Budget 2022 has hardened the income tax filing norms for regular taxpayers. Under Union Budget 2022, Nirmala Sitharaman announced that the provision of updated return is available in Section 139(8A) of the Income Tax Act. The taxpayers now have a choice to rectify their income tax return by filing an Updated Income Tax Return. The new provision allows the taxpayers to update their ITRs within two years of filing, on payment of additional taxes, in case of errors or omissions.

The Central Board of Direct Taxes (CBDT) has now notified a new Form ITR-U for documenting updated Income Tax returns in which taxpayers will have to give specific justification for filing it along with the amount of income to be offered to tax. The new Form ITR-U will be available to taxpayers for filing updated income tax returns for 2019-20 and 2020-21 fiscals.

WHO CAN FILE AN UPDATED ITR?

Any person eligible to update returns for FY 2019-20 and subsequent assessment years as per the relevant provisions of the IT Act can file the updated return via Form ITR-U. A taxpayer can file updated return only once for each assessment year.

WHAT DETAILS ARE REQUIRED TO BE MENTIONED IN ITR-U?

In ITR-U, the assessee needs to specify only the amount of additional income, under the prescribed income heads, on which tax is required to be paid. No detailed income break-up needs to be submitted, as in the case of filing regular ITR forms. The taxpayer must also determine the exact reason behind updating the return in ITR-U. Further, it is required to mention the challan details for the additional tax paid for the updated return.

PRESCRIBED DATE TO FILE FORM ITR-U

Form ITR-U can be filed only for the preceding two years of the end of relevant assessment year. The provisions of section 139(8A) have been notified and came into effect from the beginning of financial year 2022-23, hence, in the financial year 2022-23, returns for AY 2020-21 and AY 2021-22 can only be furnished under Updated return.

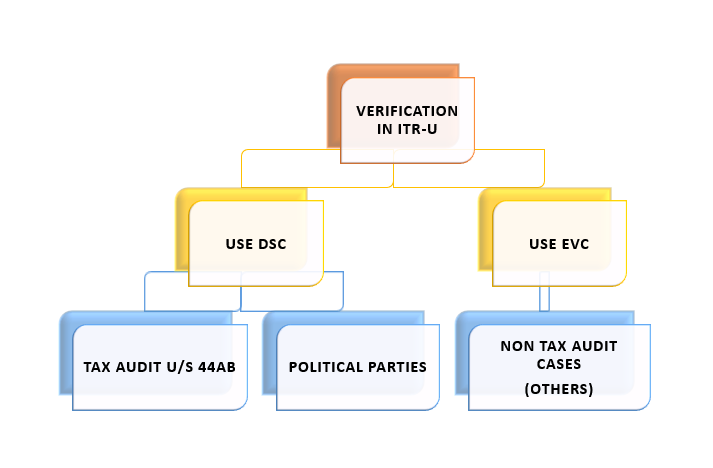

MANNER OF VERIFICATION OF UPDATED RETURN

Updated return shall be verified using Digital Signature Certificate (DSC) in case of political parties and companies who are liable for tax audit under section 44AB.

In other cases, the taxpayers have an option whether they want to file with Electronic Verification Code (EVC) or DSC.

WHAT ARE THE BENEFITS OF FILING UPDATED RETURN?

1) Taxpayer gets an additional time of 24 months to file Income Tax Return even after the due date of filing Original ITR, Belated ITR and Revised ITR have lapsed

2) Taxpayer can report any missed out incomes and pay tax on it thus reducing chances of future tax notices and litigations

3) Tax Liability and penalty under Updated Return is less than in case of proceedings for undisclosed income or income escaping assessment

CASES WHEN AN UPDATED RETURN OF INCOME CANNOT BE FURNISHED

The Form ITR-U cannot be filed in case of following reasons:

The provision does not allow the taxpayer to file the updated return if there is no additional tax outgo.

Where a search has been initiated under section 132 or requisition is made under section 132A of the Income-tax Act

Where a survey has been conducted u/s 133A other than survey u/s 133(2A) of Income-tax Act

Where any proceeding for assessment or reassessment or re-computation or revision of income is pending under the Income-tax Act

Where the Assessing Officer has information for Blank Money law, Benami law, etc. in the relevant assessment year.

Where any information is received under an agreement referred to in sections 90 or 90A of the Income-tax Act

Where any prosecution proceedings are initiated under the Income-tax Act.

PENALTY ON FILING UPDATED RETURN – PAY ADDITIONAL TAX UNDER SECTION 140B OF INCOME TAX ACT

The taxpayer filing an Updated Return must also submit proof of payment of tax and penalty as per Section 140B of the Income Tax Act.

The provision requires that the taxpayer has to pay an additional 25 per cent interest on the tax due if the updated ITR is filed within 12 months, while interest will go up to 50 per cent if it is filed after 12 months but before 24 months from the end of relevant Assessment Year. Non-payment of additional tax would be considered as invalid, and hence no return would be updated.

Therefore, the taxpayers looking to update their returns for FY 2019-20 will need to pay the tax due and interest along with an additional 50 per cent of such tax and interest. For those looking to file an updated return for FY 2020-21, the additional amount will be 25 per cent of the tax payable and interest.

NOTE: In case the taxpayer has not filed the Original return or Belated return, he/she will have to pay the taxes due for the relevant assessment year along with the late fees as per section 234F. He/she shall also pay the additional tax liability under section 140B of 25%/50% on the taxes due as per the circumstances.

A taxpayer can file an Updated ITR even if an original or belated ITR has not been filed. However, the taxpayer cannot file a Revised ITR if an original or belated ITR has not been filed

The taxpayer can file an Updated ITR only if there is an additional tax liability. In the case of a Revised ITR, there is no such restriction

The taxpayer need not pay any penalty for filing a Revised ITR. However, the taxpayer must pay a penalty in form of an Additional Tax of 25% to 50% as per Section 140B for filing an Updated ITR

Updated ITR can be filed only if there is an additional tax liability and not if there is a reduction in tax liability or an increase in the refund or claiming a loss. Revised ITR can be filed for multiple reasons such as claiming a loss, increasing refund, reduction or increase in tax liability, etc.

The taxpayer can file Revised Return multiple times while he/she can file Updated ITR only once.

A lively Small and Medium-sized Enterprise (SME) sector is an imperative element for a solid market economy. SMEs assume a significant part in the political economy, assisting to promote and strengthen reforms. There are about 44 million MSME units in India which contribute 45% of the India’s manufacturing output, account for about 35 % of our exports, and provide employment to more than 59 million people in the country.

The continuing development, intensity and prosperity of MSME units are complicatedly connected with the wellbeing and development of Indian economy. In the long term, SMEs can create a significant ascent in pay, opportunities and the overall GDP. Assuming the business environment to be helpful and steady to new organizations, they won’t just create more employment yet additionally make a variety of items and administrations for the consumers to choose from.

