Buyback of Shares is also known as Share Repurchase. The name itself suggests that buyback refers to the buying back of shares by the company from the shareholders in the open market at a premium. The repurchased shares are cancelled by the company and hence, reduce the outstanding shares in the market. Tax on Buyback of shares is now regulated by Section 115QA of the Income Tax Act,1961.

WHY DO COMPANIES BUYBACK SHARES?

Correction of Share Price: Buyback of Shares generally results in increase in the market price. So, if the market price of the shares is highly undervalued, the company can correct it by buying back of shares.

Promoter’s Shareholding: One of the main reasons behind buyback of shares is to increase the shareholding of the promoters by purchasing from the open market.

Attractive Financials: With the reduced number of shares from buyback, Earnings per share of the company would increase. It also helps in improving the key financial ratios.

Utilization of Excess Cash: By buyback of shares, company can use their excess cash balance by paying premium to the shareholders over and above the market price.

INCOME TAX ON BUYBACK ON SHARES AS PER SECTION 115QA

Initially, Section 115QA was applicable only to Unlisted companies but in the Union Budget 2019, it was announced that this section is now applicable to Listed companies also. The effect of this was applicable from 1st July, 2019.

As per Section115QA, all the companies (both listed and unlisted) have to pay tax at the rate of 20% (plus Surcharge @ 12% and HEC @4%).

Companies have to pay tax on the amount of distributed income on the buyback of shares.

The tax shall be paid within 14 days from the date of payment to the shareholders.

The amount of tax paid is not available for any credit.

Every company shall pay tax on the distributed income in case of buyback of shares even if that company is not liable to pay income tax.

As per Section 115QA read along with Section 10(34A), shareholders are exempt from any kind of tax on buyback of shares. It would have been considered as double taxation if both shareholders and companies have to pay tax on buyback of shares. Therefore, only companies are liable to pay tax on buyback of shares.

TAX LIABILITY

BEFORE AMENDMENT

POST AMENDMENT (2019)

COMPANY (Both Listed and Unlisted)

No Tax Liability

The company is now liable for a buyback tax of 20% on the Distributed Income*

INDIVIDUAL SHAREHOLDER

Individual shareholders must pay Capital Gains Tax (Long term or Short term) depending on the holding period of shares

No Tax Liability

*Rule 40BB of Income Tax Act 1962 contains the procedure for the calculation of Distributed Income in different cases.

Limited Liability Partnership (LLP) is a combination of a corporate structure along with the flexibility of a partnership. LLP is governed by Limited Liability Partnership Act, 2008. Nowadays, LLP has become very popular of business as many entrepreneurs are willing to opt for it. An LLP is a separate legal entity and the liability of its partners are limited to the agreed upon contribution in the LLP. An LLP can enter into contracts and hold property in its own name. Just like partnership deed, LLP is also operated on the basis of the LLP Agreement. Limited liability partnerships are taxed at the rate of 30%.

ADVANTAGES

Limited Liability (from the partner’s point of view): Partners in an LLP have limited liability which implies that the partners are liable only to the extent of their contribution. Partners are not responsible for any misconduct by other partners, and they are not liable to pay off the debts of the LLP from their personal assets.

Flexibility: Since LLP is operated by LLP Agreement, it has greater flexibility in the management of the business in comparison to a company.

Separate Legal Entity: LLP is a separate legal entity from its members. It can hold property, and buy assets in its own name.

Corporate Ownership: LLPs have corporate ownership without having to comply with all the compliances as in a company. It means that LLPs can appoint two companies as their members, rather than having to appoint at least one director as in the case of a company.

Perpetual Succession: Perpetual succession in an LLP means that it is not affected by the death, insolvency, retirement or any other change of the partners.

Easy Formation: As compared to a company, forming an LLP is less complicated and less time consuming. It has fewer legal compliances.

Capital Requirement: There is no minimum cap as for the requirement of capital. LLP can be formed with any amount of capital.

Audit: Audit of an LLP is not mandatory. Although, if the turnover of an LLP exceeds the certain prescribed limit, then LLP shall require to get the tax audit.

DISADVANTAGES

Taxation: In an LLP, the rate of taxation is flat 30% irrespective of the turnover, while a company is taxable at the rate of 25% if the turnover is upto Rs.250 crores.

Limited Liability (from point of view of LLP): Partners are the real owners of the LLP. They can operate in their own ways. And since the liability of the partners are limited, LLP would have to suffer any loss even if the fault is of the partner/member.

