both the persons are buyer as well as seller. One is buyer for “A” and seller for “B” and another is buyer for “B” and seller for “A”. Thus both need to pay tax with respect to transfer of VDA and show the evidence to other so that VDAs can then be exchanged. This would then be required to be reported in TDS statement along with challan number. This year Form No. 26Q has included provisions for reporting such transactions. For specified persons, Form No. 26QE has been introduced. However, if the transaction is through an Exchange there is practical issue in implementing this provision. In order to address this practical issue and to remove difficulty, it is clarified that in such a situation, as an alternative, tax may be deducted by the Exchange. Such an alternative mechanism can be exercised by the Exchange based on written contractual agreement with the buyers/sellers. If such an alternative mechanism is exercised, (i) the Exchange would be required to deduct tax for both legs of the transactions and pay to the Government. In the Form 26Q it will, for the reasons explained before, need to report it as tax deducted on both legs of the transaction. (ii) the buyer and seller would not be independently required to follow the procedure prescribed in proviso to sub-section (1) of section 194S of the Act.

When the Exchange opts for deduction of tax under section 194S of the Act on such transactions, there is also a possibility that the tax amount deducted is also in kind and needs to be converted into cash before it can be deposited with the Government. In this regard, the following mechanism shall be adopted by the Exchange (i) At the time of transaction, the Exchange will deduct TDS in the pair being traded. For example, in case of trade for Monero to Deso, 1% of Monero and 1% Deso will be deducted as tax under section 194S of the Act by the Exchange and balance shall be transferred to the customer. The trail of transactions evidencing deduction of 1% of consideration for every VDA to VDA trade shall be maintained by the Exchange. (ii) The Exchanges shall immediately execute a market order for converting this tax deducted in kind (1% Monero/ 1% Deso in the above example) to one of the primary VDAs (BT, ETH, USDT, USDC) which can be easily converted into INR. This step will ensure that the tax deducted under section 194S of the Act in the form of non-primary VDAs like Deso/Monero is converted to an equivalent of primary VDAs which have a ready INR market. Time stamps of timing of orders to be maintained to ensure such conversion of VDAs withheld to be done on immediate basis by the Exchange. If the taxes are withheld in primary VDAs, this step would be ignored. (iii) All the tax deducted under section 194S of the Act in the form of primary VDAs {or converted into primary VDA under step (ii)} will be accumulated for the day. Time limit will be from 00:00 hours to 23:59 hours. VDA accumulation by the Exchange shall be verifiable from the trail of orders for VDA to VDA trades executed during the day. (iv) The accumulated balance of primary VDAs at 00.00 hours will be converted into INR based on the market rate existing at that time. In order to bring in consistency and to avoid discretion, the Exchanges are required to place market order at 00:00 hours for the tax withheld {or converted under step (ii)} in form of primary VDAs for conversion into INR. These sell market orders shall be executed based on the open buy orders in the market. Price and quantity data for every matched trade shall be maintained by the Exchange and shall be available for verification. It shall be verifiable from the system coding that the conversion into INR happened at the first available buy order based on the prevailing buy order book of the respective Exchange at the time of conversion. As a practice, the respective Exchange liquidating the VDA shall be prohibited to be a buyer for these VDAs.

(v) Customer will be issued a contract note over email which will include the amount of tax withheld in kind under section 194S and the amount of INR realized from such tax withheld. (vi) The tax withheld in kind under section 194S of the Act and converted into INR by following the above procedure shall be deposited in the Government Account as per the time line and process given in the Income-tax Rules 1962. It is clarified that there would not be any further TDS for converting the tax withheld in kind in the form of VDA into INR or from one VDA to another VDA and then into INR.

Question 3: Whether the provision of section 194Q of the Act is also applicable on transfer of VDA? Answer Without going into the merit whether VDA is goods or not, it is clarified that once tax is deducted under section 194S of the Act, tax would not be required to be deducted under section 194Q of the Act.

Question 4: Whether the consideration for transfer of VDA shall be on Gross basis after including GST/commission or it shall be on “net basis” after exclusion of these items.

Answer: In order to remove difficulty, it is clarified that the tax required to be withheld under section 194S of the Act shall be on the “net” consideration after excluding GST/charges levied by the deductor for rendering service.

Question 5: In transactions where payment is being carried out through payment gateways, there may be tax deduction twice.