Where MSME are looking for re-organizing their working capital, make or buy decisions, new investment and return thereof, Chartered Accountants can play a very important role as business solution providers. They are being trained in three-year of thorough training to handle a wide range of challenges and having active experience. Chartered Accountants play significant part in the turn of events and advancement of SME area.

From making exceptional products to offering custom administrations, SMEs are an imperative piece of the financial texture of the world. There are many advantages of SMEs for entrepreneurs, buyers, workers and networks. Small and medium endeavours, as they are additionally known, can do things that can be challenging for larger organizations.

Few of the advantages are listed below:

Close relationship

It is quite possibly the clearest advantage. Medium and particularly small companies will manage their clients, which will empower them to address their issues more precisely and to offer a more individualized assistance, and even lay out some bond with their clients. When you know the business, the client’s connection with the SME will frequently be less difficult as compared to any large organization.CAs can play a significant part for making mindfulness among stakeholders.

Flexible

As a result of their size and less difficult construction, they will have a more prominent ability to adjust to changes. Furthermore, it will assist them with being nearer to their clients, which will permit them to know the variations in the market before any other individual.

Economic Development

SMEs have the remarkable capacity to fuel economic development. They set out many new job opportunities, drive the trend of advancement and extend the tax base. In most developing and developed economies, more than 90% of SMEs further develop the employment rate. As a matter of fact, when large businesses scale down and eliminate job opportunities, SMEs continue creating and developing more job positions.

Reduced complications in compliance:

At present a normal SME or start up invests a great amount of time and energy to deal with the different kinds of assessments at different places. Recording separate returns under every office, according to the specified courses of events, in itself is a nightmare. Further, businesses like restaurants, which fall under both sales and service taxation, have to calculate both VAT and service tax separately for compliance purposes. GST, by virtue of its unified structure and neat classification of goods and services for the purpose of taxation, essentially wipes out every such entanglement, and most importantly reduces compliance effort and costs.

Adaptable to dynamic environment:

SMEs act as a cushion against recession by adapting and innovating as per the changing circumstances. SMEs adapt fast to the dynamic business world by switching on to e-commerce and online transaction of goods and services. The progression in innovation has not just eased out the method involved with selling and purchasing, it has assisted the people with reducing expense on promoting and showcasing as well. The different online business platforms make life simple for SMEs.

CA professionals can play pro-active role in creating awareness entry into ready and big market of supplying to Ministries, departments and CPSUs through procurement policy; motivating and facilitating SMEs in registering under SPRS; by filing forms on behalf of SMEs and facilitating pre-registration capability audit.

Although SMEs have its downsides too, it is just with accuracy and care that the public authority can empower business by making business-accommodating approaches and simple funding options. Liberal arrangements urge prospective entrepreneurs to go all in and create value for themselves as well as society eventually. Chartered Accountants play major and important role in the development and promotion of MSME sector. Do not see a CA professional just for the purpose of audit; a certified Chartered Accountant can be of help in anything from money related issues to business related decisions.

Form 61A is a record of the statement of Specified Financial Transactions which must be furnished under the Income Tax Act, 1961 by certain institutions. Statement of Specified Financial Translations or SFT refers to information related to certain high-value transactions which specified persons are required to report to the income tax department. The SFT was earlier known as ‘Annual Information Return (AIR)’. The objective of SFT was to curb black money and widening the tax base.

APPLICABILITYOF FORM 61A

A banking company, Cooperative bank

A non-banking financial company (NBFC)

Any institution issuing credit card

Any person covered under audit under section 44AB of the Income Tax Act.

Post offices

A Nidhi referred to in section 406 of the Companies Act 2013

A company issuing bonds or debentures

A company issuing shares

A mutual fund institution

A company listed on the recognized stock exchange

A trustee of a mutual fund or such other person as authorized by the trustee

Authorize dealer, offshore banking unit, money changer or any other person defined in FEMA

Inspector general or sub-registrar appointed under Registration act, 1908

KEY SECTIONS OF FORM 61A

The following are the key sections and details mentioned on a typical Form 61A:

Full Name

Permanent Account Number (PAN)

Folio Number

Address

Financial Year in which the transactions carried out are being reported

Number of Specified Financial Transactions

Total Value of Specified Financial Transactions carries out in the financial year

Details of the transactions: date of transactions, name of transacting party, PAN of transacting party, full address, mode of transaction, transaction amount, transaction code, etc.

Note that transactions that must be declared and reported in Form 61A.

TRANSACTIONS TO BE REPORTED

Individuals responsible for furnishing Form 61A

Type of Transaction and limit

Banking Companies and Co-operative Banks

Cash payment for the purchase of POs (Pay orders) / DDs (Demand drafts) for amounts annually totalling Rs 10 lakh or more.

Banking Companies and Co-operative Banks

Cash payment exceeding Rs 10 lakh for purchasing any prepaid RBI instruments like RBI bonds, etc.

Banking Companies and Co-operative Banks

Deposits or withdrawals amounting to Rs 50 lakh or more from any number of current accounts of a person with the bank.

Banking Companies, Co-operative Banks and Post Offices

Deposit totalling Rs 10 lakh or more in bank accounts, other than current or time deposit accounts, of a person.

Banking Company, Co-operative Bank, Post Master General of Post office, Nidhi

Cash payment aggregating to INR 1 lakh or more in a year or Rs 10 lakh or more in any other mode of payment against any credit card bill which is issued to a customer in a year

A company or an institution issuing debentures or bonds

Receipt exceeding Rs 10 lakh or more in a year from an individual for acquiring such debentures/bonds

A company issuing shares

Receipt exceeding INR 10 lakhs in a year from an individual for acquiring such shares. This includes share application money received.

Listed companies

Share buyback from a person for an amount totalling Rs 10 lakh or more

Manager/Trustee of a Mutual Fund

Receipt equal to or exceeding Rs 10 lakh in a year from an individual acquiring the units of such Mutual Fund

A Dealer of Foreign Exchange

Receipt from a person for sale of a foreign currency or expenses incurred in such foreign currency via a debit/credit card or via the issue of draft or traveller’s cheque or any other financial instrument for an amount annually totalling Rs 10 lakh or more.

Inspector-General/Sub-Registrar appointed under the Registration Act, 1908

Sale/Purchase by a person of immovable property for Rs30 lakhs or more of sale value or value as per the stamp valuation authority.