Public Disclosure: Financial Accounts have to be represented as public records. Personal income of the members also has to be disclosed.

Capital Requirements: LLPs does not have the concept of equity investments. Investors cannot fund an LLP without becoming a member. So, it would be difficult for an LLP to fulfil the capital requirements.

TRADITIONAL PARTNERSHIP V/S LLP

PARTICULARS

TRADITIONAL PARTNERSHIP

LLP

Registration under Act

Indian Partnership Act, 1932

Limited Liability Partnership Act, 2008

Minimum no. of Partners

2 Partners

2 Partners

Maximum no. of Partners

Maximum 20 Partners

No Limit

Liability of Partners

Jointly Liable

To the extent of their contribution

Registration

Not Compulsory

Compulsory

Tax Audit

Required when Turnover/Gross Receipts exceeds Rs.1 crore – Business Rs. 50 Lakhs – Profession

Required only if Turnover > Rs.40 Lakhs; or Contribution > Rs.25 Lakhs

COMPANY V/S LLP

PARTICULARS

COMPANY

LLP

Registration under Act

Companies Act,2013

Limited Liability Partnership Act,2008

Designated Directors/Partners

Minimum – 2 Maximum – 15

Minimum – 2 No Maximum Limit

Minimum no. of members

2

2

Maximum no. of members

200

No Limit

Abiding by

MOA/AOA of the company

LLP Agreement

Tax Audit

Compulsory

Required only if Turnover > Rs.40 Lakhs; or Contribution > Rs.25 Lakhs

E-Invoicing is a system for authentication of B2B invoices electronically by the GSTN. Under the electronic invoicing framework, a unique Invoice Reference Number (IRN) is issued against each invoice digitally using Invoice Registration Portal (IRP) managed the GSTN. Maximum 100 items can be incorporated in a single invoice.

E-Invoicing eliminates the need to enter data manually in different portals, i.e., we are not required to enter the same data again and again into GST Portal, E-Way Bill Portal and in the E-Invoice Portal.

E-Invoicing also helps to track the invoices in real-time. It helps in resolving a large gap in data reconciliation under GST to reduce the mismatch of errors. It provides a framework to quickly access the complete invoice related details.

APPLICABILITY

An assessee shall comply with the provisions of e-invoicing if their aggregate turnover exceeds the specified limit in any financial year after the implementation of GST, i.e., 2017-18 onwards. The calculation of aggregate turnover shall include the turnover of all the GSTINs issued under a single PAN across India.

PHASE

APPLICABLE IF

APPLICABILITY DATE

I

TURNOVER > 500 CRORES

01.10.2020

II

TURNOVER > 100 CRORES

01.01.2021

III

TURNOVER > 50 CRORES

01.04.2021

IV

TURNOVER > 20 CRORES

01.04.2022

Example: Suppose PQR Ltd had aggregate turnover as follows:

YEAR

TURNOVER

FY 2017-18

Rs.12 crore

FY 2018-19

Rs.16 crore

FY 2019-20

Rs.23 crore

FY 2020-21

Rs.18 crore

FY 2021-22

Rs.14 crore

PQR Ltd shall mandatorily generate e-invoices from 01.04.2022 irrespective of the current year’s aggregate turnover as it has crossed the threshold limit of Rs.20 crore turnover limit in FY 2019-20.

Following class of taxpayers are currently covered under e-invoicing:

Supplies to the registered persons (B2B)

Supplies to SEZs

Exports

Deemed exports

WHO DOESN’T REQUIRE E-INVOICING?

Following category of a person exempted under e-invoice

A banking company

A non-banking financial company

A financial institution

An insurer

A person engaged in supplying passenger transportation service

A goods transport agency (GTA) supplying services

A person engaged in supplying services in terms of admission of the exhibition of cinematograph films in the multiplex screen

Persons registered in terms of Rule 14 of CGST Rules (OIDAR)

Special Economic Zone units (although e-invoicing is required for SEZ Developers)

Computing the turnover on Futures and Options is significant for the purpose of tax filing and F&O trading is mostly reported as business income while filing tax returns. Yet, one needs to analyze their total income, which can be positive or negative value (profit or loss). Expenses like office rent, telephone expenses, broker’s commission, etc. which are directly connected to F&O business should be deducted from the income. The remaining amount would be considered as the turnover from the F&O trading.

