Gold is one of the most preferred investment options in India, available in multiple forms such as physical gold, Gold ETFs, Sovereign Gold Bonds (SGBs), digital gold, and gold mutual funds. Each form has a different tax treatment under the Income-tax Act. This article explains the taxation on sale of gold in a simple and professional manner.

1. Physical Gold (Jewellery, Coins & Bars)

Physical gold includes jewellery, coins, and bars. Tax is applicable at the time of sale based on the holding period.

• Short-Term Capital Gain (STCG): If sold within 24 months, gains are taxed as per the individual’s income tax slab. • Long-Term Capital Gain (LTCG): If held for more than 24 months, gains are taxed at 12.5% without indexation. • GST paid at the time of purchase is not refundable and forms part of the cost.

2. Gold Exchange Traded Funds (ETFs)

Gold ETFs are paper gold investments traded on stock exchanges and backed by physical gold.

• STCG: Units sold within 12 months are taxed as per income tax slab rates. • LTCG: Units sold after 12 months are taxed at 12.5% without indexation.

3. Sovereign Gold Bonds (SGBs)

Sovereign Gold Bonds are issued by the RBI on behalf of the Government of India and are considered the most tax-efficient form of gold investment.

• If held till maturity (8 years): Capital gains are completely tax-free. • If sold on stock exchange: – Within 12 months: Taxed at slab rates. – After 12 months: Taxed at 12.5% without indexation. • Interest earned (around 2.5% annually) is taxable as per slab rates.

Amendment in Finance Bill, 2026 “exemption will be applicable only to those Sovereign Gold Bonds issued by the Reserve Bank of India that are subscribed to by an individual at the time of original issue and are held continuously by such individual until redemption upon maturity” it means Capital gains exemption does not apply if bought from secondary market.

4. Digital Gold & Gold Mutual Funds

Digital gold and gold mutual funds offer convenience and flexibility but follow similar tax rules.

• STCG: If sold within 24 months, gains are taxed as per income tax slab. • LTCG: If sold after 24 months, gains are taxed at 12.5% without indexation.

Conclusion:

From a tax perspective, Sovereign Gold Bonds are the most efficient option for long-term investors, while Gold ETFs and mutual funds provide liquidity with moderate taxation. Physical gold, though culturally significant, is the least tax-efficient due to GST and higher holding period requirements.

In Tabular Format

Investment type

Short-term capital gains (STCG)

Long-term capital gains (LTCG)

Notes

Sovereign Gold Bonds (SGBs)

If sold within 12 months: taxed at slab rate

If held beyond 12 months and sold before maturity: 12.5% without indexation; Nil if held till 8-year maturity

Capital gains exemption does not apply if bought from secondary market

Gold ETFs

Up to 12 months: taxed at slab rate

Beyond 12 months: 12.5% without indexation

Treated as listed securities

Gold mutual funds

Up to 24 months: taxed at slab rate

Beyond 24 months: 12.5%

Usually invest in gold ETFs

Physical gold

Up to 24 months: taxed at slab rate

Beyond 24 months: 12.5%

GST paid cannot be set off against capital gains tax

Gifted gold

Taxable only if gift from non-relatives exceeds ₹50,000

Taxable in the recipient’s hands

Gifts from specified relatives are tax-free

Inherited gold

Capital gains apply on sale

Capital gains apply on sale

Original owner’s cost and holding period are considered

Salaried individuals who engage in stock trading or Futures & Options (F&O) transactions often have queries about income tax return filing, applicability for maintaining Books of Accounts and the applicability of tax audit on F&O transactions. This guide provides an in-depth analysis based on the latest provisions under the Income Tax Act, 1961.

Understanding Trading Transactions for Taxation

Trading in stocks or F&O can be broadly classified into two categories:

Speculative Business Transactions

Non-Speculative Transactions (F&O Trading)

1. Speculative Transactions:

As per Section 43(5) of the Income Tax Act, a speculative transaction is one where the purchase and sale of stocks or commodities are settled without actual delivery. Intraday trading in equities falls under this category.

2. Non-Speculative Transactions (F&O Trading):

F&O trading, including commodity derivatives on recognized stock exchanges, is treated as non-speculative business income even though no physical delivery takes place.

Applicability of Tax Audit for F&O Trading

Since F&O trading is considered business income, tax audit provisions under Section 44AB apply similarly to any other business income. Understanding the turnover limits and profit declaration rules is crucial for compliance.

When is Tax Audit Mandatory?

Tax audit under Section 44AB is applicable in the following cases:

Turnover up to Rs. 1 crore:

Tax audit is not required, regardless of profit or loss, provided Section 44AD(4) does not apply.

Turnover exceeding Rs. 1 crore but up to Rs. 10 crore:

Tax audit is not required if at least 95% of transactions are digital.

Tax audit is mandatory if cash transactions exceed 5% of total receipts or 5% of total payments.

Please Note Receipts and payments are calculated separately, not cumulatively.

Turnover above Rs. 10 crore:

Tax audit is mandatory, irrespective of profit or loss.

Presumptive Taxation (Section 44AD) and Tax Audit:

If a taxpayer opts for Section 44AD, no tax audit is required for turnover up to Rs. 3 crore from Financial Year 2023-24 (Assessment Year 2024-25).

However, if Section 44AD(4) applies, tax audit is required if the declared profit is less than 6% (digital) or 8% (cash) of turnover, and total income exceeds the basic exemption limit.

Tax Audit for Professionals Under Section 44ADA and F&O Traders

If a taxpayer is carrying on a profession eligible for presumptive taxation under Section 44ADA and simultaneously engaged in F&O trading, the tax audit requirement is determined separately for each activity:

For F&O trading, tax audit is applicable as per Section 44AB turnover limits discussed above.

For professionals under Section 44ADA, tax audit is applicable if gross receipts exceed Rs. 75 lakh from Financial Year 2023-24 (Assessment Year 2024-25).

If both activities are carried out simultaneously, each must be evaluated independently for tax audit applicability.

How to Calculate Turnover for F&O Trading?

Determining turnover for tax audit purposes is essential for accurate reporting. The method of turnover calculation varies based on the type of transaction:

Futures and Options (F&O) Trading: Turnover is calculated as the sum of absolute values of profits and losses from each squared-off trade during the financial year.

Options Trading: If an options contract is physically settled, the premium received on the sale is included in turnover computation.

Turnover Calculation as per ICAI Guidance Note: The calculation of turnover for tax audit purposes is guided by ICAI’s Guidance Note on Tax Audit. This method ensures uniformity in turnover computation and compliance with audit requirements.

Understanding the 5% Cash Transaction Clause Under Section 44AB

For businesses with turnover between Rs. 1 crore and Rs. 10 crore, tax audit is not required if cash receipts and cash payments do not exceed 5% of total transactions. This is computed separately as follows:

Aggregate of all cash receipts, including sales, should not exceed 5% of total receipts.

Aggregate of all cash payments, including expenses, should not exceed 5% of total payments.

If either of these conditions is violated, tax audit becomes mandatory.

Since turnover is below Rs. 1 crore, no tax audit is required unless Section 44AD(4) applies.

When is Books of Accounts Mandatory to maintain?

The Income Tax Act has specified the books of accounts that are required to be maintained for the purpose of Income Tax. These have been prescribed under section 44AA and Rule 6F.

In case business/profession is being carried out by the individual or HUF the limits are increased as under:

a. For Income – Limit is Rs. 2,50,000

b. For Turnover/Gross Receipt – Limit is Rs. 25,00,000

Tax Benefits on Losses in F&O Transactions

Losses incurred in Futures & Options (F&O) transactions can be set off against rental or interest income. Any unadjusted losses can be carried forward for up to eight years and offset against future business profits, including profits from F&O transactions.