To illustrate that a person ‘X’ is required to make payment to the seller for transfer of VDA. He makes payment of one lakh rupees through digital platform of “ABC”. On these facts liability to deduct tax under section 194S of the Act may fall on both “X” and “ABC. Is tax required to be deducted by both? Answer: In order to remove this difficulty, it is provided that in the above example, the payment gateway will not be required to deduct tax under section 194S of the Act on a transaction, if the tax has been deducted by the person (‘X’) required to make deduction under section 194S of the Act. Hence, in the above example, if “X” has deducted tax under section 194S of the Act on one lakh rupees, “ABC” will not be required to deduct tax under section 194S of the Act on the same transaction. To facilitate proper implementation, “ABC” may take an undertaking from “X” regarding deduction of tax.

Question 6: Section 194S shall come into effect from the 1st July 2022. The liability to deduct tax under section 194S of the Act applies only when the value or aggregate value of the consideration for transfer of VDA exceeds fifty thousand rupees during the financial year in case of consideration being paid by specified person and ten thousand rupees in other cases. It is not clear how this limit of fifty thousand (or ten thousand) is to be computed? Answer: It is clarified that,-

(i) Since the threshold of fifty thousand rupees (or ten thousand rupees) is with respect to the financial year, calculation of consideration for transfer of VDA triggering deduction under section 194S of the Act shall be counted from 1st April, 2022. Hence, if the value or aggregate value of the consideration for transfer of VDA payable by a person exceeds fifty thousand rupees (or ten thousand rupees) during the financial year 2022-23 (including the period up to 30th June 2022), the provision of section 194S of the Act shall apply on any sum, representing consideration for transfer of VDA, credited or paid on or after 1st July 2022. (ii) Since the provision of section 194S of the Act applies at the time of credit or payment (whichever is earlier) of any sum, representing consideration for transfer of VDA, such sum which has been credited or paid before 1st July 2022 would not be subjected to tax deduction under section 194S of the Act.

Disclaimer: The content/information published on the website is only for general information of the user and shall not be construed as legal advice. While we have exercised reasonable efforts to ensure the veracity of information/content published, we shall be under no liability in any manner whatsoever for incorrect information, if any.

Section 194R of the Income Tax Act has been inserted in the Finance Act 2022 which is applicable from 1st July 2022. Government has introduced section 194R keep a check on tax leakage. This section requires for deducting tax at source (TDS) in respect of business or profession on Benefits or Perquisites. Benefit/Perquisite can be either in kind or in combination of cash and kind.

Section 28(iv) of the Income Tax Act, 1961 provides that the value of any benefit or perquisite, whether convertible into money or not, arising from business or exercise of profession is to be charged as Business Income in the hands of the recipient of such benefit or perquisite.

APPLICABILITY

Section 194R of the Income Tax Act is applicable to

All assessee (other than Individuals and HUF)

Individuals and HUF whose Turnover exceeds Rs.1 Crore or Professional Receipts exceeds Rs.50 Lakhs.

Any person providing benefit or perquisite to a Resident.

NON-APPLICABILITY

Provision of Section 194R is not applicable if the benefit or perquisite is provided to any Government entity.

Section194R is not applicable on the benefits given on occasions like festivals, marriage, etc. It is applicable only on benefits and perquisites arising out of business or profession of any resident.

As gift/ perks/ benefits, i.e., any benefit/perquisite provided to Resident employee will be added in salary and TDS will be deducted U/s 192 So provisions of Sec 194R is Not applicable in given case.

TAX RATE & THRESHOLD LIMIT

Any benefit or perquisite arising from business or profession whose aggregate value exceeds Rs.20,000 in the financial year will fall under Section194R and shall have to pay TDS @ 10%. TDS should be deducted before providing such benefit or perquisite.

To calculate the threshold limit, benefits or perquisites for the whole year shall be taken into consideration. In other words, we can say that benefits or perquisites shall be calculated from 1st April, 2022.

However, the benefit or perquisite which has been provided before 30st June, 2022 would not be subject to tax deduction under section 194R. Only the value of benefits or perquisites which are provided after 1st July, 2022 shall be liable for deducting tax at source at the rate of 10%.

CASE STUDIES

M/s PQR Limited/ PQR (Partnership Firm/AOP/BOI/Trust/Co-operative society), or Mr. PQR (Individual/HUF) having Turnover above Rs.1,00,00,000 or Professional Receipts above Rs. 50,00,000 in FY 2021-22 AY 2022-23 provides Gold Coins/ Holiday Package/ Coupons/Laptops/etc. to its dealers who is:

Case 1: Resident Person, provided with a holiday package amounting to Rs.40,000 +GST on 15/05/2022.