Persons liable for audit u/s 44AB of the Income Tax Act

Cash receipt exceeding Rs 2 lakh by a person for sale of goods or rendering of services (other than the ones specified above)

DIFFERENT PARTS OF FORM 61A

Form 61A has two parts:

Part A contains statement level information which is common for all transaction types. Based on the transaction type, the report level information has to be reported in one of the following parts:

Part B (Reporting of aggregated financial transactions by the person)

Part C (Reporting of bank accounts)

Part D (Reporting of immovable property transactions)

PROCEDURE TO FILE SPECIFIED FINANCIAL TRANSACTIONS[SFT] ONLINE

Register on the Reporting portal under ‘My Account‘ menu.

All statements uploaded to the Reporting Portal should be in the XML format consistent with the prescribed schema published by the Income Tax Department.

Once XML is generated, sign and encrypt the XML using the Submission utility and prepare a package to be uploaded.

Submit the statement on Reporting Portal.

Upon successful submission, an email with “Acknowledgment Number” will be sent to the registered email id.

DUE DATE & PENALTIES

Due date for submitting Form 61A for the previous financial year is before 31st May of the applicable assessment year.

For the initial failure to file Form 61A within the due date, penalty shall be levied under Section 271A of Rs.500 per day.

The authorities would issue a notice to such an assessee, demanding the assessee to submit the form within 30 days from the issuance of such notice.

In case of continuous default even after the notice, the penalty would be levied of Rs.1,000 per day.

The penalty of Rs.1,000 would be calculated after the stipulated time as mentioned in the notice expires.

CONSEQUENCES FOR FILING DEFECTIVE FORM

If the reporting entity or individual discovers any inaccuracy or discrepancy in the information provided in Form 61A then it shall make the required corrections with the authorities within 10 days.

In case the income tax authorities fond out that the report is incomplete or defective, the reporting entity or individual is given 30 days from the date of intimation to rectify it.

Penalty of Rs.50,000 is levied on the reporting entities and individuals in case:

Inaccurate information is provided deliberately.

Inaccurate information is submitted but does not inform it and does not correct it within 10 days.

Angel tax essentially derives its genesis from section 56(2) (vii) (b) of the Income Tax Act, 1961. Angel Tax is the tax levied by the government on the start-ups who receive funding from Angel Investors.

Angel investors get benefits in the form of taxation as the entire investment made by investors is not taxed. Angel tax is imposed on the capital raised by the means of issue of shares by unlisted companies from an Indian investor if the share price of issued shares exceeds the fair market value of the company. The excess realization is considered as income and therefore, taxed accordingly under the head ‘Income from other Sources’.

Note that Angel Tax isn’t applicable in case of investments made by Venture Capital Firms or Foreign Investors. It’s limited to investments made only by Indian Investors.

WHO IS AN ANGEL INVESTOR?

An Angel Investor is a high-net-worth individual who provides financial backing for small start-ups or entrepreneurs, typically in exchange for ownership equity in the company. They are also known as a private investor, seed investor or angel funder. The funds that Angel Investors provide may be a one-time investment to assist the business get off the ground or an ongoing injection to support and carry the company through its difficult beginning stages. Angel investors usually give financial support to start-ups at the initial moments (where the risk of failing is relatively high) and when most investors are not prepared to back them up. They are the one who invests his money in a startup while it is still finding its feet and still struggling to establish itself in the marketplace.

As per the Income Tax Notification, Angel Investors with the minimum net worth of INR 2 crore or the average return of the income of more than INR 25 lakhs in the preceding 3 financial years will be eligible for full tax exemption (100%) on the investments that are made in the start-ups above the fair market value.

PURPOSE BEHIND ANGEL TAXATION:

The primary reason for the introduction of the ‘Angel Tax’ was to tax the excessive share premium received over and above the fair market value (FMV) by the private companies, which was widely being used as a mechanism for disclosure for unaccounted money or black money. Thus, this is one of the anti-abuse provisions introduced to prevent money laundering.

One more explanation for this is since just a minor level of the population follows the tax collection necessities (which include just 2% of the complete population), a large portion of the new businesses don’t keep up with legitimate books of record and show of their assets legibly. Due to this flaw, the income tax department of India is of view that the valuation of companies needs to be done by special officers based on prescribed guidelines and formulas. This will assist the department to do the proper valuation of assets of the company, which shall further lead to higher tax payment.

ANGEL TAX RATE

Angel Tax is levied on the start-ups at a rate of 30% (excluding cess) on the Premium received. The Premium here is calculated as the difference between the net investments in excess of the fair market value.

ELIGIBILITY CRITERIA FOR STARTUP RECOGNITION:

In order to be eligible for acquiring funds by Angel Investors, the company (start-ups) need to meet certain criteria, i.e.:

i. The Start-up should be incorporated as a private limited company or enlisted as a partnership firm or a limited liability partnership.

ii. An entity shall be considered as a start-up up to 10 years from the date of its incorporation.

iii. Turnover should be less than Rs.100 Crores in any of the preceding financial years.

iv. The company remains a start-up if the turnover per year does not cross the Rs 100 crore marks in any of the 10 years. Once the company crosses the limit, it no longer remains eligible to be called a Start-Up. The limit of Rs 100 crore has been upgraded from Rs.25 crore by the Indian government in the recent past.

v. Further in the calculation of threshold of INR 25 crores, the amount of paid-up share capital and share premium in respect of shares issued to any of the following persons will not be included:

A Non-resident or

A Venture Capital Company pr

A Venture Capital Fund

vi. The firm should have approval from the Department for Promotion of Industry and Internal Trade (DPIIT)

vii. The Start-up should be working towards innovation/ improvement of existing products, services and processes and should have the potential to generate employment/ create wealth.

viii. An entity formed by splitting up or reconstruction of an existing business shall not be considered a “Start-up.”

BENEFITS AVAILABLE TO AN ELIGIBLE START-UP:

Following benefits shall be available to an eligible start-up or its shareholders:

1. Exemption from levy of angel tax under Section 56(2) (vii) (b);

2. Deductions under Section 80-IAC of the income tax Act

3. Liberalized regime of Section 79 to carry forward and set-off the losses

4. Exemption under Section 54GB to the shareholder for making investment in a startup;

5. Access to the dedicated cell created by the CBDT to resolve the issues faced by the Start-Ups.

SECTION 80(IAC):

Tax Exemption under Section 80 IAC of the income Tax Act, 1961: A Start-up may apply for Tax exemption under section 80 IAC of the Income Tax Act. Post getting clearance for Tax exemption, the Start-up can avail tax holiday for 3 consecutive financial years out of its first 10 years since incorporation.

Eligibility Criteria for applying to Income Tax exemption (80IAC):

The entity should be a recognized Start-up;

Only Private limited or a Limited Liability Partnership is eligible for Tax exemption under Section 80IAC;

The Start-up should have been incorporated after 1st April, 2016 but before April 1, 2021

Profit Exemption to eligible Start-up entities under Section 80-IAC:

100% of its profits and gains is allowed as deduction to an eligible start-up for 3 consecutive assessment years out of the 10 years (beginning from the year of incorporation).