Traders are often faced with the challenge of calculating trading turnover from Derivatives and Intra-day. So, following are the formulas, using which, we can calculate the turnover:

TYPE OF TRADING

CALCULATION OF TRADING TURNOVER

TAXABLE UNDER THE HEAD

RATES

Equity Trading Intra-day

Absolute Profit/Loss [Sale price – Buy price]

Speculative Business Income

Respective Slab Rate

Futures – Equity, Commodity, Currency

Absolute Profit/Loss [Sale price – Buy price]

Non-Speculative Business Income

Respective Slab Rate

Options – Equity, Commodity, Currency

Absolute Profit/Loss* + Premium received from Sale of Options

Non-Speculative Business Income

Respective Slab Rate

Equity Delivery** Trading & Mutual Fund Trading

Total Sales Value of Shares/ Mutual Fund

Capital Gain

LTCG@10% STCG @15%

Debt Funds***

Total Sales Value of Debt Fund

Capital Gain

LTCG@20% with indexation STCG @ respective slab rate

Respective slab rates as per Equity and Debt Orientation

*Profit & Loss both here are taken as positive figures.

**In case of Equity Funds, if the holding period is less than one year, it would be treated as Short Term Capital Gain.

***In case of debt funds, if the holding period is less than 3 years, it would be treated as Short Term Capital Gain.

We should understand this with the help of some examples:

Case 1: If Saurabh purchases 500 quantity of Equity Shares @Rs.50 and sells at Rs.57 on the same day (intra-day). His turnover would be determined as:

PARTICULARS

CALCULATION

AMOUNT

Profit on Sale of Shares

500 * (57-50)

3,500

Case 2: If Saurabh purchases 500 quantity of Futures @Rs.600 and sells at Rs.620. His turnover would be determined as:

PARTICULARS

CALCULATION

AMOUNT

Profit on Sale of Futures

500 * (620-600)

10,000

Case 3: If Saurabh buy 500 quantities of Options A @Rs.80 each and sells them at Rs.77. and he also purchases 250 quantity of Options B @ Rs.60 and sells at Rs.62. His turnover would be determined as:

PARTICULARS

CALCULATION

AMOUNT

Loss on Sale of Options A

500 * (80-77)

1,500

Premium on Sale of Options A

500 * 77

38,500

Profit on Sale of Options B

250 * (62-60)

500

Premium on Sale of Options B

250 * 62

15,500

Total Turnover

56,000

Case 4: If Saurabh buy 500 quantities of Equity Share A @Rs.80 each and sells them at Rs.87 after 13 months. He also purchased 250 quantity of Equity Share B @ Rs.60 and sells at Rs.62 after 4 months. His turnover would be determined as:

PARTICULARS

CALCULATION

AMOUNT

LTCG on Sale of Equity Share A

500 * (87-80)

3,500

STCG on Sale of Equity Share B

250 * (62-60)

500

Total Capital Gain

4,000

Note: Equity Share A has been taken under Long Term Capital Gain (LTCG) since they have been held as investment for more than one year.

F&O LOSSES AND TAX AUDIT

Intra-day stock trading is taxable under the head Speculative income/loss. Speculative loss can be adjusted only against the speculative income. However, any unadjusted speculative loss can be carried forward up to 4 years. F&O trading income/loss is covered under Non-Speculative business income. Any unadjusted business loss can be carried forward for 8 assessment years.

Tax Audit u/s 44AB is applicable when the trading turnover exceeds Rs.1 crore, but if the taxpayer has opted for presumptive taxation scheme, the limit for turnover is Rs.2 crores.

CONCLUSION

F&O trading has turned into an appealing proposition because of the accessibility of numerous trading platforms. Taxpayers often get confused while filing taxes about the income generated by F&O trading, and it is vital to comprehend the process to ascertain F&O turnover for income tax purposes, and when tax audit is applicable.

Section 40(B) of Income Tax Act provides the maximum permissible amount payable to a partner in a partnership firm. The returns of a partner can be in the form of

Interest on Capital: Interest payable to partners shall be in accordance with the terms of the partnership deed, however, it shall not exceed 12% per annum.

Share of Profit

Remuneration: Remuneration payable to partners shall be in accordance with the terms of the partnership deed

ESTIMATION OF INCOME OF PARTNER IN A FIRM

The partner’s share in the total income of firm is exempt in the hands of the partner and hence would not be included in his total income. And due to this exemption, he cannot set-off his share of profits a firm’s losses.

