According to section 2(13) of the Income Tax Act, the term “business” is defined as any trade, commerce, or manufacture or any adventure or concern in the nature of trade, commerce or manufacture.”

The term `Business’ means an activity being carried on continuously and systematically by a person with the application of his labor or skill with a view to earn income. The expression “business” does not necessarily mean trade or manufacture only, it has a much wider meaning. Business simply means any economic activity being carried on for earning profits. In any business, repetition of transactions or continuity of similar transactions is not a necessary element. Transactions may not be regular in nature.

The following activities have been considered as ‘Business’:

Advertising agent

Clearing, forwarding and shipping agents

Couriers

Insurance agent

Nursing home

Stock and share broking and dealing in shares and securities

Travel agent

DEFINITION OF PROFESSION

The term ‘Profession’ is defined under Section 2(36) of the Act Profession also includes vocation which is only a way of living. “Profession” involves the idea of an occupation requiring purely intellectual skill or manual skill controlled by the skill of the operator, as distinguished from an operation which is substantially the production or sale or arrangement for the production or sale of commodities.

Classification of any activity as ‘business’ or ‘profession’ will depend on the facts and circumstances of each case.

As per Section 44AA of the IT Act, the following have been considered as ‘Profession‘:

legal,

medical,

engineering,

architectural profession,

the profession of accountancy,

technical consultancy or

interior decoration.

Further under Rule 6F and other professions notified thereunder, the following activities can also be considered as a ‘Profession‘:

(i) Authorized Representative,

(ii) Company Secretary,

(iii) Film Artists/Actors, Cameraman, Director including an assistant director; a music director, including an assistant music director, an art director, including an assistant art director; a dance director, including an assistant dance director; Singer, Story-writer, a screen-play writer, a dialogue writer; editor, lyricist and dress designer,

(iv) Information Technology.

DIFFERENCE BETWEEN BUSINESS AND PROFESSION

PARTICULARS

BUSINESS

PROFESSION

MEANING

An economic activity where people sell goods or services.

An economic activity where people work with their knowledge and skills.

QUALIFICATION

No minimum qualification is required.

Educational or professional degree or specified knowledge is required.

TRANSFER OF INTEREST

Transfer of interest is possible.

Generally, transfer of interest is not possible.

ACCOUNTING TYPE

Generally, Manufacturing / Trading / Profit & Loss a/c is maintained.

Generally, Income & Expenditure a/c is maintained.

REWARD

Reward for business is known as ‘profit’.

Reward for profession is known as ‘professional fee’.

TAX AUDIT U/S 44AB

Applicable if annual turnover or gross receipt exceeds Rs. 1crore (Rs.2 crore for presumptive income scheme u/s 44AD).

Applicable if gross receipt exceeds Rs. 50 lakhs.

FAQs

1. Are Nursing Homes and Hospitals a Business or a Profession?

If Nursing Home or Hospital is owned by an Individual then it will be treated as ‘Profession’. But if it is owned by a Company or a firm then it will be treated as ‘Business’ because an artificial body like a company or a firm cannot possess any personal skills required to practice in a profession.

2. Teaching institutes are Business or Profession?

Same logic will be applicable in case of teaching institutes. Teaching is a profession as specified skills are required to teach any student/class. But in case of a teaching institution, it is an artificial body, and hence, it will be considered as a business. But a teaching institution can be considered as a Profession if it is owned by an individual.

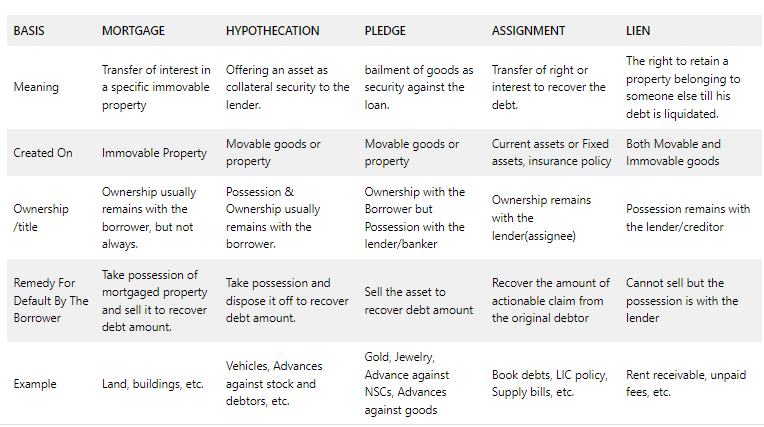

Companies Act, 2013 defines “charge” as an interest or lien created on the property or assets of a company or any of its undertakings or both as security and includes a mortgage. There are various forms of creation of charge. Some of the terms used of creation of charge are: Mortgage, Hypothecation, Pledge, etc. Although these terms are used interchangeably many times, there is different meaning attached to these words. So in this article, you will be able to understand each of the terms separately which are used in the contracts.

MORTGAGE:

A mortgage is one of the ways to create charge against immovable property where the amounts involved are generally very high, and the transfer of title is often passed. Mortgage is the transfer of interest in a specific immovable property in order to secure an existing or future debt.

The legal ownership of the asset can be transferred to the lender under mortgage if the borrower defaults on the repayment of the loan amount. However, the borrower continues to remain in possession of the property.

A mortgage is usually used for immovable assets which are permanently fixed to the earth or attached to the land like house, land, building, or any property, etc. Home loans are classified as mortgages.

The person creating the mortgage is called as Mortgagor while the person in whose favor mortgage is created (usually Banks) is called as Mortgagee.

PLEDGE:

Pledge is the bailment of goods as a security for payment of debt or performance of a promise. Bailment means delivery of goods with some purpose and with the condition that when the purpose is accomplished, the goods will be delivered back to the Bailor. Pledge is a contract between the lender and borrower, where the borrower pledges an asset as a security to the lender. Under Pledge, the ownership of the asset remains with the borrower, however, the possession of the asset is transferred to the Banker/Pledgee.

Pledge can be charged only on movable goods like stocks. The bank shall take care of the possession in good faith and as the same as its own goods.

In case of default by the borrower, the bank has a right to sell the goods in his possession with any intervention of the court and recover the amount due.

If there is any surplus while selling the asset, the amount is returned back to the pledger (borrower).

The asset can only be sold by the pledgee after giving reasonable reminder and notice to the pledgor(borrower).

In case of pledge, risk of lending comparatively reduces because possession of assets is with the lender.

Some examples of pledge are gold /jewelry loans, advance against goods or stock, advances against National Saving Certificates etc.

HYPOTHECATION:

Hypothecation is another way of creating a charge but against movable assets. Hypothecation means offering an asset as collateral security to the lender. The borrower enjoys both the ownership as well as the possession.

In the case of any default by the borrower, the lender can take the possession of the security and exercise his right to seize the asset and sell the asset to recover the dues.

The charge created under hypothecation is Equitable Charge (where there is no variation).

But in case of hypothecation of stocks to the bank, the charge which is created is called floating charge.

The common example for hypothecation is car loans. In car or vehicle loans, it remains with the borrower but the same is hypothecated to the bank or financer. If the borrower defaults, the bank then takes the possession of the car after providing sufficient notice to recover the money.

Sometimes when a bank or financial institution puts the already pledged asset as collateral for borrowing from another bank, it is called re-hypothecation.

ASSIGNMENT:

An assignment is another type of charge on current assets or fixed assets. Under assignment, the charge is created on the assets held in the books. Assignment refers to the transfer of right or interest to recover the debt.

The transferor of the claim is called as the Assignor (Borrower) and the transferee is called the Assignee (Bank).

Assignor cannot give better title to the assignee than what assignor has.