As per Section 80-IAC, an entity shall be considered as an eligible start-up if it satisfies the following criteria:

It is incorporated as a company (Private Ltd. Co. or Public Ltd. Co.) or an LLP.

It is incorporated on or after April 1, 2016 but before April 1, 2021.

Its turnover does not exceed Rs.25 Cr (Rs.100 Cr from 01.04.2020) in the previous year relevant to assessment year for which such deduction is claimed.

It is not formed by splitting up or reconstruction of a business already in existence.

It holds a certificate of eligible business from the Inter-Ministerial Board of Certification.

It is engaged in innovation, development or improvement of products or processes or services or a scalable business model with a high potential of employment generation or wealth creation.

SECTION 56:

ANGEL TAX UNDER SECTION 56(2) (VII) (B) OF THE INCOME TAX ACT –

Angel tax is the tax charged on the closely held company when it issues shares to any resident of India at a price which exceeds its fair market value. When this provision is triggered, the aggregate consideration received from issue of shares which exceeds its fair market value is charged to tax under the head ‘Income from other sources’ under section 56(2) (vii) (b).

TAX EXEMPTION UNDER SECTION 56 OF THE INCOME TAX ACT (ANGEL TAX)

Post getting recognition, a Start-up may apply for Angel Tax Exemption. A start-up shall be eligible for claiming exemption from levy of angel tax under section 56(2) (vii) (b) if following conditions are satisfied:

The entity should be a recognized Start-up;

Aggregate amount of paid-up share capital and share premium of the Start-up after the proposed issue of share, if any, does not exceed INR 25 Crore.

CONDITIONS FOR EXEMPTION FROM ANGEL TAX TO BE FULFILLED

An eligible start-up shall get exemption from Angel Tax as given u/s 56(2) (vii) (b). However, the exemption is provided subject to the condition that the start-up should not invest, within 7 years from the end of the latest financial year in which the shares are issued at a premium, in any of the following:

Building or land for the purpose (other than own use or as stock in trade or for the purpose of renting);

For advancing loans (other than where the lending of money is the substantial part of the business of the start-up);

Capital contribution to any other entity;

Shares and securities;

Motor Vehicle, aircraft, yacht, or any other mode of transport, the actual cost of which exceeds INR 10 Lakhs (other than that held by the start-up for the purpose of plying, hiring, leasing, or as stock-in-trade, in the ordinary course of business;

Jewelry (other than that held by the start-up as stock in the ordinary course of business);

Archaeological collections & Artifacts etc.

PROBLEMS WITH ANGEL TAX:

According to the Income Tax Laws of India, 30% of the investment made to a start-up is charged in the form of Angel Tax. This implies that a start-up is losing almost around 33% of the investment made to it in the form of tax. Angel tax is taking a huge toll on start-ups. A start-up company already has a lot on its plate. They have problems to handle and losing a tremendous portion of their investment in the form of tax is just not acceptable.

There are many reasons due to which startups are opposing this concept of angel taxation along with investors. As investors are reluctant to invest in Indian startups due to this concept, it imposes higher tax amount on them. Certain reasons are as mentioned below:

Payments made by Indian Residents are only liable for Angel tax. This means that if a start-up is funded by a resident Indian, then the start-up has to pay a certain share of this investment in the form of angel tax.

Investments made by non-resident investors and venture capitalists are not liable for Angel Tax deduction.

Angel taxation has halted the development and growth of startups, leaving them disheartened.

Due to large amount of taxation to be paid, many investors are avoiding making an investment in the market which has a huge impact on Indian industries as many large investors are avoiding funding due to the reason.

The imposition of angel tax hinges on the fair market valuation of the company and this has been a bone of contention between startups and the income tax department. The tax department goes by the rule book and calculates market value based on the net assets of the company. However, estimated growth prospects of the startup and future projections based on these growth prospects are major factors in determining the fair market valuation of the startup. The methodology difference in calculation of the market value of the startup makes it pay a hefty price in terms of angel tax at a whopping 30%. Angel tax in a way wipes away a major part of the investible surplus of the startup hurting its growth prospects and hitting hard on the viability of the business.

However, after facing a sustained backlash from the startup ecosystem against the imposition of angel tax, the government has finally assured the startups that no coercive action will be taken to collect angel tax and also appointed a committee to look into this issue.

WHAT ARE INITIATIVES TAKEN BY THE GOVERNMENT IN THIS REGARD?

To advance the startup industry, the government has taken some steps with regard to Angel Taxation as:

• Earlier, a company was regarded as a startup for a period of 7 years from the date of its incorporation. But now it has been increased to 10 years in order to provide benefits in terms of income tax for a further three years.

• Further, the limit for turnover has also increased from Rs.25 crores to rs.100 crores for the said financial year for the criteria to be regarded as a Start-up company.

In the case said entities meet the criteria as defined by the government, then exemption from angel taxation shall be given.

CONCLUSION

Regardless the fact that Angel tax was started with good intention, it has experienced many kickbacks. Angel Tax is deeply disapproved of by start-ups and investors alike. This has brought about a precarious decrease in the advancement of start-ups as they have spare funding. Investors, on the other hand, are also shying away from making investments in small companies. There are still many challenges that Startups and Investors are facing. This has completely disturbed the equilibrium and has made start-up survival all the tougher.

Some notifications issued by the Department to providing relief in current Pandemic Situation (Covid-19) in the country to the taxpayers on 1st May, 2021

Notification No. 08/2021- Central Tax- Relaxation in Interest for the month of March -2021 & April -2021:

Notification No. 09/2021- Central Tax-Waiver of Late Fees for specified taxpayers and specified tax periods:

Notification No. 10/2021- Central Tax-Extension in due date of filling of GSTR-4 (Composition Scheme) for Financial year 20-21 to 31st May, 2021

Notification No. 12/2021- Central Tax-Extension in due date of filling of GSTR-4 (Composition Scheme) for Financial year 20-21 to 31st May, 2021

Taxpayers having Turnover Exceeding 5 Crore in Preceding Financial Year

(Big Taxpayers required to file GSTR-3B and GSTR-1 on monthly basis)

Period

Return Type

Due Date

Return Filing Date

Interest

Late Fee

March-21

GSTR-3B

20-04-2021

Till 05-05-2021

9 % for first 15 days

Nil

After 05-05-2021

9 % for first 15 days than 18% thereafter

Rs. 20/50 per day

April-21

GSTR-3B

20-05-2021

Till 04-06-2021

9 % for first 15 days

Nil

After 04-06-2021

9 % for first 15 days than 18% thereafter

Rs. 20/50 per day

April-21

GSTR-1

11-05-2021

Till 26-05-2021

Not Applicable

Nil

After 26-05-2021

Not Applicable

Rs. 20/50 per day

Taxpayers having Turnover Upto 5 Crore in Preceding Financial Year

(Small Taxpayers required to file GSTR-3B and GSTR-1 on quarterly basis)