Is Declaring F&O Loss in the Income Tax Return is Mandatory

Many taxpayers, particularly salaried individuals engaged in F&O trading, often fail to report these transactions in their income tax returns. This omission may occur due to ignorance, but it is crucial to note that reporting all sources of income is a legal requirement.

Brokers are mandated to report all security transaction details to the Income Tax Department by filing a Statement of Financial Transactions (SFT) annually. Non-disclosure of F&O transactions can attract scrutiny from the department, resulting in notices for non-compliance and potential penalties for failure to maintain books of accounts and non-filing of the required tax audit report along with the income tax return.

Notice Under Section 139(9) of the Income Tax Act (Defective Return)

Failure to furnish a Balance Sheet and Profit & Loss Account when required can lead to receiving a notice under Section 139(9) from the Centralized Processing Centre (CPC) of the Income Tax Department. The notice typically states:

“The assessee has claimed loss under the head ‘Profits and Gains of Business or Profession’; however, a Balance Sheet and Profit & Loss Account must be provided. If the assessee falls under Section 44AD/44AE/44ADA, the books of account must be audited if the income offered is below the prescribed limits as per the provisions of the Income Tax Act.”

While an audit is not mandatory if the turnover is below INR 1 crore, the income tax return must be duly filed with a complete Balance Sheet and Profit & Loss Account under Section 139 of the Income Tax Act.

Table in Glance:

Scenarios

Opted for 44AD

Declaring Profit

Remarks

1

Yes (Turnover is less than Rs. 2Cr.)

According to 44AD

Neither require to maintain books of accounts nor audit.

2

Yes (Turnover is less than Rs. 2Cr.)

Less than 8% or 6% as the case may be or declaring loss.

Require to maintain books of accounts and audit.

3

No (Turnover is less than limit given u/s 44AB)

Profit or loss whatever is the case.

No audit, maintain books of accounts if limit of 44AA is crossed.

4

No (Turnover is more than limit given u/s 44AB)

Profit or loss whatever is the case.

Audit and maintaining books of accounts is mandatory.

Note: In all the cases of loss audit is not mandatory. It depends case to case. But in general practice and to deal with future litigation this practice followed.

Disclaimer: This article is solely for educational purpose and cannot be construed as legal and professional opinion. It is based on the interpretation of the author and are not binding on any tax authority. Author is not responsible for any loss occurred to any person acting or refraining from acting as a result of any material in this article.

A Gilt Fund is a type of debt mutual fund that primarily invests in government securities (G-secs). These are bonds issued by the central and/or state governments to borrow money. As such, gilt funds carry zero credit risk, since they are backed by sovereign guarantee, but they are sensitive to interest rate movements.

Key Features of Gilt Funds:

Feature

Description

Underlying Securities

Government bonds (short to long-term maturity)

Risk Level

Low credit risk, but high interest rate risk

Return Expectation

Moderate returns, typically 5–7% p.a. over medium to long term

Investment Horizon

Ideal for 3–5 years or more

Liquidity

High, as most gilt funds are open-ended

Regulation

Regulated by SEBI

🔹 What is a Gilt Fund Account?

A Gilt Fund Account is a folio or investment account through which an investor can:

• Invest in one or more gilt funds

• Monitor NAV, holdings, and returns

• Redeem or switch between debt schemes

It may be referred to as a Mutual Fund Account with exposure specifically to Gilt Funds. Some platforms also offer direct gilt investments via RBI Retail Direct Gilt Account, allowing investors to buy G-Secs directly from RBI.

RBI Retail Direct’:

As part of continuing efforts to increase retail participation in government securities, ‘the RBI Retail Direct’ facility was announced in the Statement of Developmental and Regulatory Policies dated February 05, 2021 for improving ease of access by retail investors through online access to the government securities market – both primary and secondary – along with the facility to open their gilt securities account (‘Retail Direct’) with the RBI.

In pursuance of this announcement, the ‘RBI Retail Direct’ scheme, which is a one-stop solution to facilitate investment in Government Securities by individual investors is being issued today. The highlights of the ‘RBI Retail Direct’ scheme are:

i. Retail investors (individuals) will have the facility to open and maintain the ‘Retail Direct Gilt Account’ (RDG Account) with RBI.

ii. RDG Account can be opened through an ‘Online portal’ provided for the purpose of the scheme.

iii. The ‘Online portal’ will also give the registered users the following facilities:

Access to primary issuance of Government securities

Access to NDS-OM.

🔄 Gilt Funds vs Share Market – A Comparison

Particulars

Gilt Funds

Share Market (Equity Investment)

Nature of Investment

Government bonds (debt instruments)

Equity shares of listed companies

Risk Level

Low credit risk, high interest rate risk

High market, business & volatility risk

Returns

Moderate & stable (linked to interest rates)

Potentially high but volatile

Ideal for

Conservative or debt-oriented investors

Growth-seeking and risk-tolerant investors

Investment Horizon

Medium to long-term

Long-term (ideally >5 years)

Volatility

Low to moderate

High

Regulation

SEBI, RBI

SEBI, Stock Exchanges

Liquidity

High in open-ended funds

High for listed shares

Taxation (LTCG >2Y)

12.5% with indexation (for funds held >2 years)

12.5% LTCG on gains > ₹1.25 lakh

📈 Who Should Invest in Gilt Funds?

• Investors looking for safety of capital with moderate returns • Suitable during falling interest rate cycles (bond prices rise) • Ideal for diversification in low-risk portfolios

⚠️ Risks to Consider

• Interest Rate Risk: As rates rise, bond prices fall, affecting NAV. • No Credit Risk, but duration risk is higher in long-term gilt funds. • Not ideal for short-term parking due to volatility from rate changes.

📑 Source References:

1. SEBI – Mutual Funds Regulations: https://www.sebi.gov.in

2. RBI Retail Direct Scheme: https://rbiretaildirect.org.in

3. AMFI – Gilt Fund Details: https://www.amfiindia.com/investor-corner/knowledge-center/types-of-mutual-funds

Disclaimer: This article is solely for educational purpose and cannot be construed as legal and professional opinion. It is based on the interpretation of the author and are not binding on any tax authority. Author is not responsible for any loss occurred to any person acting or refraining from acting as a result of any material in this article.

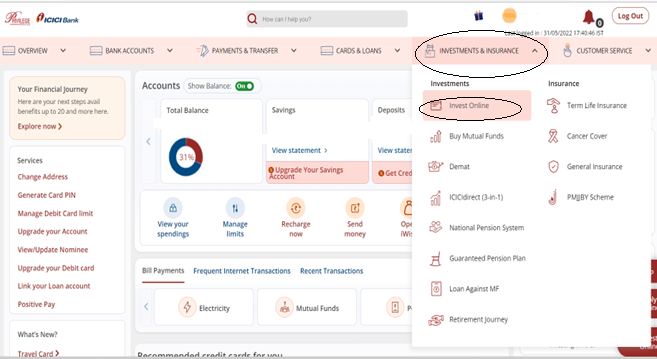

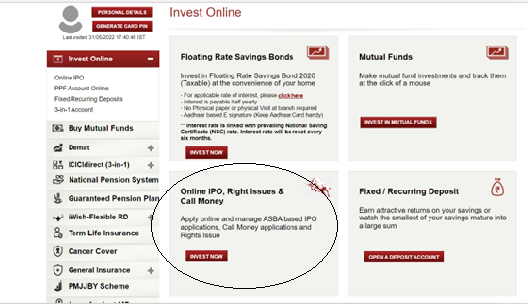

Step 2: Click on ‘Invest Online’ under the Investments & Insurance tab.