APPLICABILITY

REASON

Not Applicable

Since the benefit/gift/perquisite is provided before 1st July,2022, this section will not be applicable.

Case 2: Resident Person, provided with a holiday package amounting to Rs.40,000 +GST on 15/07/2022.

APPLICABILITY

REASON

Applicable

Since the benefit/gift/perquisite is provided after 1st July,2022, this section will be applicable and TDS will be payable @10%.

Case 3: Resident Person, provided with a holiday package amounting to Rs.10,000 +GST on 15/05/2022 and Gold Chain worth Rs.16000 on 31/07/2022.

APPLICABILITY

REASON

Applicable

Since the Gold chain is provided after 1st July,2022 and the aggregate value exceeds the threshold limit of Rs.20,000, i.e., 10,000 before 01/07/2022 and 16,000 after 01/07/2022, this section will be applicable but TDS will be payable only on the value of Gold chain which is Rs.16,000 @10%.

Case 4: Resident Person, provided with a holiday package amounting to Rs.10,000 +GST on 15/05/2022 and Gold Chain worth Rs.25000 on 31/07/2022 on the occasion of marriage

APPLICABILITY

REASON

Not Applicable

As the Gold chain provided after 1st July,2022 is on the occasion of marriage and not from business/profession, it would not be included in the aggregate value. And therefore, aggregate value does not exceed the threshold limit of Rs.20,000, so Section 194R will not be applicable.

Case 5: M/s ABC Limited (Resident Dealer) was provided with Gold Coin Worth Rs.15000 on 31/07/2022 on achieving target for FY 2021-22 and being impressed with Mr. B (employee of M/s ABC) performance it provided Silver Coins amounting to Rs.10,000 + GST to Mr. B on 31/07/2022 as gift.

APPLICABILITY

REASON

Not Applicable

As the Gold coin provided after 1st July,2022 does not exceed the aggregate value of Rs.20,000, section 194R will not be applicable on M/s ABC Ltd. Silver coins worth Rs.10,000 is not in relation with business and is provided under his personal capacity. Hence it shall not be included in the calculation of aggregate value. Therefore, Section 194R is not applicable to either Mr. B or M/s ABA Ltd.

VALUATION

It has been clarified that the valuation of benefit/perquisite shall be made at the fair market value of that benefit or perquisite.

However, if the deductor has purchased that benefit from an outside party, the value of benefit/perk will be equal to the purchase price to the deductor. And in case the deductor manufactures the same, value of benefit/perk would be equal to the market price of such item.

FAQs

Q1. Whether sales discount will attract TDS under this section?

Since sales discount are ordinary selling expenditure and are incurred as incentives to distributors for meeting sales targets, so it does not constitute as benefit or perquisite. Therefore, Section 194R will not be applicable.

Q2. Does Section194R applies to Capital Assets?

Capital Assets like car, land, etc. are taxable as benefit or perquisite and thus capital assets are covered under the ambit of section 194R.

Q3. Does Section 194R attracts taxability for free samples of medicines given to doctors?

Section 194R will be applicable to doctors or hospitals if they are receiving free samples of medicines.

Q4. Does the valuation of benefit or perquisite include GST?

The CBDT has clarified that GST will not be included for the purposes of valuation of benefit/perquisite for TDS under section 194R.

Q5. Under which head would it be taxable in the hands of the Receiver?

It would be taxable as business income under the head Business and Profession.

Q6. Many a times, a social media influencer is given a product of a manufacturing company so that he can use that product and make audio/video to speak about that product in social media. Is this product given to such influencer a benefit or perquisite? In case of benefit or perquisite being a product like car, mobile, outfit, cosmetics etc and if the product is returned to the manufacturing company after using for the purpose of rendering service, then it will not be treated as a benefit/perquisite for the purposes of section 194R of the Act. However, if the product is retained then it will be in the nature of benefit/perquisite and tax is required to be deducted accordingly under section 194R of the Act.

Q7. Whether reimbursement of out of pocket expense incurred by service provider in the course of rendering service is benefit/perquisite? Any expenditure which is the liability of a person carrying out business or profession, if met by the other person is in effect benefit/perquisite provided by the second person to the first person in the course of business/profession.

Let us assume that a consultant is rendering service to a person “X” for which he is receiving consultancy fee. [n the course of rendering that service, he has to travel to different city from the place where is regularly carrying on business or profession. For this purpose, he pays for boarding and lodging expense incurred exclusively for the purposes of rendering the service to “X”. Ordinarily, the expenditure incurred by the consultant is part of his business expenditure which is deductible from the fee that he receives from company “X”. In such a case, the fee received by the consultant is his income and the expenditure incurred on travel is his expenditure deductible from such income in computing his total income. Now if this travel expenditure is met by the company “X”, it is benefit or perquisite provided by “X” to the consultant.