Period

Return Type

Due Date

Return Filing Date

Interest

Late Fee

Jan 21-March-21

GSTR-3B

22-04-2021

Till 07-05-2021

Nil for first 15 days

Nil

Between 08-05-2021 to 22-05-2021

9 % for first 16th day to 30th day

Nil

After 22-05-2021

9 % for first 16th day to 30th day than 18% thereafter

Rs. 20/50 per day

April-21

IFF

13-05-2021

Till 28-05-2021

Not Applicable

Nil

Composition Taxpayers

Period

Return Type

Due Date

Return Filing Date

Interest

Jan 21-March-21

CMP-08

18-04-2021

Till 03-05-2021

Nil for first 15 Days

Between 03-05-2021

9 % for first 16th day to 30th day

After 18-05-2021

9 % for first 16th day to 30th day than 18% thereafter

Jan 21-March-21

GSTR-4

30-04-2021

31-05-2021

Not Applicable

Notification No. 11/2021- Central Tax-Extension in due date of filling of ITC-04 for Financial year 20-21 to 31st May, 2021

ITC-04 is a declaration furnishing by the principal manufacturer in respect of the goods dispatched to Job workers for Job Work with certain conditions.

ITC-04 is a quarterly form. It must be furnished on or before 25th day of the month succeeding the quarter. According to the provision for Jan-21 to Mar-21 quarter, the due date is 25th April-21. But in the above notification, this due date of 25th April-21 is extended to 31st May-21.

Notification No. 13/2021- Central Tax-Compliance of Rule36(4) for the month of April-21 deferred till May-21 & IFF for April shall be available till 28th May,21

The CGST Rule-36(4)restrict taxpayer to claim ITC of 5% of the eligible credit available in respect of invoices or debit notes as per details uploaded by the suppliers.

Now as per this notification ITC claims to 5% of GSTR-2B (Auto populated) in GSTR-3B is relaxed for April 2021. The taxpayer can apply this rule cumulatively for both April-2021 and May -2021 while GSTR-3B for May 2021.

Further this notification extended due date to file IFF for the month of April-2021 by taxpayer opted QRMP scheme open to file originally from 1st May -2021 to 13th May-2021 now extended to 1st May -2021 to 28th May-2021.

Notification No. 14/2021- Central Tax-Extension of dates of various compliances till 31st May-2021

Notification under section 168A of CGST Act due date of compliance which falls during the period from the 15th April 2021 to 30th May 2021 extended to 31st May 2021.

Exception of above:

On section 39 but except Sub Section(3)- TDS Return u/s 51 (GSTR-7), Sub Section (4)- Return by Input service distributor (GSTR-6) and Sub Section (5)- Non- resident Taxpayer (GSTR-5)

It means the extension is allowed in all three sub sections as mentioned above.

Section 68 as far as E-way bill is concerned

Section 10 (3) – Composition Scheme shall lapse if turnover exceeds the prescribed limit.

Section 25- Procedure for registration.

Section 27- Provisions related to Casual taxable Person and Non- Resident taxable person

Section 31- Tax Invoice

Section 37- Furnishing details of outwards supplies

Section 47- Levy of Late Fee

Section 50- Interest on delayed payment of Tax

Section 69- Power to Arrest

Section 90- Liability of Partners of the firm to pay tax

Section 122- Penalty for certain offenses

Section 129- Detention, seizure, and release of goods and conveyance in transit.

Gift tax is an act introduced by the Parliament of India in 1958. It was introduced to impose tax on giving and receiving gifts under certain circumstances which is specified under the act. if the value of the gift exceeds Rs.50,000 then the gift is taxed as income in the hands of the person who receives the gift under the head ‘Income from other sources’ at normal tax rates. (Refer this link for the meaning of ‘Gift Tax’: https://consultcaonline.com/index.php/2022/05/20/what-do-you-understand-by-gift-tax/)

In case of Transfer of Shares & Securities by an individual:

Any gift whose value is upto Rs.50,000 is exempt in the hands of both the sender as well as the receiver.

Even if the monetary value of the gift received by a close relative exceeds Rs.50,000, it would be exempt and would not be taken under Income from Other Sources.

However, if the monetary value of the gift exceeds Rs.50,000 in case on non-relative, it is taxable under the head Income from OtherSources at the Fair market value and taxed at the respective slab rates.

And, in case of Sale of shares & securities by an individual which were earlier received as a gift :

It is taxable in the hands of receiver under the head Income from Capital Gain.

In case the gift had been given by any of the close relative, the taxable amount under Capital Gain would be calculated as the difference between the Sale Value as on the date of the transaction occurring and the Cost of Acquisition as on the date it was purchased by the previous owner (since FMV on the date of receiving the gift would be zero in case of relative).

However, in case the gift has been given by any non-relative, it would be taxable under IFOS at the time of receiving the gift, and capital gain would arise only when the shares or securities are sold.

The taxable amount under Capital Gain in case of non relative would be calculated as the difference between the Sale Value and the Fair Market value as on the date of receiving the gift.

Capital Gain can be Long-term or short-term depending upon the date of purchase of the sender.

If there is Short term capital gain, it would be taxable at the rate of 15% as per section 115A of Income Tax Act.

However, based on the purchase date of the sender, if there is long term capital gain, taxability would arise at the amount exceeding Rs.1,00,000 at a rate of 10% as per section 112A.

REPORTING: Sale of shares, ETFs, Mutual funds, etc. received as a gift would be taxable as Capital Gain under Schedule CG of ITR-2 of the taxpayer.

In case of sale of shares and securities in an HUF:

In case of Hindu Undivided Family (HUF) Business, all the members would be considered as “relatives”. However, the provision applicable for relative of an individual would not be applicable here.

In this case, if any shares or securities are transferred (as gift) from its members to the HUF, it is exempt and would not be liable to tax.

However, it is not the other way around. Any gift transferred from the HUF to its members would be liable to tax since this transaction would be suspicious and improper in the place of Karta to give any gift to its members without any personal motive.

India is a nation of close-sewn families and have a great deal of motivations to praise its diversified culture, customs and religion. Various events emerge where gifts are traded. As a matter of fact, gifting each other is a symbol of adoration and warmth and can likewise be an image of societal status.

Be that as it may, numerous times, gifts can likewise be a part of tax planning/tax avoidance. While tax planning inside the structure of law is admissible, tax avoidance is disallowed and can be penalized.