Step 3: Click on ‘Invest Now’ in the Online IPO, Right Issues & Call Money column.

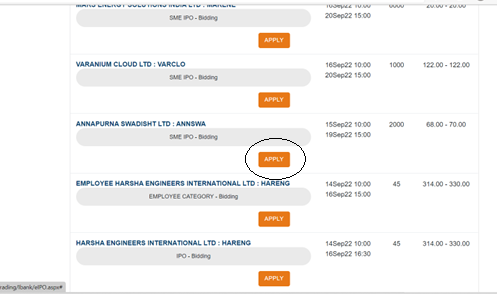

Step 4: You would get all the open IPOs for application. Click on ‘Apply’ button to choose the IPO.

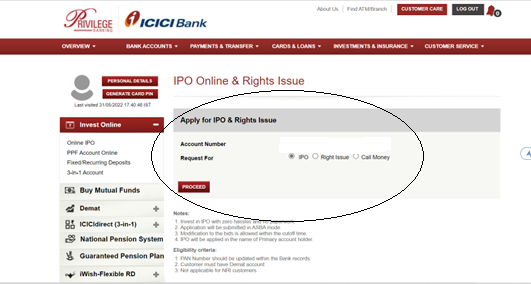

Step 5: Fill in the bank details as required and proceed for the further application.

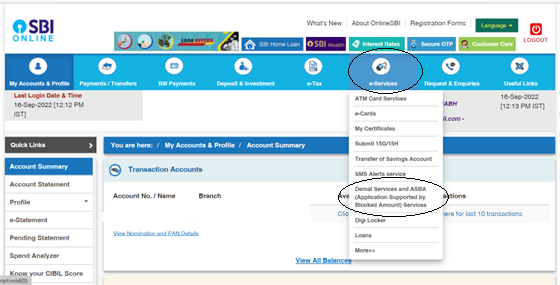

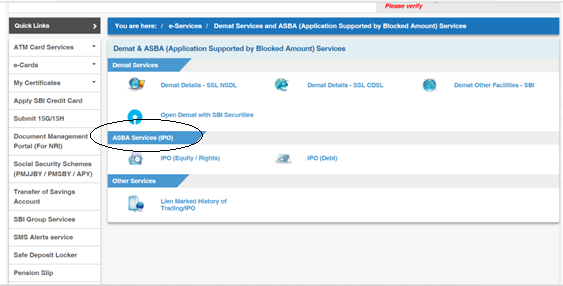

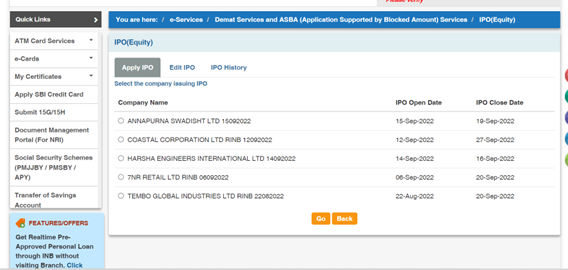

PROCESS FOR APPLYING IN AN IPO THROUGH SBI BANK

Step 1: Login to the Net Banking of SBI through the login credentials along with generating High Security Password sent on the respective mobile number. Step 2: Click on ‘Demat Services and ASBA’ tab under “e-Services”.

Step 3: Under ASBA Services, click on “IPO”.

Step 4: List of available IPOs will appear. You can select any IPO as per your choice.

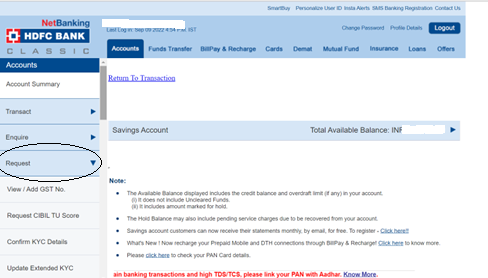

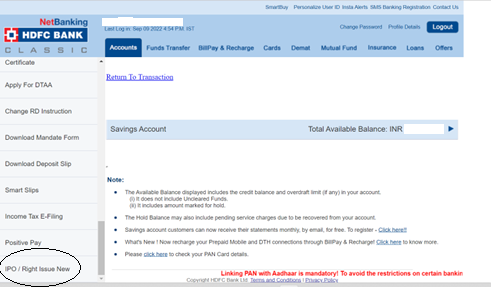

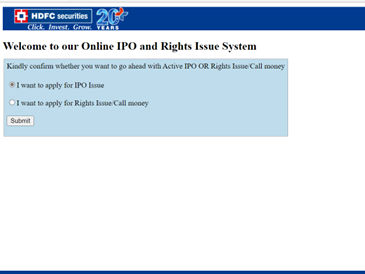

PROCESS FOR APPLYING IN AN IPO THROUGH HDFC BANK

Step 1: Login to HDFC Net Banking and click on ‘Request’ Tab on the left side.

Step 2: Select ‘IPO/Right Issue New’ under Request tab.

Step 3: Select the option for IPO Issue and choose the IPO you wish to apply for.