In case of default, the assignee, i.e., the bank can recover the amount of actionable claim from the original debtor without reference to the Assignor.

Assignment is possible through writing only.

Assignment can be of two types: Legal and Equitable Assignment. Legal Assignment is the agreement where all the legal formalities are done on stamp paper while in case of equitable assignment, all the formalities are written on the paper but the legal element is missing from this.

Examples of assignments include life insurance policies, books of debts, receivables, etc., which the bank can finance. For example – A bank can finance against the book debts. The borrower assigns the book debts to the bank in such a case.

LIEN:

The right to retain a property belonging to someone else till his debt is liquidated is called as Lien. Under a lien, the lender gets the right to hold up the asset used as collateral against the funds borrowed. However, unless the contract states otherwise, if the borrower defaults on the loan, the lender doesn’t have the right to sell the property.

Example: A piece of cloth is given to a tailor to stitch a suit. After the suit is made, the tailor has the right to retain it as security with him till he is paid the stitching charge by the person who placed the order for the suit. Once the payment is received, the tailor is bound to give the suit to the person concerned.

It is a right given to the creditor to retain/possess the security until the loan amount is paid. It is the strongest form of security since possession of the security is with the creditor.

Lien can be on both movable and immovable property.

But generally, lending companies choose to have mortgages on immovable property and lien on movable security like shares, gold, deposits, etc.

Examples of lien include rent receivable, unpaid fees, etc.

SET-OFF

A settlement of mutual debt between a creditor and a debtor through offsetting transaction claims is also known as setoff. In order to cover a loan in default, a bank has a legal right to seize funds of a guarantor or the debtor. The right of set-off enables the bank to combine two accounts (a loan account and a deposit account) of the same person. Through this settlement, a creditor can collect a greater amount than they usually could under bankruptcy proceedings. When a setoff clause is entered into, the bank can seize the customer’s current deposit. For purposes of set-off, all bank branches are treated as one single entity. A bank exercising a right of setoff must fulfill the following conditions:

the account from which the firm transfers funds must be held by the customer owing the firm money;

the account from which the firm transfers the money and the account from which the money would otherwise have come, must be held with the same firm;

both the accounts must be held in the same capacity by the customer;

COMPANIES (INCORPORATION) THIRD AMENDMENT RULES, 2022

Companies (Incorporation) Third Amendment Rules, 2022 has been notified on 18th August 2022 by Ministry of Corporate Affairs (MCA) to further amend the Companies (Incorporation) Rules, 2014. In this amendment, MCA has introduced a new Rule 25B, which is about Physical verification of the registered Office of the Company. However, this new Rule will come into effect once notified in the Official Gazette.

OVERVIEW OF RULE 25B

Earlier, as per Section 12 of the Companies Act 2013, physical verification of the company’s registered office was required only when ROC have reasonable grounds to believe that the company concerned is not carrying on a business. However, after the amendment in the Companies (Incorporation) Third Amendment Rules, 2022, physical verification has been implemented as per Rule 25B.

After Rule 25A (Active Company Tagging Identities and Verification), MCA has inserted new Rule 25B (Physical verification of the Registered Office of the company).

Companies (Incorporation) Third Amendment Rules, 2022 has been introduced by the government to ensure a more transparent process for the physical verification of companies’ registered addresses. According to the new Rule 25B, the Registrar of Companies (ROC), based upon the information made available on MCA 21 portal, shall visit the Address of the Registered Office of the company and do the physical verification of the Registered Office of the company.

As per the new rule 25B, ROC will carry out a physical verification of the location of the Registered Office of the company in the presence of two independent witnesses.

The Registrar shall carry the documents filed on the MCA 21 portal in support of the Address of the company’s registered office for physical verification.

To check the authenticity and validity of the documents as well as the office, the same shall be cross-verified with the copies of supporting documents of such Address collected during the physical check, duly authenticated from the occupant of the property where the Registered Office is situated.

The Registrar will also need to have a photograph of the company’s registered Office for proof during the physical verification.

If required, RoC will also seek assistance from the local police.

After conducting the verification process, a detailed report shall be prepared including all the information such as location details and photographs.

REGISTERED OFFICE OF A COMPANY

The company’s Registered Office is the main Office of the Company at which all the communication relating to the company are sent by the governmental departments. Company’s Registered Office shall be declared during company incorporation/LLP incorporation by the Directors of the company/LLP and they shall maintain all the required documents at the registered Office.

Registrar of Company (ROC) will be determined by the state or location where the Registered Office of the Company is situated.

Any change in the Company’s address/location of the Registered Office must notify the Registrar of Company (ROC) within a specified period of time.

REPORT ON PHYSICAL VERIFICATION OF COMPANIES REGISTERED OFFICE

Verification Report of the Registered Office of the company will be prepared by RoC in the given format.

Name and Company Identification Number (CIN) of the company

Latest Address of the company as per the MCA 21 records

Date of authorization letter issued by the Registrar of Companies

Name of Registrar of Companies

Date and Time of Physical verification

Location Details of Company along with the landmark

Details of person available at the time of Physical verification

Along with these details, ROC will also have to attach the following documents with the report:

Copy of agreement/ownership /rent agreement/No objection certificate (NOC) of the registered Office of the company from owner/tenant/lessor

Photograph of the Registered Office

Self-Attested ID card of the person available

NOTICE TO COMPANY AND DIRECTORS

Suppose the Registered Office is unable to receive and acknowledge all notices due to its location or any other issue. In that case, the ROC will notify the Company and all Directors of the intention to remove the company’s name from the official Register of Companies (ROC) by the way of show-cause notice and request them to send their reply along with the required documents.

The Director of the company needs to send their reply against the show-cause notice along with the necessary documents within 30 days from the date of the notice by the MCA; otherwise, ROC will have to take further action under section 248 of the Companies Act.

Special Mention Account (SMA) is an account which is exhibiting signs of incipient stress resulting in the borrower defaulting in timely servicing of her debt obligations, though the account has not yet been classified as NPA as per the extant RBI guidelines. In 2014, the classification of Special Mention Accounts (SMA) was introduced by the RBI to identify those accounts that has the potential to become an NPA/Stressed Asset. There are three types of SMA – SMA 0, SMA1 and SMA 2. They are usually categorized in terms of duration.

SMA SUB-CATEGORIES

BASIS FOR CLASSIFICATION

SMA – 0

1-30 Days

SMA – 1

31-60 Days

SMA – 2

61-90 Days

EXAMPLE:

Assuming due date for an account as 4th day of every month (say 4th Aug, 2022):

If the EMI/entire dues of a particular account are not received into the bank account before the day end process is run on the 4th calendar day i.e the due date, the account shall be treated as overdue after day end process. Accordingly, this account shall be classified as SMA-0. The account shall remain classifies under SMA-0 until the end of the 30th day.

If this account remains continuously overdue even after the completion of day end process on 30th day from the initial due date, after its classification as SMA-0, the account shall be classified as SMA-1 and shall continue to remain under this head till the 60th day.

Similarly, if the account continues to remains overdue even after the end of 60 days, it shall get classified as SMA-2 upon running of day end process on the 61st day from the initial due date. The maximum days to remain under SMA -2 is 90 days.

If the account remains continuously overdue for 90 days, it shall get classified as NPA (Non-Performing Asset) upon running of day end process on the 91st day from the initial due date.

NON-PERFORMING ASSETS (NPAs)

A non-performing asset (NPA) is a classification used by financial institutions for loans and advances that are in default or in arrears. In general, loans are classified as NPAs when the payment is outstanding for a period of 90 days or more, though some lenders can use shorter or longer time window in considering a loan or advance past due based on the conditions of the loan. A loan can be classified as a nonperforming asset at any point during the term of the loan or at its maturity.