However, sometimes the invoice is obtained in the name of “X” and accordingly, if paid by the consultant, is reimbursed by “X”. In this case, since the expense paid by the consultant (for which reimbursement is made) is incurred wholly and exclusively for the purposes of rendering services to “X” and the invoice is in the name of “X”, then the reimbursement made by “X” being the service recipient will not be considered as benefit/perquisite for the purposes of section 194R of the Act. If the invoice is not in the name of “X” and the payment is made by “X” directly or reimbursed, it is the benefit/perquisite provided by “X” to the consultant for which deduction is required to be made under section 194R of the Act.

Disclaimer: The content/information published on the website is only for general information of the user and shall not be construed as legal advice. While we have exercised reasonable efforts to ensure the veracity of information/content published, we shall be under no liability in any manner whatsoever for incorrect information, if any.

Buyback of Shares is also known as Share Repurchase. The name itself suggests that buyback refers to the buying back of shares by the company from the shareholders in the open market at a premium. The repurchased shares are cancelled by the company and hence, reduce the outstanding shares in the market. Tax on Buyback of shares is now regulated by Section 115QA of the Income Tax Act,1961.

WHY DO COMPANIES BUYBACK SHARES?

Correction of Share Price: Buyback of Shares generally results in increase in the market price. So, if the market price of the shares is highly undervalued, the company can correct it by buying back of shares.

Promoter’s Shareholding: One of the main reasons behind buyback of shares is to increase the shareholding of the promoters by purchasing from the open market.

Attractive Financials: With the reduced number of shares from buyback, Earnings per share of the company would increase. It also helps in improving the key financial ratios.

Utilization of Excess Cash: By buyback of shares, company can use their excess cash balance by paying premium to the shareholders over and above the market price.

INCOME TAX ON BUYBACK ON SHARES AS PER SECTION 115QA

Initially, Section 115QA was applicable only to Unlisted companies but in the Union Budget 2019, it was announced that this section is now applicable to Listed companies also. The effect of this was applicable from 1st July, 2019.

As per Section115QA, all the companies (both listed and unlisted) have to pay tax at the rate of 20% (plus Surcharge @ 12% and HEC @4%).

Companies have to pay tax on the amount of distributed income on the buyback of shares.

The tax shall be paid within 14 days from the date of payment to the shareholders.

The amount of tax paid is not available for any credit.

Every company shall pay tax on the distributed income in case of buyback of shares even if that company is not liable to pay income tax.

As per Section 115QA read along with Section 10(34A), shareholders are exempt from any kind of tax on buyback of shares. It would have been considered as double taxation if both shareholders and companies have to pay tax on buyback of shares. Therefore, only companies are liable to pay tax on buyback of shares.

TAX LIABILITY

BEFORE AMENDMENT

POST AMENDMENT (2019)

COMPANY (Both Listed and Unlisted)

No Tax Liability

The company is now liable for a buyback tax of 20% on the Distributed Income*

INDIVIDUAL SHAREHOLDER

Individual shareholders must pay Capital Gains Tax (Long term or Short term) depending on the holding period of shares

No Tax Liability

*Rule 40BB of Income Tax Act 1962 contains the procedure for the calculation of Distributed Income in different cases.

Computing the turnover on Futures and Options is significant for the purpose of tax filing and F&O trading is mostly reported as business income while filing tax returns. Yet, one needs to analyze their total income, which can be positive or negative value (profit or loss). Expenses like office rent, telephone expenses, broker’s commission, etc. which are directly connected to F&O business should be deducted from the income. The remaining amount would be considered as the turnover from the F&O trading.

Traders are often faced with the challenge of calculating trading turnover from Derivatives and Intra-day. So, following are the formulas, using which, we can calculate the turnover:

TYPE OF TRADING

CALCULATION OF TRADING TURNOVER

TAXABLE UNDER THE HEAD

RATES

Equity Trading Intra-day

Absolute Profit/Loss [Sale price – Buy price]

Speculative Business Income

Respective Slab Rate

Futures – Equity, Commodity, Currency

Absolute Profit/Loss [Sale price – Buy price]

Non-Speculative Business Income

Respective Slab Rate

Options – Equity, Commodity, Currency

Absolute Profit/Loss* + Premium received from Sale of Options

Non-Speculative Business Income

Respective Slab Rate

Equity Delivery** Trading & Mutual Fund Trading

Total Sales Value of Shares/ Mutual Fund

Capital Gain

LTCG@10% STCG @15%

Debt Funds***

Total Sales Value of Debt Fund

Capital Gain

LTCG@20% with indexation STCG @ respective slab rate

Respective slab rates as per Equity and Debt Orientation

*Profit & Loss both here are taken as positive figures.