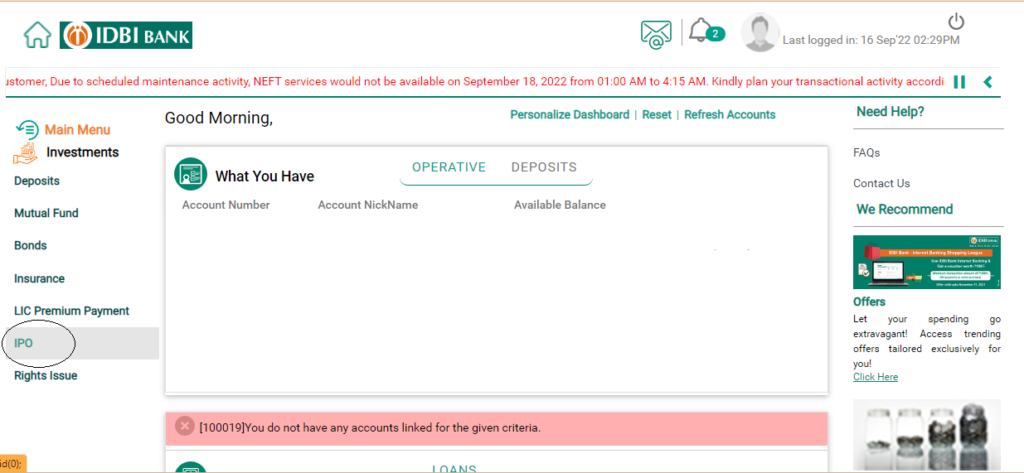

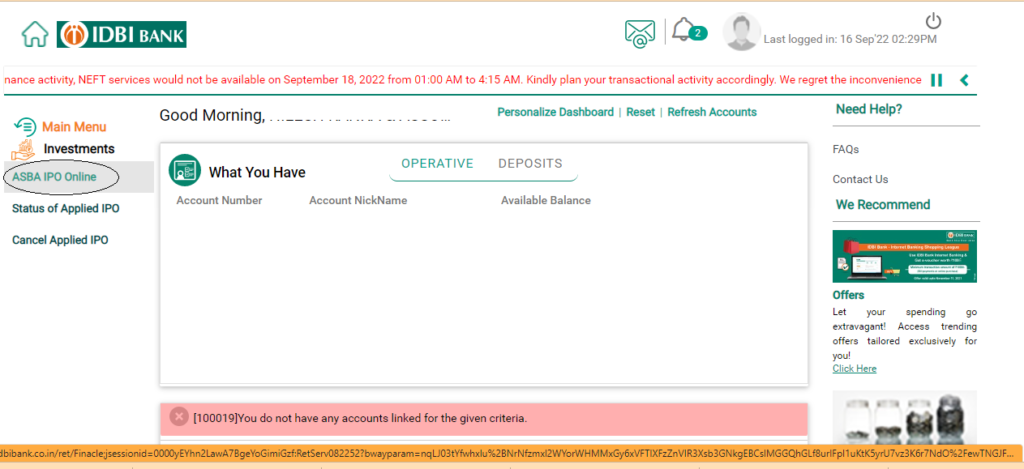

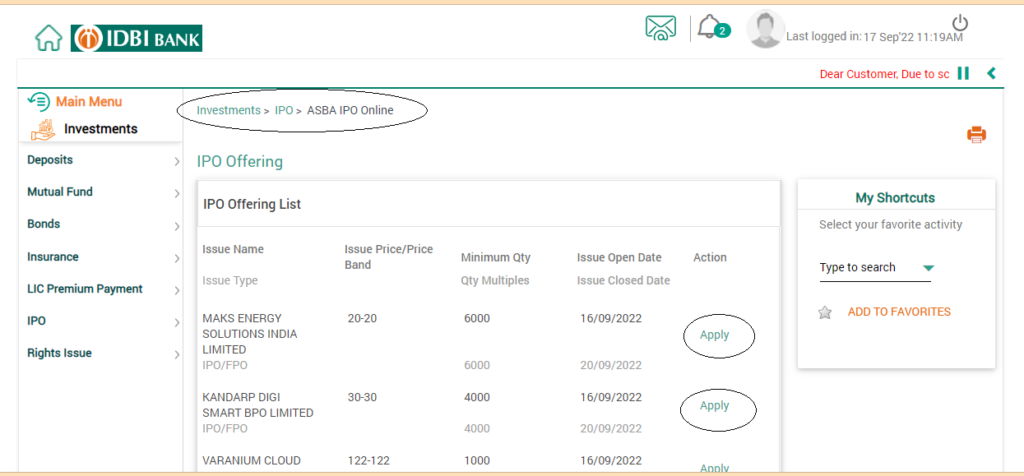

PROCESS FOR APPLYING IN AN IPO THROUGH IDBI BANK

Step 1: Login to Net Banking of IDBI Bank.

Step 2: Click on “IPO” on the left side under the Investments tab.

Step 3: Now, click on “ASBA IPO Online”.

Step 4: You will find the list of IPOs which are open on that date. Select the IPO of your choice and fill out the application providing the details of the quantity and amount that you want to invest.

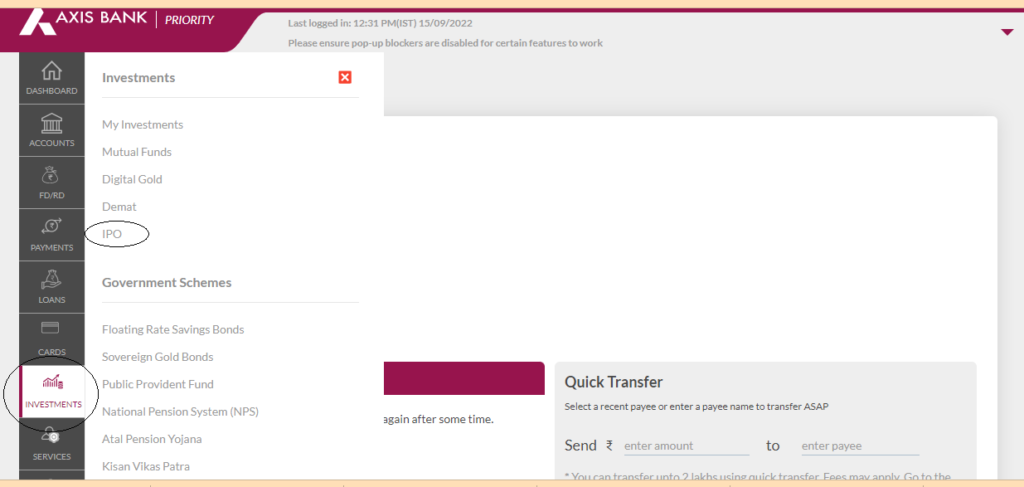

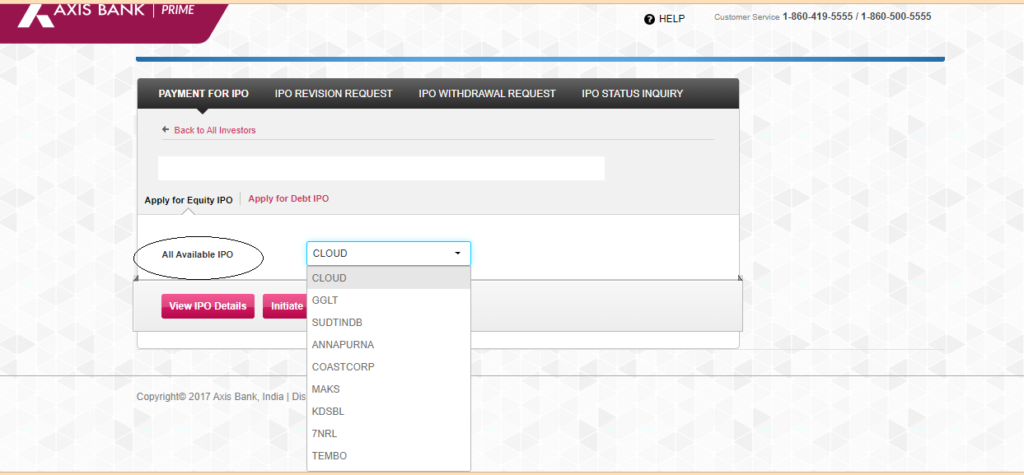

PROCESS FOR APPLYING IN AN IPO THROUGH AXIS BANK

Step 1: Login to Net Banking of Axis Bank. Go to Investments>IPO.

Step 2: Go to “Apply for Equity IPO” and you will get all the available options for the IPO. Choose any IPO according to your choice and fill the required details as requested in the application form.