INTEREST PAYABLE TO PARTNERS

There are few conditions which shall be fulfilled in order to be eligible for interest payable under section 40(B):

The interest payable by a firm to its partners should be authorized by and in accordance with the partnership deed.

The interest payable by a firm to its partners should not be for a period falling prior to the date of such partnership deed authorizing the payment of such interest.

Interest payable to partners has a maximum cap of 12% per annum. Firm cannot pay any more than the prescribed limit.

Note: Interest here means simple interest and not compounding interest.

CONDITIONS FOR DEDUCTION UNDER REMUNERATION:

Remuneration to partners includes salary, bonus, commission, etc. Following conditions need to be satisfied for claiming the deduction:

Remuneration shall be allowed only to working partners. Working Partner is a partner who actively engages in conducting the business affairs of the firm.

Remuneration must be authorized by partnership deed and according to the terms of partnership deed. Clear directions must be specified in the partnership deed.

Remuneration paid to the working partners will be allowed as deduction but it should belong to the period as specified in the partnership deed. It should be related to the period of the partnership deed.

It is not allowed if tax is paid on presumptive basis under section 44AD or section 44ADA.

Remuneration payable shall be within the maximum permissible limits (as mentioned below). This limit is for total salary to all partners and not for any single partner.

CALCULATION OF BOOK PROFIT FOR PARTNER’S REMUNERATION U/S 40(B)

Book profit means the net profit as shown in the profit and loss account which is computed according to the manner laid down in the chapter IV-D. Book profit is calculated after some adjustments which are mentioned below:

Net profit as per profit and loss account

Add remuneration/salary/bonus/commission if already debited

Add Brought forward business loss, deduction under section 80C to 80U if debited to profit and loss a/c

Deduct interest if it is not deducted

Make adjustments for expenses as per section 28 to 44D.

AMOUNT OF DEDUCTION:

BOOK PROFIT (Rs.)

MAXIMUM DEDUCTIBLE AMOUNT (Rs.)

Loss

1,50,000

Profit upto Rs.3,00,000

90% of book Profit or Rs.1,50,000; whichever is more

More than Rs.3,00,000

60% of the Book profit

TAXABILITY IN THE HANDS OF PARTNERS:

Remuneration is taxable in hands of partners as Business Income. Note that remuneration to partners is distant from the share of profits payable to partner since share of profits is exempt, but remuneration is taxable in the income of partners.

A mutual fund is a professionally-managed investment scheme, made up of a pool of money collected from many investors to invest in securities like stocks, bonds, money market instruments, and other assets. Mutual funds are operated by professional money managers, who allocate the fund’s assets and attempt to produce capital gains or income for the fund’s investors. A mutual fund’s portfolio is structured and maintained to match the investment objectives stated in its prospectus.

DIFFERENT TYPES OF MUTUAL FUND SCHEMES

EQUITY SCHEMES

S.NO.

CATEGORY

SCHEME CHARACTERISTICS/MINIMUM CONDITIONS

1

Multi-Cap Fund

Invest across large-cap, mid-cap, small-cap stocks Min. equity component – 65%

2

Large Cap Fund

Predominantly invest in large-cap stocks Min. equity component – 80%

3

Large and Mid-Cap Fund

Invest in both large-cap and mid-cap stocks Min. equity component (large-cap stocks) – 35% Min. equity component (mid-cap stocks) – 35%

4

Mid Cap Fund

Predominantly invest in mid-cap stocks Min. equity component (mid-cap stocks) – 65%

5

Small Cap Fund

Predominantly invest in small-cap stocks Min. equity component (small-cap stocks) – 65%

6

Dividend Yield Fund

Predominantly invest in dividend-yielding stocks Min. equity component – 65%

7

Value Fund

The scheme should follow a value investment strategy Min. equity component – 65%

8

Contra Fund

The scheme should follow a contrarian investment strategy. Min. equity component – 65%

9

Focused Fund

Maximum 30 stocks Min. equity component – 65%AMC to mention where the scheme intends to focus, viz., (multi-cap, large-cap, mid-cap, small-cap)

10

Sectoral/Thematic Fund

AMC to clearly mention the sector/theme that the scheme shall focus on Min. equity component (for stocks belonging to that sector/theme) – 80%

11

Equity Linked Savings Schemes (ELSS)

The statutory lock-in period of 3 years Min. equity component – 80% (per Equity Linked Saving Scheme, 2005, as notified by the Ministry of Finance)

Note: Mutual Funds will be permitted to offer either Value fund or Contra fund

DEBT SCHEMES

S.NO.