Nonperforming assets (NPAs) are listed on the Balance Sheet of every bank or other financial institution. After a specified period of non-payment by the borrower, the lender will force the borrower to liquidate any assets that were pledged in the debt agreement. In case no assets were pledged, the lender may have to write-off the asset as a bad debt. He can also sell it at a discount to any collection agencies.

Nonperforming creates a significant burden on the balance sheet of the lender. The nonpayment of interest or principal reduces the lender’s cash flow, which can disrupt budgets and decrease earnings. Loss provisions created on loans are set aside to cover any potential losses which may occur, and it therefore reduced the capital available with the Banks. Once the defaulted loans are determined, the actual losses are written off against the earnings. Carrying a significant amount of NPAs on the balance sheet over a period of time is an indicator to regulators that the financial fitness of the bank is at risk.

PURPOSE OF NPAs

It is crucial for both the borrower as well as the lender to be aware of their assets whether they are performing or non-performing assets.

In case of the borrower, if the asset is a non-performing asset and interest payments are not done, it can affect their credit and growth possibilities in a negative way. It might hamper their ability to obtain any future borrowing.

In case of the bank/lender, interest earned on loans acts as a main source of income. Therefore, non-performing assets will affect their ability to generate adequate income and thus, their overall profitability. Keeping a track of NPAs is highly significant for banks since it will adversely affect their liquidity and growth abilities.

Non-performing assets would be manageable, but it depends on the amount of NPAs how many there are and how far they have stayed overdue. Most banks can take on a fair amount of NPAs in the short term. However, if the volume of NPAs continue to increase over a period of time, it threatens the financial health and future success of the lender.

TYPES OF NON-PERFORMING ASSETS (NPA)

Term Loans, Cash Credit and Overdraft Facilities are treated as NPA if the installment of the loan, whether principal or interest, is due for more than 90 days.

Agricultural Advances are considered as NPAs if the principal payments have stayed overdue for the specified period of time. The specified period is defined as

two or more crop seasons/harvest seasons for short duration crops, and

one crop duration for long duration crops.

There could be other types of NPAs, including residential mortgages, home equity loans, credit card loans, non-credit card outstanding, and direct & indirect consumer loans. Expected payment on any account is overdue for more than 90 days would be classifies as NPA.

CLASSIFICATION OF NPA FOR BANKS

Classification of NPAs can be done among 3 categories:

Sub- Standard Assets: Sub-standard assets are those assets that have remained NPAs for a period of less than or equal to 12 months (91 days to 12 months) and the risk of the asset is normal. Risk is significantly higher as compared to Standard Assets. Banks are generally ready to take some reductions in the market value on the loan amounts categorized under this.

Doubtful Debts: The term ‘Doubtful Debt’ itself means that there is a very low chance of recovery of its advances/loans from the party. Doubtful assets are those assets that have remained under sub-standard NPAs for a period of more than 12 months. Such advances can put the bank’s liquidity and reputation in jeopardy.

Loss Assets: The final classification of non-performing assets is loss assets. This loan is identified either by the bank itself or by an external auditor/ internal auditor. The bank, in this case, has to write off the entire loan amount outstanding.

Duty Credit Scrips is an initiative scheme introduced by the Government of India under the Foreign Trade Policy in 2015. Duty Credit Scrips were introduced to provide incentive to the Exporters to boost the inflow of forex in India. What these scrips are to exporters is same as for what vouchers are to shopaholics. These can be issues to Exporter of Goods as well as Services. Exporters get these scrips from the government for exporting goods or services outside India. These Scrips can be used to set off duties while importing to India.

The value of scrip varies from scheme to scheme, product to product and country to country. However, the scrip value in most of the cases is in the range of 2% to 5% of the realized FOB Value (in free foreign exchange). Validity of Duty Credit Scrips varies according to the nature of the scrips.

Exporters can use Duty Credit Scrips (DCS) for the payment of:

PURPOSE OF DUTY CREDIT SCRIPS

Duty Credit Scrips can be used by the exporters to pay their tax liabilities on imports, if any.

DCS are transferrable in nature. So, if the exporters do have enough imports to set off these scrips, Exporters can sell them to those who import and can set off against their own tax liabilities.

Duty Credit Scrips can also be revalidated on special request to DGFT (Directorate General of Foreign Trade) under crucial circumstances.

Duty Credit Scrips cannot be used to set-off CGST/SGST/IGST liability.

DOCUMENTS TO BE SHARED WITH AUTHORITY FOR OBTAINING DCS

Copy relating to the foreign inward remittance certificate

Copy of IEC code.

CA certificate

Copy of RCMC certificate, i.e. Registration cum membership certificate

Copy relating to the invoice

Copy of foreign exchange earned

List of directors (in case of companies)

Board resolution

WHAT IS REMISSION OF DUTIES AND TAXES ON EXPORT PRODUCTS (RoDTEP) SCHEME

A scheme designed to provide rewards to exporters to offset infrastructural inefficiencies and associated costs. The Duty Credit Scrips and goods imported/ domestically procured against them shall be freely transferable. The Duty Credit Scrips can be used for:

(i) Payment of Basic Customs Duty and Additional Customs Duty specified under sections 3(1), 3(3) and 3(5) of the Customs Tariff Act, 1975 for import of inputs or goods, including capital goods, as per DoR Notification, except items listed in Appendix 3A.

(ii) Payment of Central excise duties on domestic procurement of inputs or goods,

(iii) Payment of Basic Customs Duty and Additional Customs Duty specified under Sections 3(1), 3(3) and 3(5) of the Customs Tariff Act, 1975 and fee as per paragraph 3.18 of this Policy.

Objective of the RoDTEP scheme is to promote the manufacture and export of notified goods/ products. To apply for RoDTEP scheme, an IEC is required. Other pre-requisites as mentioned in the Chapter 3 of Foreign Trade Policy and Hand book of Procedures may be referred.

WHAT IS SERVICE EXPORTS FROM INDIA SCHEME (SEIS) SCHEME

Under the framework of the SEIS Scheme, under implementation since 01.04.2015, service exporters for eligible service categories, are granted benefits in the nature of transferable Duty Credit Scrips as a percentage of Net Foreign Exchange earned on export of the eligible services in a financial year. The Duty Credit Scrips can be used Payment of Basic Customs Duty and certain other duties as listed in para 3.02 of FTP 2015-20

Pre-Requisites for Applying for SEIS Scheme

All eligibility criteria are outlined in FTP and HBP however salient ones are:

Should have an active IEC at the time of rendering services

Should have certain minimum earnings

Should have exported eligible services as notified in Appendix 3D/3E/3X (Appendix 3X will be applicable on claim for FY 2019-20 and Appendix 3D/3E will be applicable for other year claim)

Does not fall under ineligible categories as in public notice 45 dated 05.12.2017

Services provided under Modes 1 and 2 only are allowed for claim for eligible services

Negative Net Foreign Exchange earnings (NFE) makes the entitlement under zero for the financial year

WHAT IS REBATE OF STATE AND CENTRAL LEVIES AND TAXES (RoSCTL) SCHEME

Scheme to rebate all embedded State and Central Taxes/levies for meant for exports of made-up articles & garments. Pre-Requisites for Applying for RoSCTL Scheme is that an IEC is required.