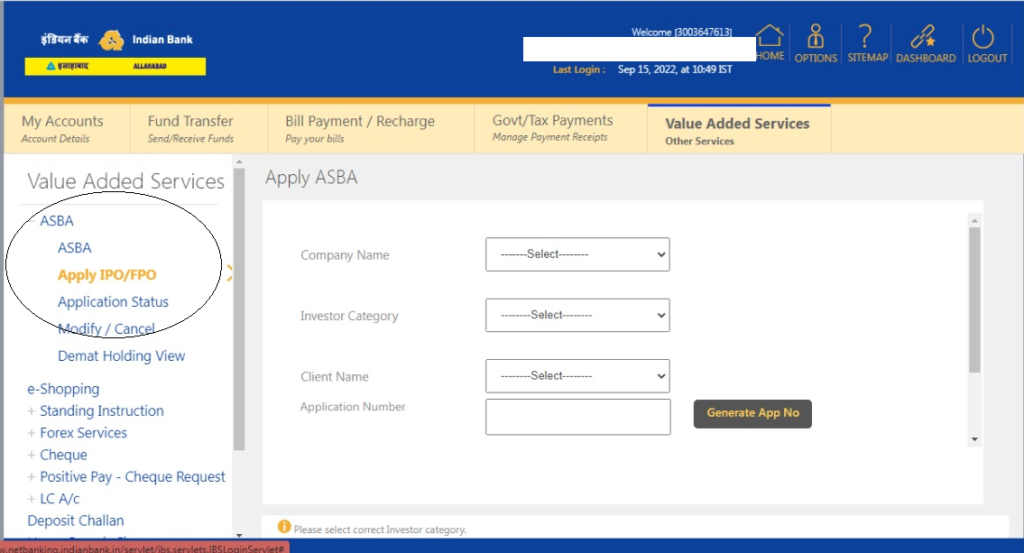

PROCESS FOR APPLYING IN AN IPO THROUGH INDIAN BANK

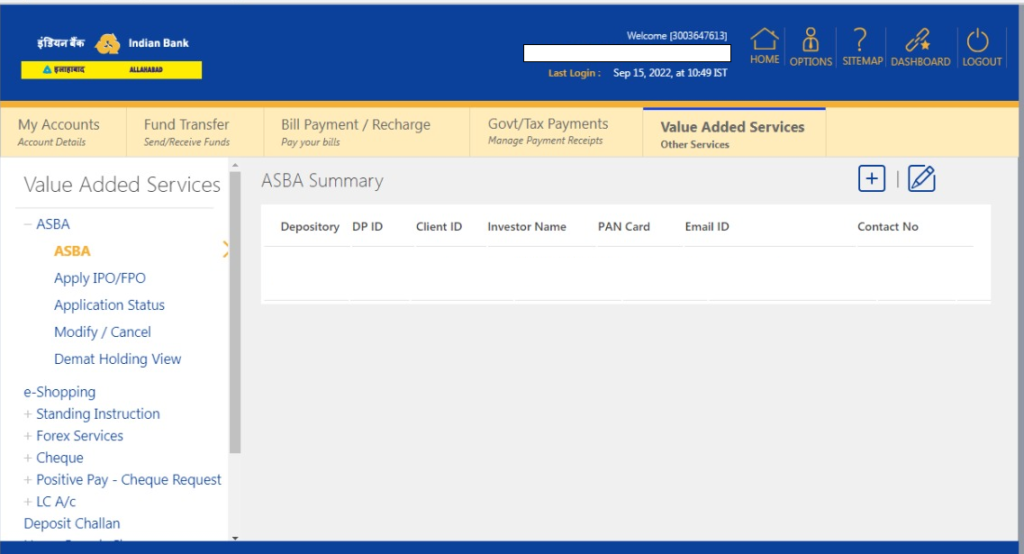

Step 1: Login to Net banking of Indian Bank. Click on ‘ASBA’ under “Value Added Services” tab.

Step 2: Click on “Apply IPO/FPO”. Fill in the details and Generate Application Number for the same.

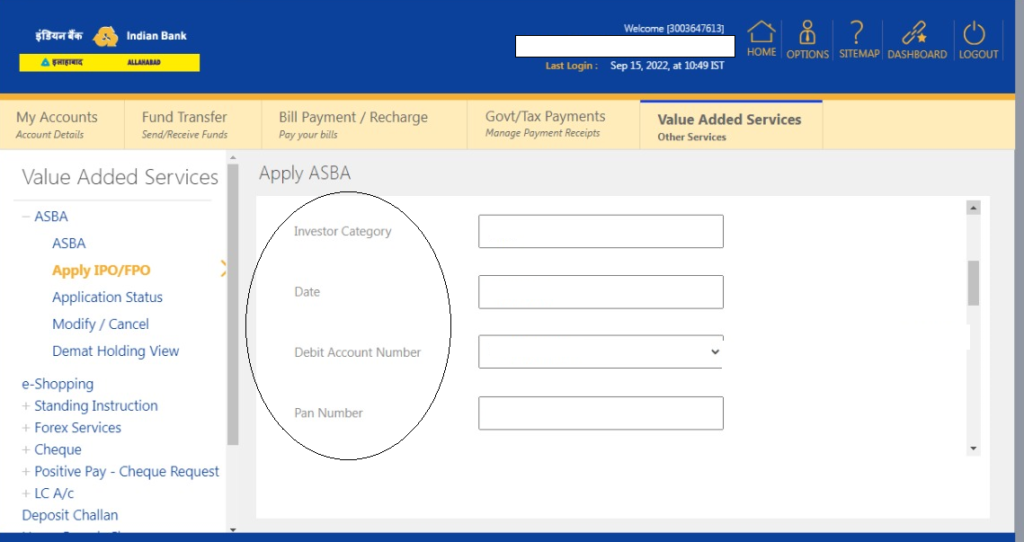

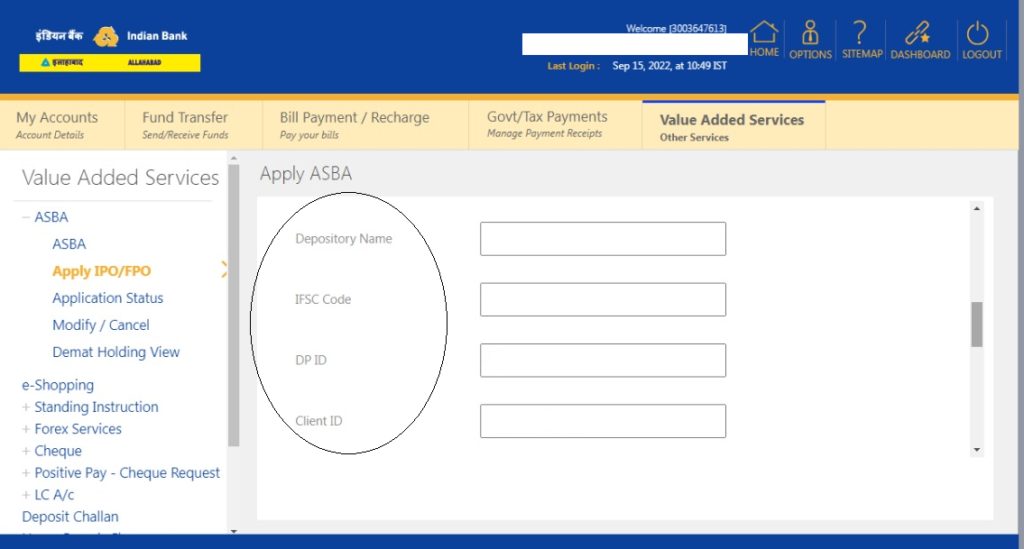

Step 3: Fill in the required details for application.

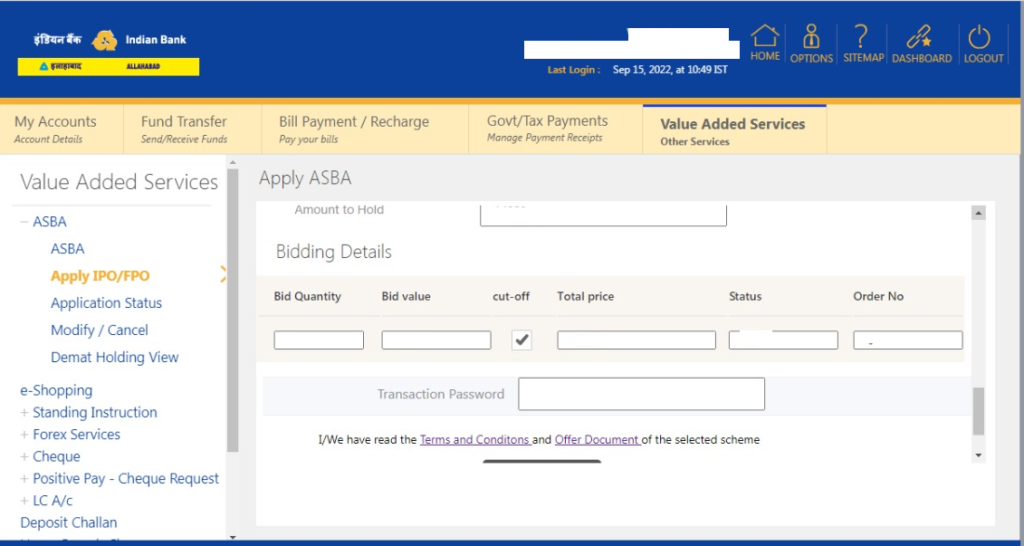

Step 4: Enter the details regarding the Quantity and Value for the Bid and complete the process by entering the Transaction Password.