CATEGORY

SCHEME CHARACTERISTICS/MINIMUM CONDITIONS

1

Overnight Fund

Invest in overnight securities – Maturity of 1 day

2

Liquid Fund

Invest in debt and money market instruments – Maturity of up to 91 days

3

Ultra-short Duration Fund

Invest in Debt & Money Market instruments – Macaulay duration of the portfolio to be between 3 – 6 months

4

Low Duration Fund

Invest in Debt & Money Market instruments – Macaulay duration of the portfolio to be between 6 – 12 months

5

Money Market Fund

Invest in Money Market instruments – Maturity up to 1 year

6

Short Duration Fund

Invest in Debt & Money Market instruments – Macaulay duration of the portfolio to be between 1-3 years

7

Medium Duration Fund

Invest in Debt & Money Market instruments – Macaulay duration of the portfolio to be between 3 – 4 years

8

Medium to Long Duration Fund

Invest in Debt & Money Market instruments – Macaulay duration of the portfolio to be between 4-7 years

9

Long Duration Fund

Invest in Debt & Money Market instruments – Macaulay duration of the portfolio to be more than 7 years

10

Dynamic Bond

Investment across duration

11

Corporate Bond Fund

Minimum 80% investment in corporate bonds (only in highest rated instruments

12

Credit Risk Fund

Minimum 65% investment in corporate bonds (below highest rated instruments)

13

Banking and PSU Fund

Minimum 80% investment in Debt instruments of banks, Public Sector Undertakings, Public Financial Institutions

14

Gilt Fund

Minimum 80% investment in Government Securities (across maturity)

15

Gilt Fund with 10-year constant duration

Minimum 80% investment in Government Securities (so that the Macaulay duration of the portfolio is equal to 10 years)

HYBRID SCHEMES

S.NO.

CATEGORY

SCHEME CHARACTERISTICS/MINIMUM CONDITIONS

1

Conservative Hybrid Fund

Minimum equity component – Between 10% and 25% Minimum debt component – Between 75% and 90%

2

Balanced Hybrid Fund

Minimum equity component – Between 40% and 60% Minimum debt component – Between 40% and 60% The AMC cannot do any arbitrage in this scheme

3

Aggressive Hybrid Fund

Minimum equity component – Between 65% and 80% Minimum debt component – Between 20% and 35%

4

Dynamic Asset Allocation (or Balanced Advantage)

Invest in equity or debt – AMC to manage it dynamically

5

Multi-Asset Allocation

Invests in at least three asset classes with a minimum allocation of at least 10% each in all three asset classes Note: AMC cannot offer foreign securities as a foreign asset class

6

Arbitrage Fund

The scheme should follow an arbitrage strategy. Minimum equity component – 65%

7

Equity Savings

Minimum equity component – 65% Minimum debt component – 10% AMC to state minimum hedged & unhedged in the Scheme Information Document (SID) AMC to state Asset Allocation under defensive considerations in the Offer Document

Note: Mutual Funds can offer either an Aggressive Hybrid fund or Balanced fund.

SOLUTION ORIENTED SCHEMES

S.NO.

CATEGORY

SCHEME CHARACTERISTICS/MINIMUM CONDITIONS

1

Retirement Fund

Lock-in: At least 5 years or till retirement age, whichever is earlier

2

Children’s Fund

Lock-in: At least 5 years or till the child attains the age of majority, whichever is earlier

OTHER SCHEMES

S.NO.

CATEGORY

SCHEME CHARACTERISTICS/MINIMUM CONDITIONS

1

Index Funds/ Exchange Traded Funds

Minimum 95% investment in securities of a particular index (which is being replicated/ tracked) AMC to mention the name of the index

2

Fund of Funds (Overseas/ Domestic)

Minimum 95% investment in the underlying fund AMC to mention the name of the underlying fund

KEY MUTUAL FUND RATIO

1. Standard Deviation:

Standard Deviation value gives an idea about how volatile fund returns has been in the past 3 years. Lower value indicates more predictable performance.