**In case of Equity Funds, if the holding period is less than one year, it would be treated as Short Term Capital Gain.

***In case of debt funds, if the holding period is less than 3 years, it would be treated as Short Term Capital Gain.

We should understand this with the help of some examples:

Case 1: If Saurabh purchases 500 quantity of Equity Shares @Rs.50 and sells at Rs.57 on the same day (intra-day). His turnover would be determined as:

PARTICULARS

CALCULATION

AMOUNT

Profit on Sale of Shares

500 * (57-50)

3,500

Case 2: If Saurabh purchases 500 quantity of Futures @Rs.600 and sells at Rs.620. His turnover would be determined as:

PARTICULARS

CALCULATION

AMOUNT

Profit on Sale of Futures

500 * (620-600)

10,000

Case 3: If Saurabh buy 500 quantities of Options A @Rs.80 each and sells them at Rs.77. and he also purchases 250 quantity of Options B @ Rs.60 and sells at Rs.62. His turnover would be determined as:

PARTICULARS

CALCULATION

AMOUNT

Loss on Sale of Options A

500 * (80-77)

1,500

Premium on Sale of Options A

500 * 77

38,500

Profit on Sale of Options B

250 * (62-60)

500

Premium on Sale of Options B

250 * 62

15,500

Total Turnover

56,000

Case 4: If Saurabh buy 500 quantities of Equity Share A @Rs.80 each and sells them at Rs.87 after 13 months. He also purchased 250 quantity of Equity Share B @ Rs.60 and sells at Rs.62 after 4 months. His turnover would be determined as:

PARTICULARS

CALCULATION

AMOUNT

LTCG on Sale of Equity Share A

500 * (87-80)

3,500

STCG on Sale of Equity Share B

250 * (62-60)

500

Total Capital Gain

4,000

Note: Equity Share A has been taken under Long Term Capital Gain (LTCG) since they have been held as investment for more than one year.

F&O LOSSES AND TAX AUDIT

Intra-day stock trading is taxable under the head Speculative income/loss. Speculative loss can be adjusted only against the speculative income. However, any unadjusted speculative loss can be carried forward up to 4 years. F&O trading income/loss is covered under Non-Speculative business income. Any unadjusted business loss can be carried forward for 8 assessment years.

Tax Audit u/s 44AB is applicable when the trading turnover exceeds Rs.1 crore, but if the taxpayer has opted for presumptive taxation scheme, the limit for turnover is Rs.2 crores.

CONCLUSION

F&O trading has turned into an appealing proposition because of the accessibility of numerous trading platforms. Taxpayers often get confused while filing taxes about the income generated by F&O trading, and it is vital to comprehend the process to ascertain F&O turnover for income tax purposes, and when tax audit is applicable.

Section 40(B) of Income Tax Act provides the maximum permissible amount payable to a partner in a partnership firm. The returns of a partner can be in the form of

Interest on Capital: Interest payable to partners shall be in accordance with the terms of the partnership deed, however, it shall not exceed 12% per annum.

Share of Profit

Remuneration: Remuneration payable to partners shall be in accordance with the terms of the partnership deed

ESTIMATION OF INCOME OF PARTNER IN A FIRM

The partner’s share in the total income of firm is exempt in the hands of the partner and hence would not be included in his total income. And due to this exemption, he cannot set-off his share of profits a firm’s losses.

INTEREST PAYABLE TO PARTNERS

There are few conditions which shall be fulfilled in order to be eligible for interest payable under section 40(B):

The interest payable by a firm to its partners should be authorized by and in accordance with the partnership deed.

The interest payable by a firm to its partners should not be for a period falling prior to the date of such partnership deed authorizing the payment of such interest.

Interest payable to partners has a maximum cap of 12% per annum. Firm cannot pay any more than the prescribed limit.

Note: Interest here means simple interest and not compounding interest.

CONDITIONS FOR DEDUCTION UNDER REMUNERATION:

Remuneration to partners includes salary, bonus, commission, etc. Following conditions need to be satisfied for claiming the deduction:

Remuneration shall be allowed only to working partners. Working Partner is a partner who actively engages in conducting the business affairs of the firm.