Initial Public Offering (IPO) is a process by which a privately held company gets listed on the stock exchange and sells its shares to investors. There are several categories of investors in IPO application process. You can apply through more than one category to maximize the chances of allotment based on the eligibility criteria.

RETAIL INDIVIDUAL INVESTORS

This category includes Resident Indian Individuals, Non-resident Indians (NRIs) and Hindu Undivided Families (HUFs)

The minimum allocation under the retail quota is 35%.

SEBI has decreed that if the issue is oversubscribed, subject to availability, all retail investors be allotted at least one lot of shares. A lottery system is used to allocate IPO shares to the public when one lot cannot be allocated to each investor.

NON INSTITUIONAL INVESTORS (includes HNI)

Institutional Bidders (NII) category includes IPO application by High Net-worth Individual (HNI) investors. Other than HNI investors, the NII reserved portion also includes:

NRIs

HUFs

Companies

FPIs, and

Trusts.

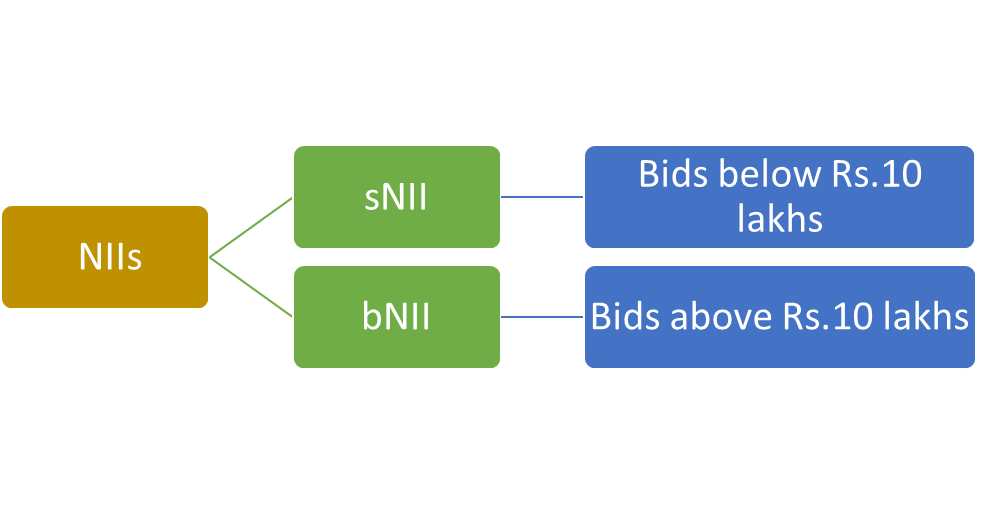

NIIs are further divided into two categories:

s-NII: NII investors who bid for shares between Rs. 2 lakhs and Rs. 10 lakhs are considered as Small NII category. The 1/3rd of NII category shares are taken for this sub-category. This subcategory is also called Small HNI (s-HNI).

b-NII: NII investors who bid for shares worth more than Rs 10 Lakhs are considered as Big NII category. The 2/3rd of NII category shares are taken for this sub-category. This subcategory is also called Big HNI (b-HNI).

HIGH NETWORTH INDIVIDUALS(HNI)

Non-Individual Investors, also known as HNIs are high-value applications and therefore are treated differently from retail applications.

HNI category allows investors to apply for more than Rs 2 lakh in an IPO.

HNI applications cannot be cancelled.

Modification of bids can be increased but cannot be reduced.

HNI investors can’t apply at the cut-off price. The applicants have to mention the exact price they are willing to pay for the IPO.

QUALIFIED INSTITUTIONAL BIDDERS (QIBs):

Commercial banks, public financial institutions, mutual fund houses and Foreign Portfolio Investors that are registered with SEBI fall in this category.

50% of the total offer price is reserved for Qualified Institutional Bidders.

Investors from this category cannot bid at the cut-off price.

QIB’s are prohibited by SEBI guidelines to withdraw their bids after the close of the IPOs.

Underwriters try to sell large sums of IPO shares to qualified investors/bankers at a thriving price before the start of the listing of IPO. To meet the targeted capital of any company, underwriters sell a huge amount of shares to QIBs. SEBI mandates that institutional investors shall sign a lock–up agreement for at least 90 days to guarantee minimal volatility during the IPO process. QIBs are particularly significant for a company launching an IPO. That’s because IPO shares are offered by the underwriters to the QIBs before the price discovery in the share market takes place. There would be lesser number of shares available to the general public if QIBs buy more shares. This would result in increased share prices. This scenario is great for a company because they want to raise as much as capital as possible.

However, SEBI has laid down rules to ensure that companies do not manipulate the IPO valuations. Because of this, SEBI doesn’t allow the companies to allocate more than 50% shares to Qualified Institutional Bidders (QIBs).

ANCHOR INVESTORS

This is a part of QIB making an application of more than Rs.10 crores in a book building issue. This category includes

Resident Indian Individuals, non-resident Indians (NRIs), HUFs, companies, trusts, science institutions, corporate bodies and societies.

Investors under this category cannot bid at the cut-off price.

Maximum 60% of the QIB category can be allocated to the Anchor Investors.

Anchor Investor Offer Price is decided separately.

No merchant banker, promoter or their relatives can apply for shares under the anchor investor category.

POINTS TO BE REMEMBERED:

UPI transaction limit for the payment of IPO has been increased from Rs.2 Lakhs to Rs.5 Lakhs for the investors with effect from 1st May, 2021.

There is a time limitation for bidding. Applications are allowed till 3:45 PM IST only. Bids placed after 3:45 PM on Day 1 and Day 2 will be pushed as AMO orders. On Day 3, bids placed after 3:45 PM will be rejected by the exchange automatically but it can vary depending upon the policies of the bank.

IPO allotment is done on a lottery or proportionate basis depending on the status of oversubscription in the segment.

KEY DIFFERENCES

PARTICULARS

RII

NII/HNI

QII

ELIGIBILITY

Resident Indian individuals and NRIs applying for shares not exceed Rs 2 Lakh in value.

Resident Indian individuals and NRIs applying for shares exceed Rs 2 Lakh in value.

Commercial banks, public financial institutions, mutual fund houses and Foreign Portfolio Investors that are registered with SEBI (More than Rs. 2 Lakhs)

SHARES AVAILABLE

35% of the Offer

15% of the Offer.

50% of the Offer.

BASIS OF ALLOTMENT

Lottery

Proportionate

Proportionate

CUT-OFF PRICE

Can invest at the cut-off price.

Cannot invest at the cut-off price.

Cannot invest at the cut-off price

BIDS

Retail investors are allowed to withdraw or lower the bids

Computing the turnover on Futures and Options is significant for the purpose of tax filing and F&O trading is mostly reported as business income while filing tax returns. Yet, one needs to analyze their total income, which can be positive or negative value (profit or loss). Expenses like office rent, telephone expenses, broker’s commission, etc. which are directly connected to F&O business should be deducted from the income. The remaining amount would be considered as the turnover from the F&O trading.