WHAT IS GIFT TAX?

Gift tax is an act introduced by the Parliament of India in 1958. It was introduced to impose tax on giving and receiving gifts under certain circumstances which is specified under the act. These gifts can be in any form including cash, jewelry, property, shares, vehicle, etc.

As per the Income tax act of 1961, if the value of the gift exceeds Rs.50,000 then the gift is taxed as income in the hands of the person who receives the gift under the head ‘Income from other sources’ at normal tax rates.

Income Tax on Gift received by an Individual or HUF is governed by provisions of Section 56(2)(x) of the Income Tax Act. As per the provisions of this Section, Gift Tax will not be levied under the subsequent 7 circumstances: –

1. Gifts received from Relatives:

Any gifts received from the ‘close’ relatives are exempted irrespective of the amount. Following people are covered under the definition of ‘close’ relatives:

Spouse of the Individual

Brother or Sister of the Individual

Brother or Sister of the spouse of the Individual

Brother or Sister of either of the parents of the Individual

Any Linear ascendant or descendent of the Individual

Any Linear ascendant or descendent of the spouse of the Individual

Spouse of the person mentioned above

NOTE:

Ø In case of HUF, all members would be considered its relatives.

Ø However, despite the fact that the actual gift is exempted in the possession of the recipient, any income earned from the gift might be taxable under the provisions of Clubbing of the Income Tax Act.

2. If the aggregate value of gifts received is upto Rs. 50,000

If the aggregate value of gifts (whether in cash or in kind) received from a person or persons (except relatives as specified above) in any financial year does not exceed Rs. 50,000/-, then such gifts aren’t susceptible to Gift Tax.

However, if the value of gifts received exceeds Rs. 50,000/-, then the whole gift so received is taxable as Income from other sources

3. On the occasion of Marriage of the Individual

Gifts received from any person (whether relative or non-relative) on the occasion of marriage is exempt from tax (irrespective of amount). But note that gifts are exempted only on the occasion of own marriage, and not on the marriage of anyone among the family.

4. Gift Tax on Property received

* In case of Immovable Properties, the stamp duty value would be considered and in case of Movable Properties, the fair market value would be considered.

KIND OF GIFT COVERED

MONETARY THRESHOLD

QUANTUM TAXABLE

Any immovable property such as land, building etc. without consideration

Stamp duty value* > Rs 50,000

Stamp duty value of the property

Any immovable property for inadequate consideration

Stamp duty value* exceeds consideration by > Rs 50,000

Stamp duty value Minus consideration

Any property (jewelry, shares, drawings etc.) other than immovable property without consideration

Fair market value *(FMV) > Rs 50,000

FMV of such property

Any property other than immovable property for a consideration

FMV exceeds consideration by > Rs 50,000

FMV Minus consideration (Same example in case of immovable property can be referred

The meaning of Property in the above-mentioned table has been defined as: –

Immovable Property being land or building or both

Shares and Securities

Jewelry

Archaeological Collections

Drawings

Paintings

Sculptures

Any other work of Art

PROVISION RELATED TO STAMP DUTY:

To calculate gift taxes on immovable property or land stamp duty on gift deeds as on the date of agreement fixing is considered if the value of stamp duty exceeds 50,000. It is done to avoid higher stamp duty because of the time gap between the agreement date and date of registration within the following scenarios:

Date of agreement and the date of registration is different.

If the consideration is paid either wholly or partly through any modes such as cheque, bank draft or electronic mode before the date of agreement for transfer.

Also, in case of disputes in the calculation of stamp duty, the stamp duty valuation authority calls for records and passes an order in writing of value as per Section 500 and lower of the stamp duty value or value arrived by Valuation officer (VO) is considered.

5. Gifts received under a Will or by way of Inheritance or in contemplation of Death of the payer

Any amount received under a will or via legacy or in contemplation of death of the payer is completely exempt in the possession of the recipient. There is no maximum cap in this case and the whole amount in cash/kind, received as gift is considered as tax free.

6. Gifts received from any Local Authority as defined in Section 10(20) are completely exempt.

7. Gifts received from any Fund or Foundation or University or other Education Institution or Hospital or other Medical Institution or any other Trust or institution referred to in Section 10(23C) or Gifts received from any fund or Institution registered under Section 12AA are also exempt, irrespective of value.

As indicated by the RBI, frauds had arisen as the most genuine concern in the administration of functional risk, with 90% of them situated in the credit portfolio of banks. Due to ever increasing frauds and the amount of non-Performing assets increasing drastically in every bank in India, RBI took the stand and introduced new reform, i.e., Agencies for Specialized Monitoring (ASM).

Indian Bank’s Association (IBA) has impaneled 83 agencies to monitor stressed loan accounts and regulate the cash flows of banks.

WHAT IS ASM?

ASM is an external agency (Chartered Accountants) which is introduced to monitor large credit exposures and huge advances of Banks/Consortium of banks. Consortium refers to the coming together of banks to sanction the limits for a certain purpose. There is always a Lead bank in a Consortium who has the majority power over others. Lead bank in a consortium of bank will select any particular agency and give the assignment to it for monitoring of account.

An Agency for Specialized Monitoring (ASM) is a mechanism of the bank, which allows it to take several steps to prevent or minimize the number of money laundering cases and misappropriation of funds. ASMs are committed to providing due diligence support in India. In the banking world, the explanation for due diligence support & services involves an in-depth investigation and analysis of the business or person’s credits, assets, and liabilities. A bank before investing or finalizing a transaction in a business initiates acquisition or gives out a loan to a customer to ensure that the deal would be lucrative and safe for the bank.

PURPOSE OF ASM:

With the effect of reporting under ASM, we come to know the problem in advance like inventory buildup, delay in receivables and diversion of funds. All the transactions will be under a strict vigilance. As employees of the banking industry don’t have such expertise in all the sectors and related business transaction, the services of ASM to closely track the activity of complex nature of transaction of borrower is to be tracked on each stage.

APPLICABILITY:

ASM will be applicable to all the debtors where exposure is above Rs.250 crores. The scope of work includes:

Regular auditing and scrutinizing deviations or fluctuations.

Monitoring of cash flow and transactions.

Analyzing of the organization’s work input and output.

Checking for misappropriation of funds or diversion of funds.

Ensuring compliance of terms and condition of sanction.

Extensive analysis of a company’s transactions, operations, and financial health.

Analyzing of Fund Flow Statement.

ASM is an entity having Chartered Accountants with good domain knowledge, experience and skill in different sectors, industries etc. In case of large exposure or exposure of specialized nature, such agency provides services of inspection, stock audit, cash flow monitoring and end use verification etc.