WHAT IS EXPORT PROMOTION CAPITAL GOODS (EPCG) SCHEME

The objective of the Export Promotion Capital Goods (EPCG) Scheme is to facilitate import of capital goods for producing quality goods and services and enhance India’s manufacturing competitiveness. EPCG Scheme allows import of capital goods for pre-production, production and post-production at zero customs duty. Capital goods imported under EPCG for physical exports are also exempt from IGST and Compensation Cess up to 31.03.2020. Alternatively, the exporter may also procure Capital Goods from domestic market in accordance with provisions of paragraph 5.07 of FTP. Capital goods for the purpose of the EPCG scheme shall include:

– Capital Goods as defined in Chapter 9

– Computer systems and software which are a part of the Capital Goods

– Catalysts for initial charge plus one subsequent charge

EPCG scheme covers manufacturer exporters with or without supporting manufacturer(s), merchant exporters tied to supporting manufacturer(s) and service providers.

WHAT IS TRANSPORT AND MARKETING ASSISTANCE (TMA) SCHEME

The “Transport and Marketing Assistance” (TMA) for specified agriculture products scheme aims to provide assistance for the international component of freight and marketing of agricultural produce which is likely to mitigate disadvantage of higher cost of transportation of export of specified agriculture products due to trans-shipment and to promote brand recognition for Indian agricultural products in the specified overseas markets.

To apply for TMA scheme, an IEC is required. Other pre-requisites as mentioned in the Chapter 7 of Foreign Trade Policy and Hand book of Procedures may be referred.

SALE OF DUTY CREDIT SCRIPS (DCS)

In case, the holder (Exporter) of these scrips is unable to use them for any reason, he/she can sell them in the market. Buyer (Any Importer) of the scrips would usually buy them at a discount on the face value. The buyer of the scrips would not pay the full value of the scrips. For example: If a holder has a Duty Credit Scrip worth Rs.2,00,000 and he is unable to use them, he should sell it in the market. Since the buyer of these scrips would not pay the full amount, it should be sold at a discount. The buyer may buy these scrips at Rs.1,80,000 instead of Rs.2,00,000.

Although these scrips are sold for Rs.1,80,000, It would still have the face value of Rs.2,00,000 and can be used for the payment of duties equivalent to Rs.2,00,000. The Buyer of these scrips gets the benefit of Rs.20,000 by paying Rs.1,80,000 instead of Rs.2,00,000. And the seller benefits from the transaction by encashing at least Rs.1,80,000 because the scrip would have been useless until its validity if he wouldn’t have used it or sold it.

GST ON RENTING OF IMMOVABLE PROPERTY FOR COMMERCIAL PURPOSE

Renting of any immovable property for a business or commercial purpose would attract GST @ 18% on the taxable value. In case of Commercial purpose, GST would be collected by the Owner/ Landlord and would be payable to the GST Department under forward charge mechanism.

OWNER/LESSOR

TENANT/LESSEE

GST PAYABLE

INPUT TAXCREDIT

UNREGISTERED

UNREGISTERED

NO GST

NOT APPLICABLE

UNREGISTERED

REGISTERED

NO GST

NOT APPLICABLE

REGISTERED

UNREGISTERED

GST UNDER FORWARD CHARGE PAYABLE BY OWNER

ITC CAN BE CLAIMED BY THE OWNER

REGISTERED

REGISTERED

GST UNDER FORWARD CHARGE PAYABLE BY OWNER

ITC CAN BE CLAIMED BY THE OWNER

GST ON RENT OF IMMOVABLE PROPERTY FOR RESIDENTIAL PURPOSE

GST had been exempted on renting of residential property to any person up to 17th July, 2022 but according to the recent amendment under GST Act, GST is applicable on Residential Property with effect from 18th July, 2022 Renting an immovable property is considered as a supply of service and it attracts GST @ 18%.

If any residential property is rented out to a registered person now, Tenant (i.e., the recipient) will be liable to pay tax at the rate of 18% under the reverse charge mechanism.

However, GST is not attracted if the residential property is rented out to any unregistered person and therefore no liability would arise under GST.

So, if the Tenant is registered under GST, then only GST would be liable to be paid.

In case of residential property, it does not matter if the Landlord is registered/unregistered under GST.

OWNER/LESSOR

TENANT/LESSEE

GST PAYABLE

INPUT TAX CREDIT

UNREGISTERED

UNREGISTERED

NO GST

NOT APPLICABLE

UNREGISTERED

REGISTERED

GST UNDER RCM PAYABLE BY TENANT

ITC CAN BE CLAIMED BY THE TENANT

REGISTERED

UNREGISTERED

NO GST

NOT APPLICABLE

REGISTERED

REGISTERED

GST UNDER RCM PAYABLE BY TENANT

ITC CAN BE CLAIMED BY THE TENANT

REGISTRATION

It is the choice of the landlord or the owner whether he/she wants to take registration in the same state in which the property is situated or in different state. It is left to the option of the landlord. They must identify the place of supply to decide if CGST and SGST is charged or IGST applies.

Any business whose aggregate turnover exceeds Rs.20 lakhs in a financial year has to mandatorily register under Goods and Services Tax (GST). This limit is set at Rs 10 lakhs for North Eastern and hilly states flagged as special category states.

SECTION 194I – TDS ON RENT

While talking about renting of immovable property, liability under Section 194I also attracts. Section 194I requires to deduct TDS on payment of rent to any resident (Landlord). It imposes an obligation for TDS deduction @10% on persons (other than individual/HUF) making rental payments to resident Indians above a specified limit, i.e., Rs.2,40,000 in a year. However, in case of Individuals/HUF, if the total sales/gross receipts/turnover exceeds limit as per section 44AB during the preceding financial year in which such income is credited or paid by way of rent, shall be obligated to deduct TDS @10% under this section.

The TDS is applicable both to residential and commercial properties and it shall be paid on the Gross Amount excluding GST.

TDS must be deposited by the 7th of the subsequent month except for the month of March. However, for the month of March, TDS needs to be deposited by 30th April.

FAQs

Q.1. If any Company/LLP/Firm/AOP/BOI takes a residential property for the purpose of residence to rent its employees, would it attract GST?

Residence provided to its employees will be considered as business expenditure. Therefore, GST will be paid under RCM and the ITC of the GST can be claimed by the Tenant.

Q.2. Can a composition dealer who is registered under GST claim ITC if it takes a residential dwelling for the purpose of residence on rent?

A composition dealer who is registered under GST if takes a residential dwelling for the purpose of residence on rent, it will be considered as an item of business expenditure. GST will be paid under RCM but as per section 10(4), ITC of the GST paid cannot be claimed as they pay tax at prescribed lower rates.

Q.3. What will be the treatment of GST if a proprietorship concern takes a residential property on rent for himself or his family?

When an individual who is registered under GST as a proprietorship concern takes a residential dwelling on rent for himself or his family, then it will be considered as personal expenditure and not a business expenditure. So, personal expenditure would also attract GST under reverse charge mechanism but it cannot claim ITC against the GST paid.

Q.4. When a residential dwelling is taken by a registered person on rent for commercial purpose, who will pay GST?

When a residential dwelling is taken on rent for commercial purpose by a registered person, it will be treated at par with the commercial unit. If the landlord is unregistered, then GST shall not be levied either to the landlord or the tenant. If the landlord is registered, GST will be charged on forward charge basis and the recipient can take the ITC of the same.

An Agency for Specialized Monitoring (ASM) is a mechanism of the bank, which allows it to take several steps to prevent or minimize the number of money laundering cases and misappropriation of funds. ASMs are committed to providing due diligence support in India.

ASM audits involve extensive analysis of a company’s transactions, operations, and financial health. The broad scope of ASM Audit work involves the following activities:

Stock & Receivable Audit

Cash flow Monitoring

Sales/Purchase Monitoring

End Use of Funds/Siphoning of Funds

Verification of group company transactions at arms-length

Validation of Drawing Power as per Banks’ sanctioned terms

LIE Work for Term Loans/Projects

Review of project progress vis-a-vis scheduled milestones, Capacity Utilization, asset book size, quality and diversification.