Traders are often faced with the challenge of calculating trading turnover from Derivatives and Intra-day. So, following are the formulas, using which, we can calculate the turnover:

TYPE OF TRADING

CALCULATION OF TRADING TURNOVER

TAXABLE UNDER THE HEAD

RATES

Equity Trading Intra-day

Absolute Profit/Loss [Sale price – Buy price]

Speculative Business Income

Respective Slab Rate

Futures – Equity, Commodity, Currency

Absolute Profit/Loss [Sale price – Buy price]

Non-Speculative Business Income

Respective Slab Rate

Options – Equity, Commodity, Currency

Absolute Profit/Loss* + Premium received from Sale of Options

Non-Speculative Business Income

Respective Slab Rate

Equity Delivery** Trading & Mutual Fund Trading

Total Sales Value of Shares/ Mutual Fund

Capital Gain

LTCG@10% STCG @15%

Debt Funds***

Total Sales Value of Debt Fund

Capital Gain

LTCG@20% with indexation STCG @ respective slab rate

Respective slab rates as per Equity and Debt Orientation

*Profit & Loss both here are taken as positive figures.

**In case of Equity Funds, if the holding period is less than one year, it would be treated as Short Term Capital Gain.

***In case of debt funds, if the holding period is less than 3 years, it would be treated as Short Term Capital Gain.

We should understand this with the help of some examples:

Case 1: If Saurabh purchases 500 quantity of Equity Shares @Rs.50 and sells at Rs.57 on the same day (intra-day). His turnover would be determined as:

PARTICULARS

CALCULATION

AMOUNT

Profit on Sale of Shares

500 * (57-50)

3,500

Case 2: If Saurabh purchases 500 quantity of Futures @Rs.600 and sells at Rs.620. His turnover would be determined as:

PARTICULARS

CALCULATION

AMOUNT

Profit on Sale of Futures

500 * (620-600)

10,000

Case 3: If Saurabh buy 500 quantities of Options A @Rs.80 each and sells them at Rs.77. and he also purchases 250 quantity of Options B @ Rs.60 and sells at Rs.62. His turnover would be determined as:

PARTICULARS

CALCULATION

AMOUNT

Loss on Sale of Options A

500 * (80-77)

1,500

Premium on Sale of Options A

500 * 77

38,500

Profit on Sale of Options B

250 * (62-60)

500

Premium on Sale of Options B

250 * 62

15,500

Total Turnover

56,000

Case 4: If Saurabh buy 500 quantities of Equity Share A @Rs.80 each and sells them at Rs.87 after 13 months. He also purchased 250 quantity of Equity Share B @ Rs.60 and sells at Rs.62 after 4 months. His turnover would be determined as:

PARTICULARS

CALCULATION

AMOUNT

LTCG on Sale of Equity Share A

500 * (87-80)

3,500

STCG on Sale of Equity Share B

250 * (62-60)

500

Total Capital Gain

4,000

Note: Equity Share A has been taken under Long Term Capital Gain (LTCG) since they have been held as investment for more than one year.

F&O LOSSES AND TAX AUDIT

Intra-day stock trading is taxable under the head Speculative income/loss. Speculative loss can be adjusted only against the speculative income. However, any unadjusted speculative loss can be carried forward up to 4 years. F&O trading income/loss is covered under Non-Speculative business income. Any unadjusted business loss can be carried forward for 8 assessment years.

Tax Audit u/s 44AB is applicable when the trading turnover exceeds Rs.1 crore, but if the taxpayer has opted for presumptive taxation scheme, the limit for turnover is Rs.2 crores.

CONCLUSION

F&O trading has turned into an appealing proposition because of the accessibility of numerous trading platforms. Taxpayers often get confused while filing taxes about the income generated by F&O trading, and it is vital to comprehend the process to ascertain F&O turnover for income tax purposes, and when tax audit is applicable.

A mutual fund is a professionally-managed investment scheme, made up of a pool of money collected from many investors to invest in securities like stocks, bonds, money market instruments, and other assets. Mutual funds are operated by professional money managers, who allocate the fund’s assets and attempt to produce capital gains or income for the fund’s investors. A mutual fund’s portfolio is structured and maintained to match the investment objectives stated in its prospectus.

DIFFERENT TYPES OF MUTUAL FUND SCHEMES

EQUITY SCHEMES

S.NO.

CATEGORY

SCHEME CHARACTERISTICS/MINIMUM CONDITIONS

1

Multi-Cap Fund

Invest across large-cap, mid-cap, small-cap stocks Min. equity component – 65%

2

Large Cap Fund

Predominantly invest in large-cap stocks Min. equity component – 80%

3

Large and Mid-Cap Fund

Invest in both large-cap and mid-cap stocks Min. equity component (large-cap stocks) – 35% Min. equity component (mid-cap stocks) – 35%

4

Mid Cap Fund

Predominantly invest in mid-cap stocks Min. equity component (mid-cap stocks) – 65%

5

Small Cap Fund

Predominantly invest in small-cap stocks Min. equity component (small-cap stocks) – 65%

6

Dividend Yield Fund

Predominantly invest in dividend-yielding stocks Min. equity component – 65%

7

Value Fund

The scheme should follow a value investment strategy Min. equity component – 65%

8

Contra Fund

The scheme should follow a contrarian investment strategy. Min. equity component – 65%

9

Focused Fund

Maximum 30 stocks Min. equity component – 65%AMC to mention where the scheme intends to focus, viz., (multi-cap, large-cap, mid-cap, small-cap)

10

Sectoral/Thematic Fund

AMC to clearly mention the sector/theme that the scheme shall focus on Min. equity component (for stocks belonging to that sector/theme) – 80%

11

Equity Linked Savings Schemes (ELSS)

The statutory lock-in period of 3 years Min. equity component – 80% (per Equity Linked Saving Scheme, 2005, as notified by the Ministry of Finance)

Note: Mutual Funds will be permitted to offer either Value fund or Contra fund

DEBT SCHEMES

S.NO.

CATEGORY

SCHEME CHARACTERISTICS/MINIMUM CONDITIONS

1

Overnight Fund

Invest in overnight securities – Maturity of 1 day

2

Liquid Fund

Invest in debt and money market instruments – Maturity of up to 91 days

3

Ultra-short Duration Fund

Invest in Debt & Money Market instruments – Macaulay duration of the portfolio to be between 3 – 6 months

4

Low Duration Fund

Invest in Debt & Money Market instruments – Macaulay duration of the portfolio to be between 6 – 12 months

5

Money Market Fund

Invest in Money Market instruments – Maturity up to 1 year

6

Short Duration Fund

Invest in Debt & Money Market instruments – Macaulay duration of the portfolio to be between 1-3 years

7

Medium Duration Fund

Invest in Debt & Money Market instruments – Macaulay duration of the portfolio to be between 3 – 4 years

8

Medium to Long Duration Fund

Invest in Debt & Money Market instruments – Macaulay duration of the portfolio to be between 4-7 years

9

Long Duration Fund

Invest in Debt & Money Market instruments – Macaulay duration of the portfolio to be more than 7 years

10

Dynamic Bond

Investment across duration

11

Corporate Bond Fund

Minimum 80% investment in corporate bonds (only in highest rated instruments

12

Credit Risk Fund

Minimum 65% investment in corporate bonds (below highest rated instruments)

13

Banking and PSU Fund

Minimum 80% investment in Debt instruments of banks, Public Sector Undertakings, Public Financial Institutions

14

Gilt Fund

Minimum 80% investment in Government Securities (across maturity)

15

Gilt Fund with 10-year constant duration

Minimum 80% investment in Government Securities (so that the Macaulay duration of the portfolio is equal to 10 years)

HYBRID SCHEMES

S.NO.