After bringing ASM to the banking world, Chartered Accountants have to be more careful and work diligently towards the responsibility of reporting under ASM.

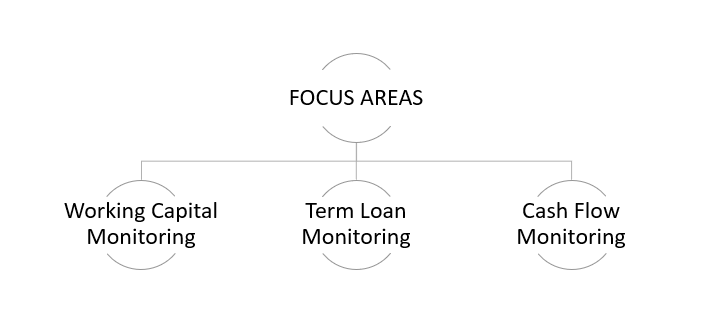

FOCUS AREAS:

Under ASM, Chartered Accountants does not have to necessarily check all the transactions, they mainly checks the transactions which are above the exposure limit. The main focus areas are:

REPORTING REQUIREMENTS:

There are some important areas which shall be covered by the firm under ASM reporting, these are-

Physical verification of stock shall be verified and reported with the help of GR note, e-way bill, etc.

Bank statements need to be verified extensively and sanction of drawing limit shall be checked.

Inventory Holding, Working Capital, Debtors, Ageing, Ratios, Shareholding Pattern etc.; all need to be checked thoroughly.

Documentation of working papers shall be managed properly by the Agency.

Any change in the industry and its impact on the client shall also be included in the report.

Disclosure of any contingencies and legal issues shall be reported.

And, report shall also specify whether the client has cooperated with the Agency and justifications for the same.

Along with these issues, report shall also include any disaster covered or any value addition or adverse remark by the company and any comment on the overall health of the company, whether good or bad as per the respective Chartered Accountant.

CARO 2020 is applicable to all the companies which were covered under CARO 2016. There has been absolutely no change on the applicability of CARO with respect to CARO 2016. It is applicable to all the statutory audits commencing on or after 1st April, 2021 corresponding to the financial year 2020-21.

Previously, there were 16 clauses and 10 sub-clauses, but after CARO 2020, there are 21 clauses and 28 sub-clauses. 7 clauses were newly entered, 1 clause has been merged and 1 has been deleted.

The amendments made under CARO 2020 have been divided into 4 categories:

SCHEDULE III AMENDMENTS –

Clause 3(i)(c) Title Deeds of Immovable Properties: There had been an amendment in this clause as-

“Whether the title deeds of all the immovable properties (other than the properties where the company is the lessee and the lease agreements are duly executed in favor of the lessee) disclosed in the financial statements are held in the name of the company, if not, provide the details thereof”.

2. Clause 3(i)(d) PPE Revaluation: This clause has been newly added under CARO 2020.

“Whether the company has revalued its Property, Plant and equipment (including the Right to Use assets) or intangible assets or both during the year and, if so, whether the revaluation is based on the valuation by a Registered Valuer; specify the amount of change, if change is 10% or more in the aggregate of the net carrying value of each class of Property, Plant and Equipment or intangible assets”;

3. Clause 3(i)(e) Benami Property: This clause has been newly added under CARO 2020.

“Whether any proceedings have been initiated or are pending against the company or holding any benami property under the Benami Transactions (Prohibition) Act, 1988 (45 of 1988) and rules made thereunder, if so, whether the company has appropriately disclosed the details in its financial statements.”

4. Clause 3(ii)(b) Working Capital: This clause has been newly added under CARO 2020.

“Whether during any point of time of the year, the company has been sanctioned working capital limits in excess of five crore rupees, in aggregate, from banks or financial institutions on the basis of security of current assets; whether the quarterly returns or statements filed by the company with such banks or financial institutions, are in agreementwith the books of account of the Company, if not, give details;

FAQs on Working Capital

Q1. Can working capital loan be sanctioned on the basis other than current assets?

A. No, working capital loan cannot be sanctioned other than on the basis of current assets.

Q2. If the amount of loan sanctioned is more than 5 crores, but the amount utilized is 1 crore – is it covered here?

A. Yes, it is covered here too since the provision only states about the sanction of the loan not about utilization.

Q3. Does the term ‘Sanction’ include Renewal?

A. Yes, renewal is allowed but it should be only on the basis of current assets.

Q4. If the company is also submitting monthly returns – whether the same also need to be verified by the auditor?

A. Guidance Note provides that the auditor will verify the returns on quarterly basis only. Even if the returns are submitted monthly, it will be verified by the auditor quarterly.

5. Clause 3(viii) Surrender or disclosure of Unrecorded income: This clause has been newly added under CARO 2020.

“Whether any transactions not recorded in the books of account have been surrendered or disclosed as income during the year in the tax assessments under the Income Tax Act, 1961, if so, whether the previously unrecorded income has been properly recorded in the books of accounts during the year”;

6. Clause 3(iii)(f) Loans /Advances to Promoters/ Related Parties: This clause has been newly added under CARO 2020.

“Whether the company has granted any loans or advances in the nature of loans either repayable on demand or without specifying any terms or period of repayment, if so, specify the aggregate amount, percentage thereof to the total loans granted, aggregate amount of loans granted to Promoters, Related Parties as defined in clause (76) of section 2 of the Companies Act, 2013.

7. Clause 3(ix)(b) Wilful Defaulter: This clause has been newly added under CARO 2020.

“Whether the company is a declared wilful defaulter by any bank or financial institutions or other lender”;

If the company is declared as a wilful defaulter, then the details such as date of declaration, date of default, amount of default and it’s nature, shall be disclosed to the Auditor.

8. Clause 3(ix)(d) Short term fund utilization for long term: This clause has been newly added under CARO 2020.

“Whether the funds raised on short term basis have been utilized for long term purposes, if yes, the nature an amount to be indicated”;

9. Clause 3(xix) Capacity of meeting current liability: This clause has been newly added under CARO 2020.

“On the basis of financial ratios, ageing and expected dates of realization of financial assets and payment of financial liabilities, other information accompanying the financial statements, the auditor’s knowledge of the Board of Directors and management plans, whether the auditor is of the opinion that no material uncertainty exists as on the date of the audit report that the company is capable of meeting its liabilities existing at the date of balance sheet as and when they fall due within a period of one year from the balance sheet date.