Verification of re-valuation of assets if any

Verification of routing of project revenue and expenses through designated bank accounts

Verification of project expenses, payments to creditors and advances to suppliers

Review of unbilled revenue and WIP and justifiable reasons for the same

Litigations/Contingent Liabilities including letters of comfort

Pre-disbursement verification of some specific high value transactions as the Banks may deem necessary

External Ratings, statutory and regulatory compliances, insurance cover.

Assessment of Quarterly Key Financial Indicators/Movement in stock exchanges

Movement in promoter holding in the company from time to time and percentage holding pledged to financial institutions and banks to raise capital

Any other Key Areas Review (KAR) which the Banks find necessary to be monitored

DOCUMENTS REQUIRED TO BE SUBMITTED:

The Firm / Company shall submit their application / details in the prescribed format (self-attested)

Registration with professional bodies / organizations.

GST Registration Certificate

Details of all the Key Personnel comprising their name, qualification and their education.

CV as per format provided of all key personnel, including that of technical / financial experts.

Memorandum and Articles of Association along with Certificate of Incorporation for company / registered partnership deed along with the Registrar of Firm certificate in case of partnership firms

Audited Balance sheets along with all annexure for preceding 2 years

Other documents supporting their expertise in any particular field

Letters of empanelment from other banks / financial institutions, if any

Details of projects undertaken as per format provided

Letters of assignments from other clients / lenders.

All these documents need to be complete and shall be uploaded successfully. No manual submission is required for the application under ASM.

FEE STRUCTURE FOR APPLICATION OF ASM (2022-23):

Application Fee for Fresh Empanelment is Rs.50,000 and for the Renewal of registration is Rs.25,000.

After being shortlisted, Empanelment Fee is Rs.1,00,000 for General Category and Rs.1,50,000 for Specialized category (irrespective of being fresh applicant or existing applicant).

The Fees mentioned above is non-refundable under any circumstance and exclusive of GST.

Submission of application with supporting documents (details mentioned below) by ASMs

Successful Payment of stipulated application fees by the ASMs

Scrutiny of the application and eligibility by the Working Group constituted by IBA

Finalization of eligible agencies for empanelment

Payment of stipulated Empanelment fees by the ASMs

Approval of the panel by the Managing Committee of IBA

Publication of the approved list of empaneled ASMs

Sharing of the approved panel with member banks

AFTER APPLICATION

After submitting the application, the applicant shall wait for being shortlisted. The shortlisting process would take a period of around a month.

Once shortlisted, the applicant would receive a mail from IBA for further payment of Rs.1,00,000/ Rs,1,50,000 as per the General/Special category respectively. Once the Payment has been made, it would be represented by the “Tick” on the Payment Tab.

The category (General/Special) would be decided and mentioned in the mail by the Managing Committee accordingly.

FINAL SELECTION

Once the additional amount has been paid, IBA would take minimum of 30 days to process all the applications.

The final decision shall be declared by IBA through a mail. If the firm has been empaneled for taking us ASM assignments, an empanelment letter would be attached in the mail. That empanelment letter has to be signed by the authorized signatory and shall be uploaded in the online portal under the ‘Confirmation’ tab.

With the completion of five years of India’s GST law, the GST Council has conducted its 47th Council Meeting with the presence of Finance Minister Nirmala Sitharaman. GST Council has allowed Amendments in GSTR-3B (Monthly GST return for taxpayers). Further, it permitted Auto-Population of most details in Form GSTR-3B and in Form GSTR-9 for better and easy compliance.

RELIEF TO INTRASTATE E-COMMERCE SUPPLIERS

GST Council have agreed to ease compliance bottlenecks for e-commerce suppliers. It allowed the e-commerce suppliers to register under the composition scheme for intrastate supplies easing their registration hassles and for reducing tax outgo. The new composition scheme for e-commerce suppliers for intrastate online sales will be implemented on 1st Jan 2023, once the IT system is set up. It means that such intrastate e-commerce suppliers will no longer need to obtain mandatory GST registration if their turnover does not exceed the limit of Rs.40 lakh (goods) or Rs.20 lakh (services) or such lower limits defined for some states/UTs. However, Interstate suppliers on e-commerce platforms shall have to obtain registration irrespective of turnover, compulsorily.

DEADLINE EXTENSIONS TO COMPOSITION TAXPAYERS

GSTR-4 for FY 2021-22 to get a waiver of late fee for filing up to 28th July 2022 as against earlier extension of up to 30th June 2022.

CMP-08 deadline for Apr-Jun 2022 (Q1 of FY 2022-23) to get an extension up to 30th July 2022 from 18th July 2022.

CORRECTION OF INVERTED TAX STRUCTURE

DESCRIPTION OF GOODS & SERVICES

OLD RATE

NEW RATE

Solar water heaters and systems

5%

12%

Prepared or finished leather or chamois leather or composition leathers

5%

12%

Job work for processing of hides, skins, leather, making of leather products including footwear, and clay brick manufacturing

5%

12%

Earthwork works contracts and sub-contracts to the Central and state governments, Union Territories and local authorities

5%

12%

Pawan Chakki being air-based atta chakki, wet grinder, cleaning, sorting or grading machines for seeds and grain pulses, and milling machines or cereal making machines, etc;

5%

18%

Ink for drawing, printing, and writing

12%

18%

Knives with paper knives, cutting blades, pencil sharpeners and its blades, skimmers, cake-servers, spoons, forks, ladles, etc

12%

18%

Centrifugal pumps, submersible pumps deep tube-well turbine pumps, bicycle pumps that are power-driven mainly for handling water

12%

18%

Milking machines and dairy machinery, cleaning, sorting or grading machines and its parts for eggs, fruit or other agri produce

12%

18%

Lights and fixture, LED lamps, their metal printed circuits board

12%

18%

Marking out and drawing instruments

12%

18%

Services by foreman to chit fund

12%

18%

Works contract for railways, metro, roads, bridges, effluent treatment plant, crematorium, etc.

12%

18%

Works contract and sub-contract to the Central and state governments, local authorities for canals, dams, pipelines, plants for water supply, historical monuments, educational institutions, hospitals, etc

12%

18%

GST RATE HIKES

DESCRIPTION OF GOODS & SERVICES

OLD RATE

NEW RATE

What’s costlier

Cut and Polished diamonds

0.25%

1.50%

Tetra Pack (Aseptic Packaging Paper)

12%

18%

Tar (From coal, or coal gasification plants, or producer gas plants and coke oven plants)

5%/18%

18%

GST RATE CUTS

Description of goods or services

Old Rate

New Rate

Import of tablets called Diethylcarbamazine (DEC) free of cost for National Filariasis Elimination Programme (IGST)

5%

Nil

Import of particular defence items by private businesses or suppliers for end-consumption of Defence (IGST)

Applicable rates

Nil

Ostomy Appliances

12%

5%

Orthopedic appliances such as intraocular lens, artificial parts of the body, splints and other fracture appliances, other appliances which are worn or carried, or body implants, to compensate for a defect or disability

12%

5%

Transport of goods and passengers by ropeways (with ITC of services)

18%

5%

Renting of truck or goods carriage including the fuel cost

18%

12%

*The rates will come into effect from 18th July 2022 subject to CBIC notification

SNIPPING OF GST EXEMPTIONS

DESCRIPTION OF GOODS & SERVICES

OLD RATE

NEW RATE

Earlier fully exempted, now withdrawn

Maps and hydrographic or similar charts of all kinds, including atlases, wall maps, topographical plans and globes, printed