Remuneration must be authorized by partnership deed and according to the terms of partnership deed. Clear directions must be specified in the partnership deed.

Remuneration paid to the working partners will be allowed as deduction but it should belong to the period as specified in the partnership deed. It should be related to the period of the partnership deed.

It is not allowed if tax is paid on presumptive basis under section 44AD or section 44ADA.

Remuneration payable shall be within the maximum permissible limits (as mentioned below). This limit is for total salary to all partners and not for any single partner.

CALCULATION OF BOOK PROFIT FOR PARTNER’S REMUNERATION U/S 40(B)

Book profit means the net profit as shown in the profit and loss account which is computed according to the manner laid down in the chapter IV-D. Book profit is calculated after some adjustments which are mentioned below:

Net profit as per profit and loss account

Add remuneration/salary/bonus/commission if already debited

Add Brought forward business loss, deduction under section 80C to 80U if debited to profit and loss a/c

Deduct interest if it is not deducted

Make adjustments for expenses as per section 28 to 44D.

AMOUNT OF DEDUCTION:

BOOK PROFIT (Rs.)

MAXIMUM DEDUCTIBLE AMOUNT (Rs.)

Loss

1,50,000

Profit upto Rs.3,00,000

90% of book Profit or Rs.1,50,000; whichever is more

More than Rs.3,00,000

60% of the Book profit

TAXABILITY IN THE HANDS OF PARTNERS:

Remuneration is taxable in hands of partners as Business Income. Note that remuneration to partners is distant from the share of profits payable to partner since share of profits is exempt, but remuneration is taxable in the income of partners.

Budget 2022 has hardened the income tax filing norms for regular taxpayers. Under Union Budget 2022, Nirmala Sitharaman announced that the provision of updated return is available in Section 139(8A) of the Income Tax Act. The taxpayers now have a choice to rectify their income tax return by filing an Updated Income Tax Return. The new provision allows the taxpayers to update their ITRs within two years of filing, on payment of additional taxes, in case of errors or omissions.

The Central Board of Direct Taxes (CBDT) has now notified a new Form ITR-U for documenting updated Income Tax returns in which taxpayers will have to give specific justification for filing it along with the amount of income to be offered to tax. The new Form ITR-U will be available to taxpayers for filing updated income tax returns for 2019-20 and 2020-21 fiscals.

WHO CAN FILE AN UPDATED ITR?

Any person eligible to update returns for FY 2019-20 and subsequent assessment years as per the relevant provisions of the IT Act can file the updated return via Form ITR-U. A taxpayer can file updated return only once for each assessment year.

WHAT DETAILS ARE REQUIRED TO BE MENTIONED IN ITR-U?

In ITR-U, the assessee needs to specify only the amount of additional income, under the prescribed income heads, on which tax is required to be paid. No detailed income break-up needs to be submitted, as in the case of filing regular ITR forms. The taxpayer must also determine the exact reason behind updating the return in ITR-U. Further, it is required to mention the challan details for the additional tax paid for the updated return.

PRESCRIBED DATE TO FILE FORM ITR-U

Form ITR-U can be filed only for the preceding two years of the end of relevant assessment year. The provisions of section 139(8A) have been notified and came into effect from the beginning of financial year 2022-23, hence, in the financial year 2022-23, returns for AY 2020-21 and AY 2021-22 can only be furnished under Updated return.

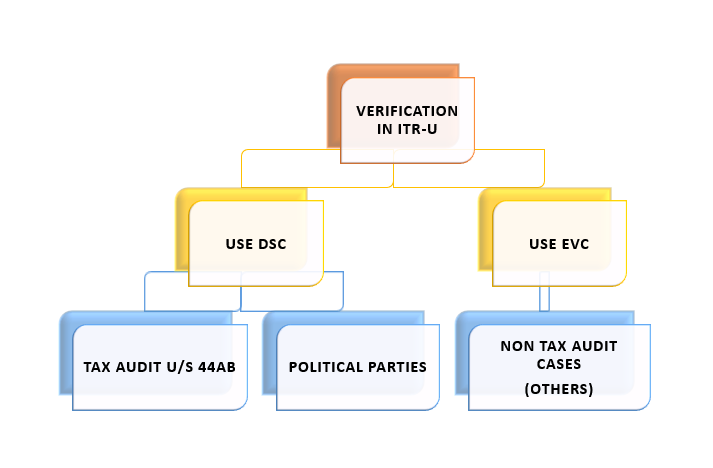

MANNER OF VERIFICATION OF UPDATED RETURN

Updated return shall be verified using Digital Signature Certificate (DSC) in case of political parties and companies who are liable for tax audit under section 44AB.