10. Clause 3(xx) Transfer of CSR fund: This clause has been newly added under CARO 2020.

(a) “Whether, in respect of other than ongoing projects, the company has transferred unspent amount to a Fund specified in Schedule VII to the Companies Act within a period of six months of the expiry of the financial year in compliance with second proviso to sub-section (5) of section 135 of the said Act”;

(b) “Whether any amount remaining unspent under sub-section (5) of the section 135 of the Companies Act pursuant to any ongoing project, has been transferred to special account in compliance with the provision of sub-section (6) of section 135 of the said Act”;

FUND RELATED AMENDMENTS

11. Clause 3(iii)(a) Investment/Guarantee/Security: There had been an amendment as well as new addition in this clause as-

“Whether during the year the company has made investments in, provided any guarantee or security or granted any loans or advances in the nature of loans, secured or unsecured, to companies, firms, Limited Liability Partnerships or any other parties, if so –

(a) Whether during the year the company has provided loans or provided advances in the nature of loans, or stood guarantee, or provided security to any other entity [not applicable to companies whose principal business is to give loans], if do, indicate –

(A)The aggregate amount during the year, and balance outstanding at the balance sheet date with respect to such loans or advances and guarantees or security to subsidiaries, joint venture and associates;

(B)The aggregate amount during the year, and balance outstanding at the balance sheet date with respect to such loans or advances and guarantees or security to parties other than subsidiaries, joint ventures and associates;

12. Clause 3(iii)(b) Investment, Guarantee, Security, Loan/Advance given – not prejudicial: There had been an amendment in this clause as-

“Whether the investments made, guarantees provided, security given and the terms and conditions of the grant of all loans and advances in the nature of loans and guarantees provided are not prejudicial to the company’s interest;

13. Clause 3(iii)(e) Ever-greening of Loan: This clause has been newly added under CARO 2020.

“Whether the loan or advance in the nature of loan granted which has fallen due during the year, has been renewed or extended or fresh loans granted to settle the overdues of existing loans given to the same parties, if so, specify the aggregate amount of such dues renewed or extended or settled by fresh loans and the percentage of the aggregate to the total loans or advances in the nature of loans granted during the year [not applicable to companies whose principal business is to give loans];

14. Clause 3(v) Deemed Deposit: There had been an amendment in this clause as-

“In respect of deposits accepted by the company or amounts which are deemed to be deposits, whether the directives issued by the Reserve Bank of India and the provisions of sections 73 to 76 or any other relevant provisions of the Companies Act and the rules made thereunder, where applicable, have been complied with, if not, the nature of such contraventions be stated; if an order has been passed by Company Law Board or National Company Law Tribunal or Reserve Bank of India or any court or any other tribunal, whether the same has been complied with or not;

15. Clause 3(ix)(a) Default in Repayment: There had been an amendment in this clause as-

“Whether the company has defaulted in repayment of loans or other borrowings or in the payment of interest thereon to any lender, if yes, the period and the amount of default to be reported in the format given – to give lender wise details in case of banks, financial institutions and Government only and not in respect of other lenders.

16. Clause 3(ix)(e,f) Fund – Subsidiaries, Associates, Joint Ventures: These clauses has been newly added under CARO 2020.

e) “Whether the company has taken any funds from any entity or person on account of or to meet the obligations of its subsidiaries, associates or joint ventures, if so, details thereof with nature of such transactions and the amount in each case;

f) “Whether the company has raised loans during the year on the pledge of securities held in its subsidiaries, joint ventures or associate companies, if so, give details thereof and also report if the company has defaulted in repayment of such loans raised;

17. Clause 3(xvii) Cash Losses: This clause has been newly added under CARO 2020.

“Whether the company has incurred cash losses in the financial year and in the immediately preceding financial year, if so, state the amount of cash losses;

CONTROL RELATED AMENDMENTS

18. Clause3(i)(a) Record of Intangible Assets: This clause has been newly added under CARO 2020.

B. “Whether the company is maintaining proper records showing full particulars of intangible assets”

19. Clause 3(ii)(a) Inventory Physical Verification: There had been an amendment in this clause as-

“Whether physical verification of inventory has been conducted at reasonable intervals by the management and whether, in the opinion of the auditor, the coverage and procedure of such verification by the management is appropriate; whether any discrepancies of 10% or more in the aggregate for each class of inventory were noticed and if so, whether they have been properly dealt with in the books of account;

20. Clause 3(ix) Fraud Related: There had been an amendment in this clause as-

“Whether any fraud by the company or any fraud on the company by its officers or employees has been noticed or reported during the year; if yes, the nature and the amount involved is to be indicated;

“Whether any report under sub-section (12) of Section 143 of the Companies Act has been filed by the auditors in Form ADT-4 as prescribed under rule 13 of Companies (Audit and Auditors) Rules, 2014 with the Central Government;

21. Clause 3(ix) Whistle Blower Complaints: This clause has been newly added under CARO 2020.

“Whether the auditor has considered whistle-blower complaints, if any, received during the year by the company;

22. Clause 3(xiv) Internal Audit system and report: This clause has been newly added under CARO 2020.

“Whether the company has an internal audit system commensurate with the size and nature of its business”;

“Whether the reports of the Internal Auditors for the period under audit were considered by the statutory auditor”;

23. Clause 3(xviii) Resignation of Statutory Auditor: This clause has been newly added under CARO 2020.

“Whether there has been any resignation of the statutory auditors during the year, if so, whether the auditor has taken into consideration the issues, objections, or concerns raised by the outgoing auditors;

24.Clause 3(xxi) Consolidated Financial Statements:This clause has been newly added under CARO 2020.

The CARO 2016 did not apply to the consolidated financial statements. But the CARO 2020 contains this clause that is now applicableto report on consolidated financial statements.

“Whether there has been any qualifications or adverse remarks by the respective auditors in the Companies (Auditor’s Report) Order (CARO) reports of the companies included in the consolidated financial statements, if yes, indicate the details of the companies and the paragraph numbers of the CARO report containing the qualifications or adverse remarks”

SPECIFIC REGULATION AMENDMENTS

25. Clause 3(xii)(c) Default in Payment: This clause has been newly added under CARO 2020.

“Whether there has been any default in payment of interest on deposits or repayment thereof for any period and if so, the details thereof”;

26. Clause 3(xvi) NBFC/CIC: This clause has been newly added under CARO 2020.

b) “Whether the company has conducted any Non-Banking Financial of Housing Finance activities without a valid Certificate of Registration (CoR) from the Reserve Bank of India as per Reserve Bank of India Act,1934”;

c) “Whether the company is a Core Investment Company (CIC) as defined in the regulations made by the Reserve Bank of India, if so, whether it continues to fulfil the criteria of a CIC, and in case the company is an exempted or unregistered CIC, whether it continues to fulfil such criteria”;

d)” Whether the Group has more than one CIC as part of the Group, if yes, indicate the number of CICs which are part of the Group”;

The aim of CARO 2020 is to enhance the overall quality of reporting by the company auditors. Therefore, CARO 2020 has included the above-mentioned reporting requirements.