Nil

12%

Cheques, lose or in book form

Nil

18%

Parts of goods of heading 8801

Nil

18%

Air transportation of passengers to and from north-eastern states and Bagdogra now restricted to economy class

Nil

Condition added

Transportation by rail or a vessel of railway equipment and material, storage or warehousing of commodities attracting tax such as copra, nuts, spices, jaggery, cotton, etc, fumigation in a warehouse of agri produce, services by RBI, IRDA, SEBI, FSSAI, and GSTN, renting of residential dwelling to GST-registered businesses, and services by the cord blood banks for preserving stem cells

Nil

Applicable rate

Room rent (excluding ICU) exceeding Rs.5,000 per patient day taxed without ITC

Nil

5%

Common bio-medical waste treatment facilities for treating or disposing biomedical waste shall be taxed with availability of ITC, like CETPs

Nil

12%

Hotel accommodation priced up to Rs.1,000 per day

Nil

12%

Training or coaching in recreational activities on arts or culture, or sports other than by individuals

Nil

Applicable rate

Earlier partially exempted, now withdrawn

Petroleum/ Coal bed methane

5%

12%

e-Waste

5%

18%

Scientific and technical instruments to public funded research institutes

5%

Applicable rate

*The rates will come into effect from 18th July 2022 subject to CBIC notification

SECTION 115BBH – TAX ON INCOME FROM VIRTUAL DIGITAL ASSETS

As per Section 115BBH, virtual digital assets (cryptocurrencies and non-fungible tokens) would be taxed at a flat rate of 30% on profits. This section will be effective from 1st April, 2023 and will accordingly apply in relation to the assessment year 2023-24 (Financial Year 2022-23) and subsequent assessment years.

Tax shall be levied in the same manner as winnings from horse races or other speculative transactions are treated.

No deduction will be allowed in respect of such income from virtual digital assets except for the deduction as “Cost of Acquisition”.

Cost of Acquisition does not include infrastructure cost which might be incurred on mining crypto assets.

Losses incurred from one virtual digital currency cannot be set-off against any income, not even from the income from another digital currency. However, Rebate under section 87A is available.

If any person receives Digital Currency as a gift, it would be taxable in the hands of recipient.

SECTION 194S – TDS ON VIRTUAL DIGITAL ASSETS

The Finance Bill, 2022 has inserted a new section 194S which requires to deduct tax at source (TDS) @ 1% on the purchase consideration on transfer on virtual digital asset to any resident. Section 194S is effective from 1st July, 2022.

TDS @ 1% shall be paid irrespective of profit or loss on Virtual Digital Asset (mainly cryptocurrencies). Virtual Digital Asset is defined under Section 2(47A). In case of transfer of virtual digital assets, tax shall be deducted from the gross amount of consideration paid to the resident person.

However, in some cases, before releasing the consideration, the person responsible for the transfer of virtual digital asset shall ensure that tax has been paid in respect of such consideration:

Where consideration is wholly in kind;

Where a transaction is in exchange for another virtual digital asset, and there is no part in cash; or

Where consideration is partly in cash and partly in kind, but the part in cash is not sufficient to meet the liability of deduction of tax in respect of whole of such transfer.

According to Section 194S of the Income tax Act, Specified Person is defined as:

a person being an individual or Hindu Undivided Family (HUF) whose total sales, gross receipts or turnover in case of business does not exceed Rs 1 crore and in case of profession does not exceed Rs 50 lakh during the financial year immediately preceding the financial year, or

a person being an individual or Hindu Undivided Family (HUF) not having any income under the head “Profits and gains of business and profession”.

In case of Specified Person, the provisions of section 203A (Requirement to obtain Tax deduction and Collection Account Number) and 206AB (Special provision for deduction of TDS for Non-Filers of Income Tax Returns) will not be applicable.

Further, in case the payer is a Specified Person and the aggregate value of such consideration to a resident is less than Rs.50,000 during the financial year, no tax shall be deducted. However, in any other case, the threshold limit is proposed to be Rs.10,000 during the financial year.

TDS collected under Section 194S shall be deposited within 30 days from the end of the month in which the deduction has been made. Deposit of tax so deducted shall be made in the challan-cum-statement Form 26QE.

If the PAN of the deductee (buyer) is not available, then the tax at the time of transfer of VDA will be deducted at the rate of 20%. Further, if an individual has not filed his/her income tax return, then TDS will be deducted at a higher rate of 5% (as against normal rate of 1%), if the payer is not a specified person.

CIRCULAR NO. 13 of 2022 – Guidelines for removal of difficulties under sub-section (6) of section 194S of the Income-tax Act, 1961 issued by CBDT on 22nd June, 2022

Question 1. Who is required to deduct tax when the transfer of VDA is taking place on or through an Exchange and payment is made by the purchaser to the Exchange (directly or through broker) and then from the Exchange it goes to seller directly or through the broker? Answer: According to section 194S of the Act, any person who is responsible for paying to any resident any sum by way of consideration for transfer of VDA is required to deduct tax. Thus, in a peer to peer (i.e. direct buyer to seller) transaction, the buyer (i.e. person paying the consideration) is required to deduct tax under section 194S of the Act. However, if the transaction is taking place on or through an Exchange there is a possibility of tax deduction requirement under section 194S of the Act at multiple stages. Hence, in order to remove difficulties for transactions taking place on or through an Exchange, the following clarifications are issued:- (i) In a case where the transfer of VDA takes place on or through an Exchange and the VDA being transferred is owned by a person other than the Exchange: In this case buyer would be crediting or making payment to the Exchange (directly or through a broker). The Exchange then would be required to credit or make payment to the owner of VDA being transferred, either directly or through a broker. Since there are multiple players, to remove difficulty it is clarified that:

Tax may be deducted under section 194S of the Act only by the Exchange which is crediting or making payment to the seller (owner of the VDA being transferred). In a case where broker owns the VDA, it is the broker who is the seller. Hence, the amount of consideration being credited or paid to the broker by the Exchange is also subject to tax deduction under section 194S of the Act.

In a case where the credit/payment between Exchange and the seller is through a broker (and the broker is not seller), the responsibility to deduct tax under section 194S of the Act shall be on both the Exchange and the broker. However, if there is a written agreement between the Exchange and the broker that broker shall be deducting tax on such credit/payment, then broker alone may deduct the tax under section 194S of the Act. The Exchange would be required to furnish a quarterly statement (in Form no 26QF) for all such transactions of the quarter on or before the due date prescribed in the Income-tax Rules, 1962.

(ii) In a case where the transfer of VDA takes place on or through an Exchange and the VDA being transferred is owned by such Exchange: In this case there are no multiple players. The buyer is required to deduct tax under section 194S of the Act. However, there may be a practical issue as the buyer may not know whether the VDA being transferred is owned by the Exchange or not. Hence, there may be genuine doubt in the mind of buyer with regard to its responsibility to deduct tax under section 194S of the Act. This difficulty would also be there if the buyer is buying VDA from an Exchange through a broker. To remove this difficulty, it is clarified that while the primary responsibility to deduct tax under section 194S of the Act, in this case, remains with the buyer or his broker, as an alternative the Exchange may enter into a written agreement with the buyer or his broker that in regard to all such transactions the Exchange would be paying the tax on or before the due date for that quarter. The Exchange would be required to furnish a quarterly statement (in Form No. 26QF) for all such transactions of the quarter on or before the due date prescribed in the Income-tax Rules, 1962. The Exchange would also be required to furnish its income tax return and all these transactions must be included in such return. If these conditions are complied with, the buyer or his broker would not be held as assessee in default under section 201 of the Act for these transactions. For the purpose of this circular,- (i) The term “Exchange” means any person that operates an application or platform for transferring of VDAs, which matches buy and sell trades and executes the same on its application or platform. (ii) The term “Broker” means any person that operates an application or platform for transferring of VDAs and holds brokerage account/accounts with an Exchange for execution of such trades.