In other cases, the taxpayers have an option whether they want to file with Electronic Verification Code (EVC) or DSC.

WHAT ARE THE BENEFITS OF FILING UPDATED RETURN?

1) Taxpayer gets an additional time of 24 months to file Income Tax Return even after the due date of filing Original ITR, Belated ITR and Revised ITR have lapsed

2) Taxpayer can report any missed out incomes and pay tax on it thus reducing chances of future tax notices and litigations

3) Tax Liability and penalty under Updated Return is less than in case of proceedings for undisclosed income or income escaping assessment

CASES WHEN AN UPDATED RETURN OF INCOME CANNOT BE FURNISHED

The Form ITR-U cannot be filed in case of following reasons:

The provision does not allow the taxpayer to file the updated return if there is no additional tax outgo.

Where a search has been initiated under section 132 or requisition is made under section 132A of the Income-tax Act

Where a survey has been conducted u/s 133A other than survey u/s 133(2A) of Income-tax Act

Where any proceeding for assessment or reassessment or re-computation or revision of income is pending under the Income-tax Act

Where the Assessing Officer has information for Blank Money law, Benami law, etc. in the relevant assessment year.

Where any information is received under an agreement referred to in sections 90 or 90A of the Income-tax Act

Where any prosecution proceedings are initiated under the Income-tax Act.

PENALTY ON FILING UPDATED RETURN – PAY ADDITIONAL TAX UNDER SECTION 140B OF INCOME TAX ACT

The taxpayer filing an Updated Return must also submit proof of payment of tax and penalty as per Section 140B of the Income Tax Act.

The provision requires that the taxpayer has to pay an additional 25 per cent interest on the tax due if the updated ITR is filed within 12 months, while interest will go up to 50 per cent if it is filed after 12 months but before 24 months from the end of relevant Assessment Year. Non-payment of additional tax would be considered as invalid, and hence no return would be updated.

Therefore, the taxpayers looking to update their returns for FY 2019-20 will need to pay the tax due and interest along with an additional 50 per cent of such tax and interest. For those looking to file an updated return for FY 2020-21, the additional amount will be 25 per cent of the tax payable and interest.

NOTE: In case the taxpayer has not filed the Original return or Belated return, he/she will have to pay the taxes due for the relevant assessment year along with the late fees as per section 234F. He/she shall also pay the additional tax liability under section 140B of 25%/50% on the taxes due as per the circumstances.

A taxpayer can file an Updated ITR even if an original or belated ITR has not been filed. However, the taxpayer cannot file a Revised ITR if an original or belated ITR has not been filed

The taxpayer can file an Updated ITR only if there is an additional tax liability. In the case of a Revised ITR, there is no such restriction

The taxpayer need not pay any penalty for filing a Revised ITR. However, the taxpayer must pay a penalty in form of an Additional Tax of 25% to 50% as per Section 140B for filing an Updated ITR

Updated ITR can be filed only if there is an additional tax liability and not if there is a reduction in tax liability or an increase in the refund or claiming a loss. Revised ITR can be filed for multiple reasons such as claiming a loss, increasing refund, reduction or increase in tax liability, etc.

The taxpayer can file Revised Return multiple times while he/she can file Updated ITR only once.

Form 61A is a record of the statement of Specified Financial Transactions which must be furnished under the Income Tax Act, 1961 by certain institutions. Statement of Specified Financial Translations or SFT refers to information related to certain high-value transactions which specified persons are required to report to the income tax department. The SFT was earlier known as ‘Annual Information Return (AIR)’. The objective of SFT was to curb black money and widening the tax base.

APPLICABILITYOF FORM 61A

A banking company, Cooperative bank

A non-banking financial company (NBFC)

Any institution issuing credit card

Any person covered under audit under section 44AB of the Income Tax Act.

Post offices

A Nidhi referred to in section 406 of the Companies Act 2013

A company issuing bonds or debentures

A company issuing shares

A mutual fund institution

A company listed on the recognized stock exchange

A trustee of a mutual fund or such other person as authorized by the trustee

Authorize dealer, offshore banking unit, money changer or any other person defined in FEMA

Inspector general or sub-registrar appointed under Registration act, 1908

KEY SECTIONS OF FORM 61A

The following are the key sections and details mentioned on a typical Form 61A:

Full Name

Permanent Account Number (PAN)

Folio Number

Address

Financial Year in which the transactions carried out are being reported

Number of Specified Financial Transactions

Total Value of Specified Financial Transactions carries out in the financial year

Details of the transactions: date of transactions, name of transacting party, PAN of transacting party, full address, mode of transaction, transaction amount, transaction code, etc.