CATEGORY

SCHEME CHARACTERISTICS/MINIMUM CONDITIONS

1

Conservative Hybrid Fund

Minimum equity component – Between 10% and 25% Minimum debt component – Between 75% and 90%

2

Balanced Hybrid Fund

Minimum equity component – Between 40% and 60% Minimum debt component – Between 40% and 60% The AMC cannot do any arbitrage in this scheme

3

Aggressive Hybrid Fund

Minimum equity component – Between 65% and 80% Minimum debt component – Between 20% and 35%

4

Dynamic Asset Allocation (or Balanced Advantage)

Invest in equity or debt – AMC to manage it dynamically

5

Multi-Asset Allocation

Invests in at least three asset classes with a minimum allocation of at least 10% each in all three asset classes Note: AMC cannot offer foreign securities as a foreign asset class

6

Arbitrage Fund

The scheme should follow an arbitrage strategy. Minimum equity component – 65%

7

Equity Savings

Minimum equity component – 65% Minimum debt component – 10% AMC to state minimum hedged & unhedged in the Scheme Information Document (SID) AMC to state Asset Allocation under defensive considerations in the Offer Document

Note: Mutual Funds can offer either an Aggressive Hybrid fund or Balanced fund.

SOLUTION ORIENTED SCHEMES

S.NO.

CATEGORY

SCHEME CHARACTERISTICS/MINIMUM CONDITIONS

1

Retirement Fund

Lock-in: At least 5 years or till retirement age, whichever is earlier

2

Children’s Fund

Lock-in: At least 5 years or till the child attains the age of majority, whichever is earlier

OTHER SCHEMES

S.NO.

CATEGORY

SCHEME CHARACTERISTICS/MINIMUM CONDITIONS

1

Index Funds/ Exchange Traded Funds

Minimum 95% investment in securities of a particular index (which is being replicated/ tracked) AMC to mention the name of the index

2

Fund of Funds (Overseas/ Domestic)

Minimum 95% investment in the underlying fund AMC to mention the name of the underlying fund

KEY MUTUAL FUND RATIO

1. Standard Deviation:

Standard Deviation value gives an idea about how volatile fund returns has been in the past 3 years. Lower value indicates more predictable performance.

So, if you are comparing 2 funds (let’s say Fund A and Fund B) in the same category. If Fund A and Fund B has given 9% returns in last 3 years, but Fund A standard deviation value is lower than Fund B. So, you can say that there is a higher chance that Fund A will continue giving similar returns in future also whereas Fund B returns may vary.

2. Beta

Beta value gives idea about how volatile fund performance has been compared to similar funds in the market. Lower beta implies the fund gives more predictable performance compared to similar funds in the market.

So, if you are comparing 2 funds (let’s say Fund A and Fund B) in the same category. If Fund A and Fund B has given 9% returns in last 3 years, but Fund A beta value is lower than Fund B. So, you can say that there is a higher chance that Fund A will continue giving similar returns in future also whereas Fund B returns may vary.

3. Sharpe Ratio

Sharpe ratio indicates how much risk was taken to generate the returns. Higher the value means, fund has been able to give better returns for the amount of risk taken. It is calculated by subtracting the risk-free return, defined as an Indian Government Bond, from the fund’s returns, and then dividing by the standard deviation of returns.

For example, if fund A and fund B both have 3-year returns of 15%, and fund A has a Sharpe ratio of 1.40 and fund B has a Sharpe ratio of 1.25, you can choose fund A, as it has given higher risk-adjusted return.

4. Treynor’s Ratio

Treynor’s ratio indicates how much excess return was generated for each unit of risk taken. Higher the value means, fund has been able to give better returns for the amount of risk taken. It is calculated by subtracting the risk-free return, defined as an Indian Government Bond, from the fund’s returns, and then dividing by the beta of returns.

For example, if fund A and fund B both have 3-year returns of 15%, and fund A has a Treynor’s ratio of 1.40 and fund B has a Treynor’s ratio of 1.25, then you can choose fund A, as it has given higher risk-adjusted return.

5. Jension’s Alpha

Alpha indicates how fund generated additional returns compared to a benchmark.

Let’s say if a fund A benchmarks its returns with Nifty50 returns then alpha equal to 1.0 indicates the fund has beaten the nifty returns by 1%, so the higher the alpha, the better.

6. Sortino Ratio

The Sortino ratio is a variation of the Sharpe ratio that differentiates harmful volatility from total overall volatility by using the asset’s standard deviation of negative portfolio returns—downside deviation—instead of the total standard deviation of portfolio returns. The Sortino ratio takes an asset or portfolio’s return and subtracts the risk-free rate, and then divides that amount by the asset’s downside deviation.

Just like the Sharpe ratio, a higher Sortino ratio result is better. When looking at two similar investments, a rational investor would prefer the one with the higher Sortino ratio because it means that the investment is earning more return per unit of the bad risk that it takes on.

For example, assume Mutual Fund X has an annualized return of 12% and a downside deviation of 10%. Mutual Fund Z has an annualized return of 10% and a downside deviation of 7%. The risk-free rate is 2.5%. The Sortino ratios for both funds would be calculated as:

Mutual Fund X Sortino = (12%−2.5%)/10% = 0.95

Mutual Fund Z Sortino = (10%−2.5%)/7% = 1.07

Even though Mutual Fund X is returning 2% more on an annualized basis, it is not earning that return as efficiently as Mutual Fund Z, given their downside deviations. Based on this metric, Mutual Fund Z is the better investment choice.

Sovereign Gold Bonds (SGBs) are the alternative to investment in physical gold. These bonds are risk-free as issued by the Government of India. The Government launched this scheme in 2015 under Gold Monetisation Scheme. These bonds are backed with policies and procedures notified by RBI.

Features:

A Person resident in India having PAN can apply for this scheme. Even a resident person subsequently changes the status to non-resident also continues to hold SGB till early redemption/maturity.

The Bonds are issued in one gram of gold denominations and in multiples thereof. The Minimum investment shall be 1 gram per fiscal year. The Maximum investment is 4 kg for Individual/HUF and 20 kg for others per fiscal year.

Bonds having a tenor of 8 years but early redemption allowed after 5 years of lock- in period.

Once bond purchased the certificate of holding will be issued by the RBI. The said holding is credited in the Demat account and can be traded in stock exchanges.

At the time of redemption price will be decided based on the simple average of the closing price of gold purity 999 of the previous 3 working days published by the India Bullion and Jewelers Association Limited.

Advantage to Invest in SGB:

Every investor is compensated with fixed Interest at the rate of 2.50 percent payable semiannually directly in the bank account of the investor.

Bonds are exchange traded fund.

Bonds are transferable to relatives/friends/others in accordance with the provisions of the Government Securities Act 2006.

The capital gains tax arising on redemption on the maturity of SGB to “an individual” has been exempted. The indexation benefits will be provided to long terms capital gains arising on the transfer of bonds.

Joint holding is allowed.

A minor also can invest.

Nomination facility is available for the investor.

Investment in SGB is risk-free. All the risk and cost of storage with holding physical gold are eliminated.

No TDS will deduct. It’s the responsibility of bond holders to comply with tax laws.

Partial redemption is allowed in multiples of 1 gram.