Question 2: Question no 1 was with respect to transactions where the consideration for transfer of VDA is not in kind. How will this operate in a situation where it is in kind or in exchange of another VDA?

Answer: According to proviso to sub-section (1) of section 194S of the Act, there could be situations where the consideration is in kind or in exchange of another VDA or partly in kind and cash is not sufficient to meet the TDS liability. In these situations, the person responsible for paying such consideration is required to ensure that tax required to be deducted has been paid in respect of such consideration, before releasing the consideration.

In the above situation, the buyer will release the consideration in kind after seller provides proof of payment of such tax (e.g. Challan details etc.). In a situation where VDA “A” is being exchanged with another VDA “B”, both the persons are buyer as well as seller. One is buyer for “A” and seller for “B” and another is buyer for “B” and seller for “A”. Thus both need to pay tax with respect to transfer of VDA and show the evidence to other so that VDAs can then be exchanged. This would then be required to be reported in TDS statement along with challan number. This year Form No. 26Q has included provisions for reporting such transactions. For specified persons, Form No. 26QE has been introduced. However, if the transaction is through an Exchange there is practical issue in implementing this provision. In order to address this practical issue and to remove difficulty, it is clarified that in such a situation, as an alternative, tax may be deducted by the Exchange. Such an alternative mechanism can be exercised by the Exchange based on written contractual agreement with the buyers/sellers. If such an alternative mechanism is exercised, (i) the Exchange would be required to deduct tax for both legs of the transactions and pay to the Government. In the Form 26Q it will, for the reasons explained before, need to report it as tax deducted on both legs of the transaction. (ii) the buyer and seller would not be independently required to follow the procedure prescribed in proviso to sub-section (1) of section 194S of the Act.

When the Exchange opts for deduction of tax under section 194S of the Act on such transactions, there is also a possibility that the tax amount deducted is also in kind and needs to be converted into cash before it can be deposited with the Government. In this regard, the following mechanism shall be adopted by the Exchange (i) At the time of transaction, the Exchange will deduct TDS in the pair being traded. For example, in case of trade for Monero to Deso, 1% of Monero and 1% Deso will be deducted as tax under section 194S of the Act by the Exchange and balance shall be transferred to the customer. The trail of transactions evidencing deduction of 1% of consideration for every VDA to VDA trade shall be maintained by the Exchange. (ii) The Exchanges shall immediately execute a market order for converting this tax deducted in kind (1% Monero/ 1% Deso in the above example) to one of the primary VDAs (BT, ETH, USDT, USDC) which can be easily converted into INR. This step will ensure that the tax deducted under section 194S of the Act in the form of non-primary VDAs like Deso/Monero is converted to an equivalent of primary VDAs which have a ready INR market. Time stamps of timing of orders to be maintained to ensure such conversion of VDAs withheld to be done on immediate basis by the Exchange. If the taxes are withheld in primary VDAs, this step would be ignored. (iii) All the tax deducted under section 194S of the Act in the form of primary VDAs {or converted into primary VDA under step (ii)} will be accumulated for the day. Time limit will be from 00:00 hours to 23:59 hours. VDA accumulation by the Exchange shall be verifiable from the trail of orders for VDA to VDA trades executed during the day. (iv) The accumulated balance of primary VDAs at 00.00 hours will be converted into INR based on the market rate existing at that time. In order to bring in consistency and to avoid discretion, the Exchanges are required to place market order at 00:00 hours for the tax withheld {or converted under step (ii)} in form of primary VDAs for conversion into INR. These sell market orders shall be executed based on the open buy orders in the market. Price and quantity data for every matched trade shall be maintained by the Exchange and shall be available for verification. It shall be verifiable from the system coding that the conversion into INR happened at the first available buy order based on the prevailing buy order book of the respective Exchange at the time of conversion. As a practice, the respective Exchange liquidating the VDA shall be prohibited to be a buyer for these VDAs.

(v) Customer will be issued a contract note over email which will include the amount of tax withheld in kind under section 194S and the amount of INR realized from such tax withheld. (vi) The tax withheld in kind under section 194S of the Act and converted into INR by following the above procedure shall be deposited in the Government Account as per the time line and process given in the Income-tax Rules 1962. It is clarified that there would not be any further TDS for converting the tax withheld in kind in the form of VDA into INR or from one VDA to another VDA and then into INR.

Question 3: Whether the provision of section 194Q of the Act is also applicable on transfer of VDA? Answer Without going into the merit whether VDA is goods or not, it is clarified that once tax is deducted under section 194S of the Act, tax would not be required to be deducted under section 194Q of the Act.

Question 4: Whether the consideration for transfer of VDA shall be on Gross basis after including GST/commission or it shall be on “net basis” after exclusion of these items.

Answer: In order to remove difficulty, it is clarified that the tax required to be withheld under section 194S of the Act shall be on the “net” consideration after excluding GST/charges levied by the deductor for rendering service.

Question 5: In transactions where payment is being carried out through payment gateways, there may be tax deduction twice.

To illustrate that a person ‘X’ is required to make payment to the seller for transfer of VDA. He makes payment of one lakh rupees through digital platform of “ABC”. On these facts liability to deduct tax under section 194S of the Act may fall on both “X” and “ABC. Is tax required to be deducted by both? Answer: In order to remove this difficulty, it is provided that in the above example, the payment gateway will not be required to deduct tax under section 194S of the Act on a transaction, if the tax has been deducted by the person (‘X’) required to make deduction under section 194S of the Act. Hence, in the above example, if “X” has deducted tax under section 194S of the Act on one lakh rupees, “ABC” will not be required to deduct tax under section 194S of the Act on the same transaction. To facilitate proper implementation, “ABC” may take an undertaking from “X” regarding deduction of tax.

Question 6: Section 194S shall come into effect from the 1st July 2022. The liability to deduct tax under section 194S of the Act applies only when the value or aggregate value of the consideration for transfer of VDA exceeds fifty thousand rupees during the financial year in case of consideration being paid by specified person and ten thousand rupees in other cases. It is not clear how this limit of fifty thousand (or ten thousand) is to be computed? Answer: It is clarified that,-

(i) Since the threshold of fifty thousand rupees (or ten thousand rupees) is with respect to the financial year, calculation of consideration for transfer of VDA triggering deduction under section 194S of the Act shall be counted from 1st April, 2022. Hence, if the value or aggregate value of the consideration for transfer of VDA payable by a person exceeds fifty thousand rupees (or ten thousand rupees) during the financial year 2022-23 (including the period up to 30th June 2022), the provision of section 194S of the Act shall apply on any sum, representing consideration for transfer of VDA, credited or paid on or after 1st July 2022. (ii) Since the provision of section 194S of the Act applies at the time of credit or payment (whichever is earlier) of any sum, representing consideration for transfer of VDA, such sum which has been credited or paid before 1st July 2022 would not be subjected to tax deduction under section 194S of the Act.

Disclaimer: The content/information published on the website is only for general information of the user and shall not be construed as legal advice. While we have exercised reasonable efforts to ensure the veracity of information/content published, we shall be under no liability in any manner whatsoever for incorrect information, if any.

Section 194R of the Income Tax Act has been inserted in the Finance Act 2022 which is applicable from 1st July 2022. Government has introduced section 194R keep a check on tax leakage. This section requires for deducting tax at source (TDS) in respect of business or profession on Benefits or Perquisites. Benefit/Perquisite can be either in kind or in combination of cash and kind.