Note that transactions that must be declared and reported in Form 61A.

TRANSACTIONS TO BE REPORTED

Individuals responsible for furnishing Form 61A

Type of Transaction and limit

Banking Companies and Co-operative Banks

Cash payment for the purchase of POs (Pay orders) / DDs (Demand drafts) for amounts annually totalling Rs 10 lakh or more.

Banking Companies and Co-operative Banks

Cash payment exceeding Rs 10 lakh for purchasing any prepaid RBI instruments like RBI bonds, etc.

Banking Companies and Co-operative Banks

Deposits or withdrawals amounting to Rs 50 lakh or more from any number of current accounts of a person with the bank.

Banking Companies, Co-operative Banks and Post Offices

Deposit totalling Rs 10 lakh or more in bank accounts, other than current or time deposit accounts, of a person.

Banking Company, Co-operative Bank, Post Master General of Post office, Nidhi

Cash payment aggregating to INR 1 lakh or more in a year or Rs 10 lakh or more in any other mode of payment against any credit card bill which is issued to a customer in a year

A company or an institution issuing debentures or bonds

Receipt exceeding Rs 10 lakh or more in a year from an individual for acquiring such debentures/bonds

A company issuing shares

Receipt exceeding INR 10 lakhs in a year from an individual for acquiring such shares. This includes share application money received.

Listed companies

Share buyback from a person for an amount totalling Rs 10 lakh or more

Manager/Trustee of a Mutual Fund

Receipt equal to or exceeding Rs 10 lakh in a year from an individual acquiring the units of such Mutual Fund

A Dealer of Foreign Exchange

Receipt from a person for sale of a foreign currency or expenses incurred in such foreign currency via a debit/credit card or via the issue of draft or traveller’s cheque or any other financial instrument for an amount annually totalling Rs 10 lakh or more.

Inspector-General/Sub-Registrar appointed under the Registration Act, 1908

Sale/Purchase by a person of immovable property for Rs30 lakhs or more of sale value or value as per the stamp valuation authority.

Persons liable for audit u/s 44AB of the Income Tax Act

Cash receipt exceeding Rs 2 lakh by a person for sale of goods or rendering of services (other than the ones specified above)

DIFFERENT PARTS OF FORM 61A

Form 61A has two parts:

Part A contains statement level information which is common for all transaction types. Based on the transaction type, the report level information has to be reported in one of the following parts:

Part B (Reporting of aggregated financial transactions by the person)

Part C (Reporting of bank accounts)

Part D (Reporting of immovable property transactions)

PROCEDURE TO FILE SPECIFIED FINANCIAL TRANSACTIONS[SFT] ONLINE

Register on the Reporting portal under ‘My Account‘ menu.

All statements uploaded to the Reporting Portal should be in the XML format consistent with the prescribed schema published by the Income Tax Department.

Once XML is generated, sign and encrypt the XML using the Submission utility and prepare a package to be uploaded.

Submit the statement on Reporting Portal.

Upon successful submission, an email with “Acknowledgment Number” will be sent to the registered email id.

DUE DATE & PENALTIES

Due date for submitting Form 61A for the previous financial year is before 31st May of the applicable assessment year.

For the initial failure to file Form 61A within the due date, penalty shall be levied under Section 271A of Rs.500 per day.

The authorities would issue a notice to such an assessee, demanding the assessee to submit the form within 30 days from the issuance of such notice.

In case of continuous default even after the notice, the penalty would be levied of Rs.1,000 per day.

The penalty of Rs.1,000 would be calculated after the stipulated time as mentioned in the notice expires.

CONSEQUENCES FOR FILING DEFECTIVE FORM

If the reporting entity or individual discovers any inaccuracy or discrepancy in the information provided in Form 61A then it shall make the required corrections with the authorities within 10 days.

In case the income tax authorities fond out that the report is incomplete or defective, the reporting entity or individual is given 30 days from the date of intimation to rectify it.

Penalty of Rs.50,000 is levied on the reporting entities and individuals in case:

Inaccurate information is provided deliberately.

Inaccurate information is submitted but does not inform it and does not correct it within 10 days.

![FORM 61A [SFT] OF INCOME TAX ACT](https://consultcaonline.com/wp-content/uploads/2022/05/Copy-of-Copy-of-Thrifty-In-Transit-YouTube-Thumbnail-1.png)