So, if you are comparing 2 funds (let’s say Fund A and Fund B) in the same category. If Fund A and Fund B has given 9% returns in last 3 years, but Fund A standard deviation value is lower than Fund B. So, you can say that there is a higher chance that Fund A will continue giving similar returns in future also whereas Fund B returns may vary.

2. Beta

Beta value gives idea about how volatile fund performance has been compared to similar funds in the market. Lower beta implies the fund gives more predictable performance compared to similar funds in the market.

So, if you are comparing 2 funds (let’s say Fund A and Fund B) in the same category. If Fund A and Fund B has given 9% returns in last 3 years, but Fund A beta value is lower than Fund B. So, you can say that there is a higher chance that Fund A will continue giving similar returns in future also whereas Fund B returns may vary.

3. Sharpe Ratio

Sharpe ratio indicates how much risk was taken to generate the returns. Higher the value means, fund has been able to give better returns for the amount of risk taken. It is calculated by subtracting the risk-free return, defined as an Indian Government Bond, from the fund’s returns, and then dividing by the standard deviation of returns.

For example, if fund A and fund B both have 3-year returns of 15%, and fund A has a Sharpe ratio of 1.40 and fund B has a Sharpe ratio of 1.25, you can choose fund A, as it has given higher risk-adjusted return.

4. Treynor’s Ratio

Treynor’s ratio indicates how much excess return was generated for each unit of risk taken. Higher the value means, fund has been able to give better returns for the amount of risk taken. It is calculated by subtracting the risk-free return, defined as an Indian Government Bond, from the fund’s returns, and then dividing by the beta of returns.

For example, if fund A and fund B both have 3-year returns of 15%, and fund A has a Treynor’s ratio of 1.40 and fund B has a Treynor’s ratio of 1.25, then you can choose fund A, as it has given higher risk-adjusted return.

5. Jension’s Alpha

Alpha indicates how fund generated additional returns compared to a benchmark.

Let’s say if a fund A benchmarks its returns with Nifty50 returns then alpha equal to 1.0 indicates the fund has beaten the nifty returns by 1%, so the higher the alpha, the better.

6. Sortino Ratio

The Sortino ratio is a variation of the Sharpe ratio that differentiates harmful volatility from total overall volatility by using the asset’s standard deviation of negative portfolio returns—downside deviation—instead of the total standard deviation of portfolio returns. The Sortino ratio takes an asset or portfolio’s return and subtracts the risk-free rate, and then divides that amount by the asset’s downside deviation.

Just like the Sharpe ratio, a higher Sortino ratio result is better. When looking at two similar investments, a rational investor would prefer the one with the higher Sortino ratio because it means that the investment is earning more return per unit of the bad risk that it takes on.

For example, assume Mutual Fund X has an annualized return of 12% and a downside deviation of 10%. Mutual Fund Z has an annualized return of 10% and a downside deviation of 7%. The risk-free rate is 2.5%. The Sortino ratios for both funds would be calculated as:

Mutual Fund X Sortino = (12%−2.5%)/10% = 0.95

Mutual Fund Z Sortino = (10%−2.5%)/7% = 1.07

Even though Mutual Fund X is returning 2% more on an annualized basis, it is not earning that return as efficiently as Mutual Fund Z, given their downside deviations. Based on this metric, Mutual Fund Z is the better investment choice.

Budget 2022 has hardened the income tax filing norms for regular taxpayers. Under Union Budget 2022, Nirmala Sitharaman announced that the provision of updated return is available in Section 139(8A) of the Income Tax Act. The taxpayers now have a choice to rectify their income tax return by filing an Updated Income Tax Return. The new provision allows the taxpayers to update their ITRs within two years of filing, on payment of additional taxes, in case of errors or omissions.

The Central Board of Direct Taxes (CBDT) has now notified a new Form ITR-U for documenting updated Income Tax returns in which taxpayers will have to give specific justification for filing it along with the amount of income to be offered to tax. The new Form ITR-U will be available to taxpayers for filing updated income tax returns for 2019-20 and 2020-21 fiscals.

WHO CAN FILE AN UPDATED ITR?

Any person eligible to update returns for FY 2019-20 and subsequent assessment years as per the relevant provisions of the IT Act can file the updated return via Form ITR-U. A taxpayer can file updated return only once for each assessment year.

WHAT DETAILS ARE REQUIRED TO BE MENTIONED IN ITR-U?