Section 28(iv) of the Income Tax Act, 1961 provides that the value of any benefit or perquisite, whether convertible into money or not, arising from business or exercise of profession is to be charged as Business Income in the hands of the recipient of such benefit or perquisite.

APPLICABILITY

Section 194R of the Income Tax Act is applicable to

All assessee (other than Individuals and HUF)

Individuals and HUF whose Turnover exceeds Rs.1 Crore or Professional Receipts exceeds Rs.50 Lakhs.

Any person providing benefit or perquisite to a Resident.

NON-APPLICABILITY

Provision of Section 194R is not applicable if the benefit or perquisite is provided to any Government entity.

Section194R is not applicable on the benefits given on occasions like festivals, marriage, etc. It is applicable only on benefits and perquisites arising out of business or profession of any resident.

As gift/ perks/ benefits, i.e., any benefit/perquisite provided to Resident employee will be added in salary and TDS will be deducted U/s 192 So provisions of Sec 194R is Not applicable in given case.

TAX RATE & THRESHOLD LIMIT

Any benefit or perquisite arising from business or profession whose aggregate value exceeds Rs.20,000 in the financial year will fall under Section194R and shall have to pay TDS @ 10%. TDS should be deducted before providing such benefit or perquisite.

To calculate the threshold limit, benefits or perquisites for the whole year shall be taken into consideration. In other words, we can say that benefits or perquisites shall be calculated from 1st April, 2022.

However, the benefit or perquisite which has been provided before 30st June, 2022 would not be subject to tax deduction under section 194R. Only the value of benefits or perquisites which are provided after 1st July, 2022 shall be liable for deducting tax at source at the rate of 10%.

CASE STUDIES

M/s PQR Limited/ PQR (Partnership Firm/AOP/BOI/Trust/Co-operative society), or Mr. PQR (Individual/HUF) having Turnover above Rs.1,00,00,000 or Professional Receipts above Rs. 50,00,000 in FY 2021-22 AY 2022-23 provides Gold Coins/ Holiday Package/ Coupons/Laptops/etc. to its dealers who is:

Case 1: Resident Person, provided with a holiday package amounting to Rs.40,000 +GST on 15/05/2022.

APPLICABILITY

REASON

Not Applicable

Since the benefit/gift/perquisite is provided before 1st July,2022, this section will not be applicable.

Case 2: Resident Person, provided with a holiday package amounting to Rs.40,000 +GST on 15/07/2022.

APPLICABILITY

REASON

Applicable

Since the benefit/gift/perquisite is provided after 1st July,2022, this section will be applicable and TDS will be payable @10%.

Case 3: Resident Person, provided with a holiday package amounting to Rs.10,000 +GST on 15/05/2022 and Gold Chain worth Rs.16000 on 31/07/2022.

APPLICABILITY

REASON

Applicable

Since the Gold chain is provided after 1st July,2022 and the aggregate value exceeds the threshold limit of Rs.20,000, i.e., 10,000 before 01/07/2022 and 16,000 after 01/07/2022, this section will be applicable but TDS will be payable only on the value of Gold chain which is Rs.16,000 @10%.

Case 4: Resident Person, provided with a holiday package amounting to Rs.10,000 +GST on 15/05/2022 and Gold Chain worth Rs.25000 on 31/07/2022 on the occasion of marriage

APPLICABILITY

REASON

Not Applicable

As the Gold chain provided after 1st July,2022 is on the occasion of marriage and not from business/profession, it would not be included in the aggregate value. And therefore, aggregate value does not exceed the threshold limit of Rs.20,000, so Section 194R will not be applicable.

Case 5: M/s ABC Limited (Resident Dealer) was provided with Gold Coin Worth Rs.15000 on 31/07/2022 on achieving target for FY 2021-22 and being impressed with Mr. B (employee of M/s ABC) performance it provided Silver Coins amounting to Rs.10,000 + GST to Mr. B on 31/07/2022 as gift.

APPLICABILITY

REASON

Not Applicable

As the Gold coin provided after 1st July,2022 does not exceed the aggregate value of Rs.20,000, section 194R will not be applicable on M/s ABC Ltd. Silver coins worth Rs.10,000 is not in relation with business and is provided under his personal capacity. Hence it shall not be included in the calculation of aggregate value. Therefore, Section 194R is not applicable to either Mr. B or M/s ABA Ltd.

VALUATION

It has been clarified that the valuation of benefit/perquisite shall be made at the fair market value of that benefit or perquisite.

However, if the deductor has purchased that benefit from an outside party, the value of benefit/perk will be equal to the purchase price to the deductor. And in case the deductor manufactures the same, value of benefit/perk would be equal to the market price of such item.

FAQs

Q1. Whether sales discount will attract TDS under this section?

Since sales discount are ordinary selling expenditure and are incurred as incentives to distributors for meeting sales targets, so it does not constitute as benefit or perquisite. Therefore, Section 194R will not be applicable.

Q2. Does Section194R applies to Capital Assets?

Capital Assets like car, land, etc. are taxable as benefit or perquisite and thus capital assets are covered under the ambit of section 194R.

Q3. Does Section 194R attracts taxability for free samples of medicines given to doctors?

Section 194R will be applicable to doctors or hospitals if they are receiving free samples of medicines.

Q4. Does the valuation of benefit or perquisite include GST?

The CBDT has clarified that GST will not be included for the purposes of valuation of benefit/perquisite for TDS under section 194R.

Q5. Under which head would it be taxable in the hands of the Receiver?

It would be taxable as business income under the head Business and Profession.

Q6. Many a times, a social media influencer is given a product of a manufacturing company so that he can use that product and make audio/video to speak about that product in social media. Is this product given to such influencer a benefit or perquisite? In case of benefit or perquisite being a product like car, mobile, outfit, cosmetics etc and if the product is returned to the manufacturing company after using for the purpose of rendering service, then it will not be treated as a benefit/perquisite for the purposes of section 194R of the Act. However, if the product is retained then it will be in the nature of benefit/perquisite and tax is required to be deducted accordingly under section 194R of the Act.

Q7. Whether reimbursement of out of pocket expense incurred by service provider in the course of rendering service is benefit/perquisite? Any expenditure which is the liability of a person carrying out business or profession, if met by the other person is in effect benefit/perquisite provided by the second person to the first person in the course of business/profession.

Let us assume that a consultant is rendering service to a person “X” for which he is receiving consultancy fee. [n the course of rendering that service, he has to travel to different city from the place where is regularly carrying on business or profession. For this purpose, he pays for boarding and lodging expense incurred exclusively for the purposes of rendering the service to “X”. Ordinarily, the expenditure incurred by the consultant is part of his business expenditure which is deductible from the fee that he receives from company “X”. In such a case, the fee received by the consultant is his income and the expenditure incurred on travel is his expenditure deductible from such income in computing his total income. Now if this travel expenditure is met by the company “X”, it is benefit or perquisite provided by “X” to the consultant.

However, sometimes the invoice is obtained in the name of “X” and accordingly, if paid by the consultant, is reimbursed by “X”. In this case, since the expense paid by the consultant (for which reimbursement is made) is incurred wholly and exclusively for the purposes of rendering services to “X” and the invoice is in the name of “X”, then the reimbursement made by “X” being the service recipient will not be considered as benefit/perquisite for the purposes of section 194R of the Act. If the invoice is not in the name of “X” and the payment is made by “X” directly or reimbursed, it is the benefit/perquisite provided by “X” to the consultant for which deduction is required to be made under section 194R of the Act.

Disclaimer: The content/information published on the website is only for general information of the user and shall not be construed as legal advice. While we have exercised reasonable efforts to ensure the veracity of information/content published, we shall be under no liability in any manner whatsoever for incorrect information, if any.