In ITR-U, the assessee needs to specify only the amount of additional income, under the prescribed income heads, on which tax is required to be paid. No detailed income break-up needs to be submitted, as in the case of filing regular ITR forms. The taxpayer must also determine the exact reason behind updating the return in ITR-U. Further, it is required to mention the challan details for the additional tax paid for the updated return.

PRESCRIBED DATE TO FILE FORM ITR-U

Form ITR-U can be filed only for the preceding two years of the end of relevant assessment year. The provisions of section 139(8A) have been notified and came into effect from the beginning of financial year 2022-23, hence, in the financial year 2022-23, returns for AY 2020-21 and AY 2021-22 can only be furnished under Updated return.

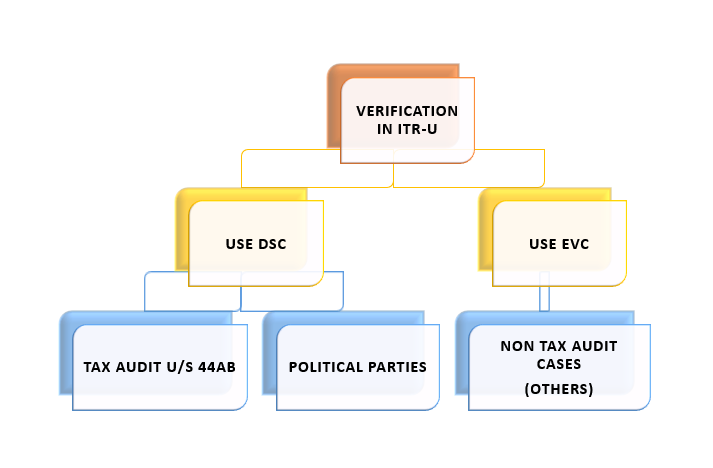

MANNER OF VERIFICATION OF UPDATED RETURN

Updated return shall be verified using Digital Signature Certificate (DSC) in case of political parties and companies who are liable for tax audit under section 44AB.

In other cases, the taxpayers have an option whether they want to file with Electronic Verification Code (EVC) or DSC.

WHAT ARE THE BENEFITS OF FILING UPDATED RETURN?

1) Taxpayer gets an additional time of 24 months to file Income Tax Return even after the due date of filing Original ITR, Belated ITR and Revised ITR have lapsed

2) Taxpayer can report any missed out incomes and pay tax on it thus reducing chances of future tax notices and litigations

3) Tax Liability and penalty under Updated Return is less than in case of proceedings for undisclosed income or income escaping assessment

CASES WHEN AN UPDATED RETURN OF INCOME CANNOT BE FURNISHED

The Form ITR-U cannot be filed in case of following reasons:

The provision does not allow the taxpayer to file the updated return if there is no additional tax outgo.

Where a search has been initiated under section 132 or requisition is made under section 132A of the Income-tax Act

Where a survey has been conducted u/s 133A other than survey u/s 133(2A) of Income-tax Act

Where any proceeding for assessment or reassessment or re-computation or revision of income is pending under the Income-tax Act

Where the Assessing Officer has information for Blank Money law, Benami law, etc. in the relevant assessment year.

Where any information is received under an agreement referred to in sections 90 or 90A of the Income-tax Act

Where any prosecution proceedings are initiated under the Income-tax Act.

PENALTY ON FILING UPDATED RETURN – PAY ADDITIONAL TAX UNDER SECTION 140B OF INCOME TAX ACT

The taxpayer filing an Updated Return must also submit proof of payment of tax and penalty as per Section 140B of the Income Tax Act.

The provision requires that the taxpayer has to pay an additional 25 per cent interest on the tax due if the updated ITR is filed within 12 months, while interest will go up to 50 per cent if it is filed after 12 months but before 24 months from the end of relevant Assessment Year. Non-payment of additional tax would be considered as invalid, and hence no return would be updated.

Therefore, the taxpayers looking to update their returns for FY 2019-20 will need to pay the tax due and interest along with an additional 50 per cent of such tax and interest. For those looking to file an updated return for FY 2020-21, the additional amount will be 25 per cent of the tax payable and interest.

NOTE: In case the taxpayer has not filed the Original return or Belated return, he/she will have to pay the taxes due for the relevant assessment year along with the late fees as per section 234F. He/she shall also pay the additional tax liability under section 140B of 25%/50% on the taxes due as per the circumstances.

A taxpayer can file an Updated ITR even if an original or belated ITR has not been filed. However, the taxpayer cannot file a Revised ITR if an original or belated ITR has not been filed

The taxpayer can file an Updated ITR only if there is an additional tax liability. In the case of a Revised ITR, there is no such restriction

The taxpayer need not pay any penalty for filing a Revised ITR. However, the taxpayer must pay a penalty in form of an Additional Tax of 25% to 50% as per Section 140B for filing an Updated ITR

Updated ITR can be filed only if there is an additional tax liability and not if there is a reduction in tax liability or an increase in the refund or claiming a loss. Revised ITR can be filed for multiple reasons such as claiming a loss, increasing refund, reduction or increase in tax liability, etc.

The taxpayer can file Revised Return multiple times while he/she can file Updated ITR only once.

A lively Small and Medium-sized Enterprise (SME) sector is an imperative element for a solid market economy. SMEs assume a significant part in the political economy, assisting to promote and strengthen reforms. There are about 44 million MSME units in India which contribute 45% of the India’s manufacturing output, account for about 35 % of our exports, and provide employment to more than 59 million people in the country.

The continuing development, intensity and prosperity of MSME units are complicatedly connected with the wellbeing and development of Indian economy. In the long term, SMEs can create a significant ascent in pay, opportunities and the overall GDP. Assuming the business environment to be helpful and steady to new organizations, they won’t just create more employment yet additionally make a variety of items and administrations for the consumers to choose from.

Where MSME are looking for re-organizing their working capital, make or buy decisions, new investment and return thereof, Chartered Accountants can play a very important role as business solution providers. They are being trained in three-year of thorough training to handle a wide range of challenges and having active experience. Chartered Accountants play significant part in the turn of events and advancement of SME area.

From making exceptional products to offering custom administrations, SMEs are an imperative piece of the financial texture of the world. There are many advantages of SMEs for entrepreneurs, buyers, workers and networks. Small and medium endeavours, as they are additionally known, can do things that can be challenging for larger organizations.

Few of the advantages are listed below:

Close relationship

It is quite possibly the clearest advantage. Medium and particularly small companies will manage their clients, which will empower them to address their issues more precisely and to offer a more individualized assistance, and even lay out some bond with their clients. When you know the business, the client’s connection with the SME will frequently be less difficult as compared to any large organization.CAs can play a significant part for making mindfulness among stakeholders.

Flexible

As a result of their size and less difficult construction, they will have a more prominent ability to adjust to changes. Furthermore, it will assist them with being nearer to their clients, which will permit them to know the variations in the market before any other individual.

Economic Development

SMEs have the remarkable capacity to fuel economic development. They set out many new job opportunities, drive the trend of advancement and extend the tax base. In most developing and developed economies, more than 90% of SMEs further develop the employment rate. As a matter of fact, when large businesses scale down and eliminate job opportunities, SMEs continue creating and developing more job positions.

Reduced complications in compliance:

At present a normal SME or start up invests a great amount of time and energy to deal with the different kinds of assessments at different places. Recording separate returns under every office, according to the specified courses of events, in itself is a nightmare. Further, businesses like restaurants, which fall under both sales and service taxation, have to calculate both VAT and service tax separately for compliance purposes. GST, by virtue of its unified structure and neat classification of goods and services for the purpose of taxation, essentially wipes out every such entanglement, and most importantly reduces compliance effort and costs.

Adaptable to dynamic environment:

SMEs act as a cushion against recession by adapting and innovating as per the changing circumstances. SMEs adapt fast to the dynamic business world by switching on to e-commerce and online transaction of goods and services. The progression in innovation has not just eased out the method involved with selling and purchasing, it has assisted the people with reducing expense on promoting and showcasing as well. The different online business platforms make life simple for SMEs.

CA professionals can play pro-active role in creating awareness entry into ready and big market of supplying to Ministries, departments and CPSUs through procurement policy; motivating and facilitating SMEs in registering under SPRS; by filing forms on behalf of SMEs and facilitating pre-registration capability audit.

Although SMEs have its downsides too, it is just with accuracy and care that the public authority can empower business by making business-accommodating approaches and simple funding options. Liberal arrangements urge prospective entrepreneurs to go all in and create value for themselves as well as society eventually. Chartered Accountants play major and important role in the development and promotion of MSME sector. Do not see a CA professional just for the purpose of audit; a certified Chartered Accountant can be of help in anything from money related issues to business related decisions.